Key Takeaways

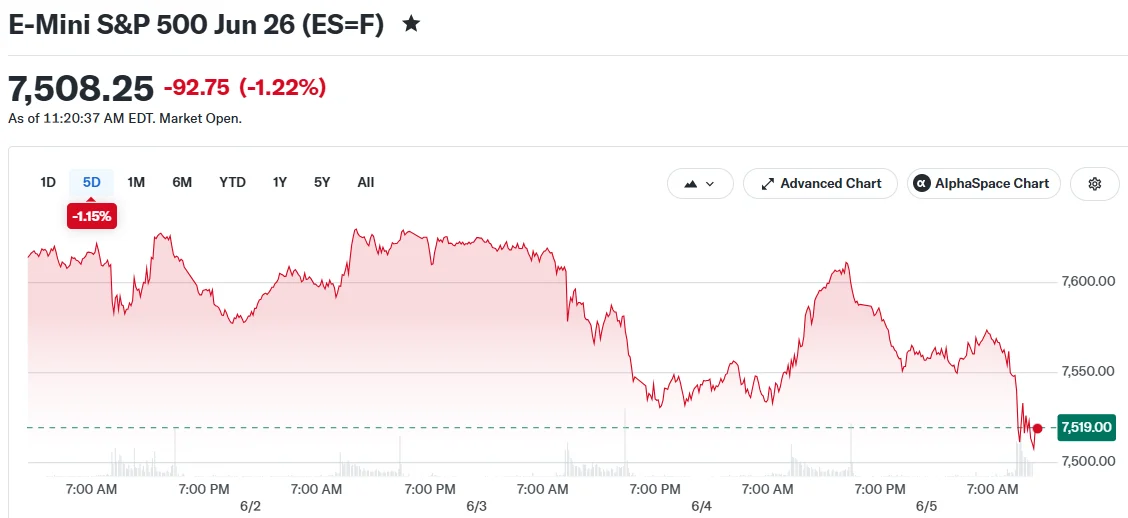

- Major indices declined Friday with Nasdaq losing 2.1%, S&P 500 down 1.1%, and Dow shedding 140 points

- May employment report revealed 172,000 new positions, significantly above the 88,000 consensus estimate

- Robust labor market data elevated rate increase probability to 68.3%, eliminating expectations for policy easing

- Semiconductor stocks continued declining following Broadcom’s disappointing earnings reaction

- S&P 500’s historic 9-week rally, longest since 1985, faces potential end

Equity markets experienced significant declines Friday following an unexpectedly strong employment report that elevated speculation about potential rate increases while technology stocks faced renewed pressure from artificial intelligence spending concerns.

The tech-heavy Nasdaq plummeted 2.1%. The S&P 500 declined 1.1%. The Dow Jones Industrial Average retreated approximately 140 points, representing a 0.3% loss.

The market downturn resulted from two distinct pressures converging simultaneously.

Employment Data Exceeds Forecasts

The May nonfarm payrolls data indicated American employers created 172,000 positions during the month. Wall Street analysts had projected approximately 88,000 additions. The jobless rate remained unchanged at 4.3%.

The better-than-anticipated figures transformed market expectations regarding Federal Reserve monetary policy. Market participants rapidly adjusted their positioning to reflect heightened probability of at least one rate increase before year-end.

The likelihood of a rate hike surged to 68.3%, climbing from 50.4% recorded the previous trading session. This development essentially eliminates near-term prospects for policy accommodation.

Eric Winograd, chief US economist at AllianceBernstein, said the data shows the economy is still holding up. “That’s enough to keep the Fed on hold,” he wrote.

These developments unfold as President Trump maintains public advocacy for rate reductions. Kevin Warsh, Trump’s appointee, has recently assumed leadership as Fed chair.

Semiconductor and AI Sectors Face Continued Pressure

Broadcom experienced substantial losses Thursday following its quarterly earnings announcement. Friday brought additional declines for the company’s shares.

The wider semiconductor industry mirrored this weakness. Market participants have adopted increasingly cautious stances regarding artificial intelligence infrastructure investments, with Broadcom’s financial results amplifying these apprehensions.

Technology equities had experienced robust gains throughout recent weeks, providing significant support for benchmark indices. That upward trajectory has now encountered resistance.

The Nasdaq had emerged as a primary beneficiary of enthusiasm surrounding AI technologies. The index now bears the brunt of deteriorating sentiment in this sector.

Historic Rally Faces Potential Conclusion

The S&P 500 approached Friday’s session positioned for a tenth consecutive week of advances. Such a streak would have represented the longest sustained rally since 1985.

That impressive run now confronts the possibility of termination.

The benchmark has retreated as multiple challenges accumulate — monetary policy concerns, technology sector vulnerability, and international political tensions.

Indications of stalled US-Iran ceasefire discussions contributed to the cautious atmosphere across Wall Street. President Trump characterized negotiations as reaching their “final” phases, though considerable uncertainty persists.

Futures contracts had already signaled lower openings before the employment statistics released, with Nasdaq 100 futures pacing the morning session’s declines.

The convergence of resilient employment conditions, hawkish monetary policy expectations, and faltering artificial intelligence momentum left limited opportunities for equity investors Friday.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants