There is no shortage of peer-to-peer loan platforms operating in the online space. While consumer choice is always a good thing, it can be somewhat challenging to differentiate between platforms. With that being said, Robocash aims to distance itself from its main market rivals by facilitating P2P loans in the emerging economies.

This includes the likes of Vietnam, Indonesia, Kazakhstan, and Russia. Although the platform covers multiple loan types, this mainly centres on payday loans. While this presents the opportunity to make double-digit annual returns, the risks of investing in peer-to-peer consumer loans – especially considering the location of the end-user, is fraught with risk.

As such, we would strongly recommend reading our in-depth RoboCash Review prior to signing up. Within it, we’ll cover the ins and outs of how the platform works, where your money is invested, how much you are likely to make, and of course – what risks you need to consider.

Robocash at a Glance

| Robocash - Visit |

|---|---|

| Product Type | Peer to Peer Lending |

| Potential Return | 12 - 14% |

| Fees | No Fees |

| Min Investment | €10 |

| Available to | European Union &Switzerland |

What is RoboCash?

Launched in 2017 and based in Croatia, Robocash is a crowdfunding platform that allows you to invest in consumer loans. The platform is owned by parent company Robocash Group – a Russia-based lender that facilitates loans for the consumer marketplace.

However, the reach of Robocash Group goes far and beyond just Russia. On the contrary, the lender provides financing in multiple jurisdictions across Europe and Asia. Crucially, while Spain is the exception to the rule, most of the loans hosted by Robocash Group are for consumers in emerging economies.

As a result, this gives you the opportunity to invest in consumer loans that yield double-digit annual returns. In fact, most of the loans hosted at Robocash yield between 10%-13%. This is considerably higher than what you would get by investing in a traditional asset class like fixed-rate bonds or shares.

With that said, the risks of lending your money out to consumers based in the emerging economies does come with its risks. While the platform does offer the all-important Buyback Guarantee, this isn’t a safeguard that is 100% fool-proof. Nevertheless, Robocash allows you to make an investment from just €10 per loan, so there’s every opportunity to diversify your holdings.

In terms of the loans themselves, these all centre on short-term loans that rarely surpass a term of 1 month. As such, you’ll likely be investing in payday loan-style structures. In some cases, you will have the opportunity to invest in installment loans with a longer repayment period, albeit, these are less common at Robocash.

So now that you have a basic understanding of what Robocash offers, in the next section we are going to look at eligibility.

Robocash Eligibility

Although Robocash is owned by a Russian company, the platform is focused on serving European customers. As such, you’ll need to be aged at least 18 years old and be based in the European Union.

Robocash also accepts customers from Switzerland, although those based in the United Kingdom are not eligible.

Other than being in possession of a European bank account, there are no other eligibility requirements to consider.

Types of Investments at Robocash

First and foremost, it is important to understand how the structure of Robocash works. As we briefly noted earlier, Robocash is owned by Russia-based Robocash Group. The parent company is a financing firm that has a number of loan originators under its belt. This includes Tez Credit, Zaimer, and Z Finance.

These loan originators will have a direct presence in countries such as Vietnam, Indonesia, and Kazakhstan. Everyday consumers based in the respective local market will apply for a loan, and then the originator will perform the required due diligence on the borrower. If the originator approves the loan, it will then appear on the Robocash platform.

When it does, you will then have the opportunity to invest money into the loan. To clarify, Robocash is not a lender. On the contrary, it is merely a third-party between you as an investor, and the individual loan originators that it has partnered with via Robocash Group.

Payday Loans

The vast majority of loans facilitated by Robocash and its group of originators are that of a payday loan. More specially, loans are typically for just a few hundred Euros at the most, with the end-borrower legally obliged to repay the funds when they next get paid.

For example, there is currently a funding opportunity listed at Robocash for a payday loan of just €71.21. The end-borrower is based in Kazakhstan, and the repayment term is 30 days. The annualized yield on the loan is 12%, which is a decent return.

However, it is important to note that the end-borrower is likely to be paying considering more than 12% on the loan. As we’ll cover further down in our review, this disparity in interest is how Robocash makes its money, and it also funds the Buyback Guarantee.

Robocash loans on a short-term basis can vary from 7 days to 1 month. The minimum amount that the end-borrow can obtain is €14, and the maximum is capped at €420.

Installment Loans

On top of short-term payday loans, Robocash also lists installment loans. These can vary from just 1 month, up to a maximum term of 1 year. The minimum amount that can be borrowed via a Robocash installment loan is €353, with the maximum capped at €14,120.

Crucially, installment loans are always secured, meaning that the end-borrower is required to put an asset up as collateral. However, installment loans at Robocash are less prevalent in comparison to payday loans.

How Much can I Make at Robocash?

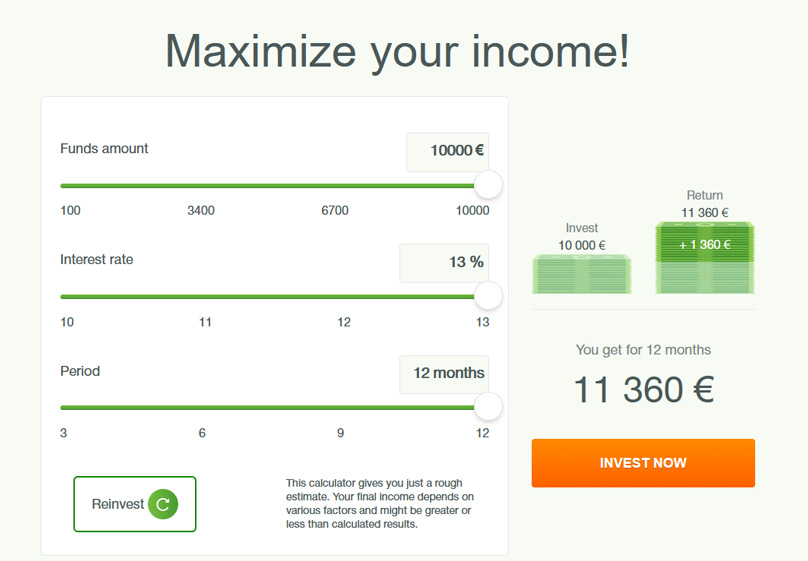

As is the case with most peer-to-peer lending sites active in the market, the potential returns available at Robocash are highly attractive. The platform notes that since its inception in 2017, investors have made average annualized returns of 12%.

However, there is no guarantee that this will always be the case. Nevertheless, most of the loans hosted by Robocash come with an annual return of between 10% and 13%.

How do I get my Money Back?

The investment process at Robocash operates much the same as any other P2P site in the space. Once you have made an investment, the end-borrower will be required to repay the funds on the agreed repayment date. As most of the loans at Robocash are for terms of less than 30 days, this is usually when they next get paid.

When the loan has been repaid in full, the loan originator in question will then forward the funds to Robocash. In turn, Robocash will then credit your account. This is ideal if you are the type of investor that doesn’t like to lock your funds away for long periods of time.

The only exception to this is if the loan is a longer-term installment loan. If this is the case, then you will receive fixed monthly payments until the loan is settled in full.

Manual Investing vs Auto Invest

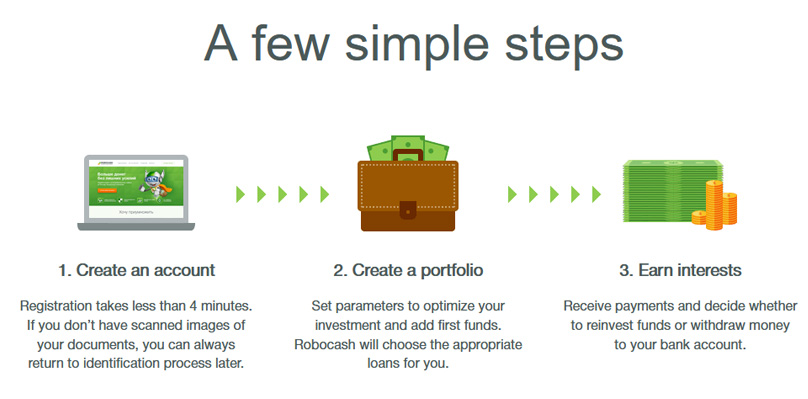

Once you have opened an account and deposited funds, you will have the option of choosing your investments manually, or utilizing the auto invest feature.

DIY Investing

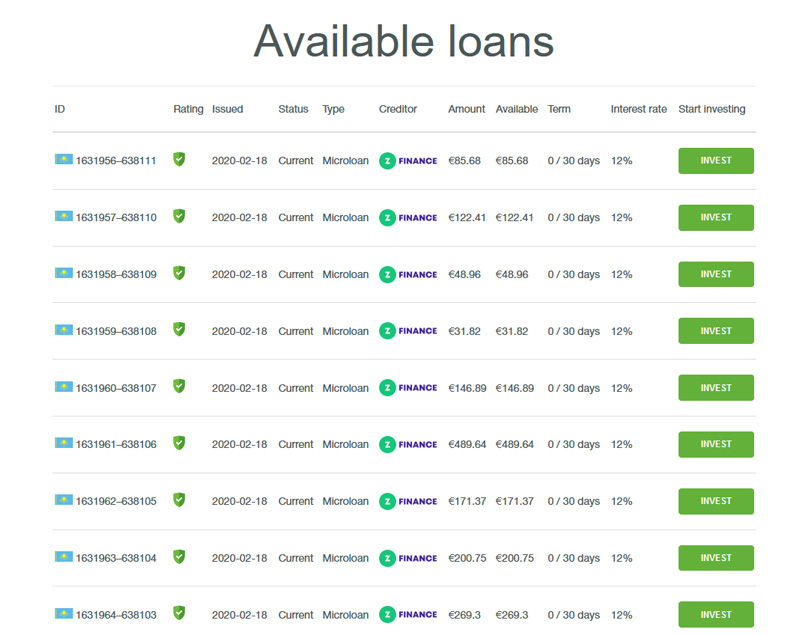

If you prefer to choose your own investments on a DIY basis, you’ll be presented with a range of information on each loan type. This includes the following:

- Country that the end-borrower is located

- Type of loan structure

- Size of the loan

- How much is available to invest

- The loan term in days

- Interest rate paid on the investment

Once you have found an investment that you like the look of, you simply need to choose how much you want to inject, and you can then forget about it until the funds are repaid.

While this does give you a more hands-on approach to investing, choosing your loan structures manually can be extremely time-consuming. Moreover, you are somewhat hindered in the ability to diversify across hundreds of loans, and you’ll need to repeat the process every few days if you want to reap the rewards of compound interest.

As such, it might be worth considering the auto invest feature.

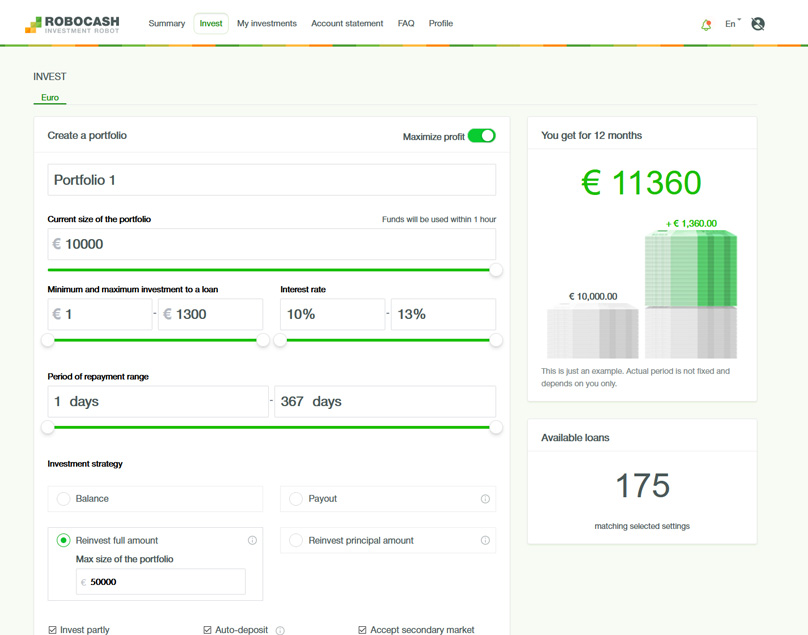

Auto Invest

Most members of Robocash opt for the auto invest plan. As the name suggests, this allows you to invest without needing to manually choose your own loan structures.

Instead, you simply need to set some initial parameters, and then Robocash will take care of the rest.

Here’s what you need to do:

- Choose a portfolio name

- Decide the minimum amount you want to invest per loan, as well as the maximum.

- Choose the interest rate range that you want to invest in

- Select the minimum and maximum loan term in days

- Decide whether or not you want your payments reinvested

Once you’ve set up the above parameters, you won’t need to do anything else. With that being said, we would strongly suggest that you consider utilizing the re-investment option. This means that every time you receive a payment on one of your loans, Robocash will automatically purchase new loans.

As such, you’ll benefit from the effects of compound interest – which should sit at the heart of your long-term investment goal.

How Much can I Invest at Robocash?

The minimum amount that you can invest at the platform is €10. Robocash has capped the maximum investment amount to €10,000, which is somewhat restrictive. As such, when you reach the €10,000 threshold, you won’t be able to invest anymore.

Robocash Deposits and Withdrawals

When it comes to funding your Robocash account, the only supported method is that of a bank transfer. The account must be in your name, and come from a European bank account.

You will be required to withdraw your balance back to the same bank account. There are no fees to deposit or withdraw funds, which is great.

Robocash Fees

One of the most attractive aspects of using Robocash is that you will not be charged any fees to use the platform. This is in stark contrast to other peer-to-peer lending sites, which often charged a variable fee every time you invest, or an annual maintenance fee.

With that being said, Robocash is in the business of making money, so how does it achieve this if no fees are charged? In a nutshell, the parent company – Robocash Group, has a number of loan originators within its network. When these loan originators approve financing, it will be at a rate significantly higher than what you receive in interest.

For example, while most short-term loans at Robocash pay in the region of 10%-13%, the end-borrower will be paying substantially more. As is the case with most payday loan structures, this is likely to be triple-figures at the very least.

As such, not only does Robocash profit from the disparity in interest, but this also paves the way for the platform’s Buyback Guarantee.

Is my Money Safe at Robocash?

As is the case with any investment platform that you plan to use for the first time, you need to make some serious considerations regarding safety. After all, annualized yields of 10%-13% are going to be anything but risk-free.

The biggest risk that you will face at Robocash is a default on the loan you have invested in. This will be the case if the end-borrower fails to meet their repayment date. On the one hand – this wouldn’t be overly detrimental when you consider the size of the loans issued. However, if multiple defaults occur at any given time, this could have a trickle-down effect on your earnings.

The good news is that there are a number of safeguards in place to reduce your exposure to a loss.

High-Interest Protection

First and foremost, it is important to remember that loans come with average returns of 10%-13%. As such, this gives you an extremely wide safety net in the event that a default occurred.

This means that were your investments to take a couple of hits along the way, you would likely still make a reasonably good profit. However, this is on the proviso that you install the necessary diversification tools – which is best realized via the auto invest feature.

Buyback Guarantee

More and more peer-to-peer loan platforms are now installing a Buyback Guarantee. In its most basic form, the Buyback Guarantee covers your investments in the event that the end-borrower defaults.

The good news is that each and every loan facilitated by Robocash benefits from the Buyback Guarantee. This means that if the end-borrower fails to repay their loan 30 days after the agreed repayment date, Robocash will purchase the loan agreement.

As we briefly mentioned earlier, the Buyback Guarantee is funded from the surplus interest that the loan originator charges. However, it is crucial to recognize that the Buyback Guarantee is not a guarantee in its truest form.

On the contrary, the guarantee is only as good as the underlying company offering it. As such, were Robocash to run into financial difficulties, it might not have the required capital to honour the Buyback Guarantee. If it doesn’t, then your entire investment portfolio is at risk of loss.

Platform Failure

If Robocash was to cease trading, all of the outstanding investments at the platform would be the responsibility of the respective administrator or liquidator. While this doesn’t guarantee beyond doubt that you will receive your money back, you will have a legal claim over the amount you have vested at Robocash.

Can I Sell my Robocash Investment Early?

Unlike other crowdfunding platforms active in the P2P arena, Robocash does not offer a secondary marketplace. However, we would argue that it doesn’t really need one. When you consider that the vast majority of loans hosted at the platform mature in less than 30 days, a secondary market would be somewhat redundant.

While the platform also hosts longer-term loans from time-to-time, you are under no obligation to invest in these. Instead, if liquidity could be an issue further down the line, ensure that your auto invest parameters are limited to 30 days.

Ultimately, if you feel that having your money locked away for up to month is beyond the realms of comfort, then the investment arena might not be right your individual profile.

Customer Support at Robocash

If you require assistance at Robocash, the platform offers a number of support channels. The easiest way to make contact is via the live chat facility.

If you prefer to speak with somebody over the phone, you can call Robocash at +385 1344-58-18 (Croatia Country Code)

Alternatively, you can send an email to support@robo.cash.

Robocash Review: The Verdict?

In summary, apart from offering the ability to invest in loans issued in emerging economies, Robocash is much the same as any other peer-to-peer platform operating in the market. For example, you’ll have access to annualized double-digit yields at the click of a button, and you can get started from just €10 per investment.

Moreover, the platform offers a highly useful auto invest feature, so once you’ve deposited the required funds, Robocash takes care of the rest. As is the case with other P2P sites, Robocash also offers a Buyback Guarantee. Although this doesn’t guarantee that your money is 100% safe, it does offer much-needed protection on a borrower default.

All in all, Robocash ticks most boxes. Just make sure that you have a firm understanding of the underlying risks, and diversify your holdings as much as you can.

RoboCash

Pros

- Great Returns

- Auto-Investing

- Buyback Guarantee

- Minimum Investment €10

- No investment fees

Cons

- Not Regulated

- No secondary market

- Website is Dated

- Maximum investment is €10,000

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants