Key Takeaways

- Wall Street banking giant JPMorgan recommends purchasing semiconductor equities following a challenging opening to the latter half of 2026

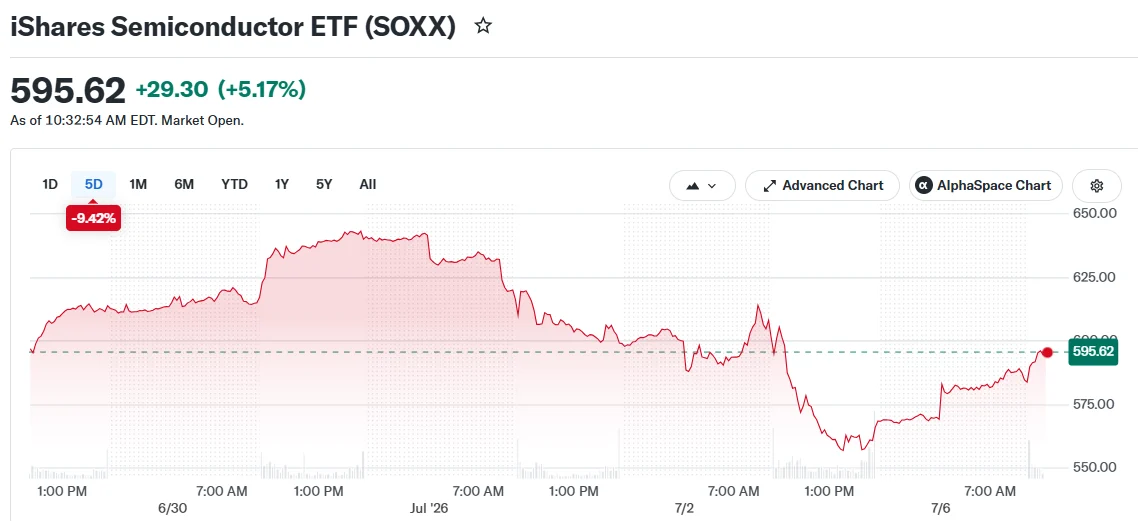

- The PHLX Semiconductor Sector Index declined 5.4% in the prior week but surged 2.5% at Monday’s opening bell

- JPMorgan’s investment hierarchy places semiconductors above cloud hyperscalers, with both preferred over sectors vulnerable to AI disruption

- The financial institution maintains a bearish stance on software, business services, and media sectors, labeling them vulnerable to AI-driven revenue erosion

- JPMorgan anticipates wider market participation during the second half, with smaller capitalization stocks and global markets poised for gains

The semiconductor industry experienced a challenging opening to 2026’s second half. The PHLX Semiconductor Sector Index, commonly referenced by its ticker SOX, dropped 5.4% throughout the abbreviated trading period preceding the Independence Day holiday. This marked the index’s consecutive second weekly retreat.

However, analysts at JPMorgan view the recent decline as an attractive entry point rather than a cautionary signal.

Mislav Matejka, a strategist at JPMorgan, informed clients via a Monday research note that the semiconductor industry’s growth cycle shows no signs of “peaking anytime soon.” The strategist emphasized that substantial new production capacity won’t materialize until 2028 at the earliest.

Market sentiment reflected this optimistic outlook. The SOX index jumped 2.5% at Monday’s open. The Nasdaq Composite climbed 0.7% shortly following the opening bell as investor enthusiasm for artificial intelligence chip manufacturers returned to the Street.

Multiple equities that underperformed during the previous week spearheaded Monday’s recovery. Applied Materials, Marvell, and Broadcom all registered gains. Memory-focused companies including Western Digital, Seagate, and Sandisk also rebounded strongly, propelling the Roundhill Memory ETF upward by more than 6.1%.

Sectors Facing Headwinds According to JPMorgan

While maintaining an optimistic view on semiconductors, the bank expresses greater reservation regarding other segments of the artificial intelligence investment landscape.

Matejka outlined the firm’s investment hierarchy as “semis over hyperscalers over AI at risk plays.” Regarding the Magnificent Seven technology giants, he noted the group is “likely to see derating continuing on monetization fears.”

JPMorgan maintains what it describes as a “fundamentally bearish” position on sectors facing AI-driven revenue cannibalization. These include software, business services, and media industries. While the bank acknowledges that temporary rebounds may occur when these segments become excessively oversold, the fundamental outlook remains pessimistic.

The underlying logic centers on artificial intelligence technologies eroding rather than enhancing revenues for enterprises operating within these industries.

Second Half Market Perspective for 2026

Beyond the semiconductor sector, JPMorgan anticipates global equity markets will establish new record highs during the year’s remaining months.

The institution cites robust corporate earnings projections, moderating inflationary pressures, and conservative investor positioning as fundamental supporting elements.

Matejka also identified the resolution of geopolitical tensions involving Iran as a potential market catalyst. He suggested that crude oil quotations, inflation forecasts, government bond yields, and central bank interest rate expectations could all reverse the movements observed during the second quarter.

The strategist noted that artificial intelligence will “unlikely to be the only story in town” throughout the second half. Smaller capitalization equities, cyclical sectors, and international markets should all experience benefits as investment participation expands across broader segments.

Stagflation concerns, which dampened market sentiment throughout recent months, are projected to diminish according to the strategist’s assessment.

JPMorgan’s investment thesis remains straightforward. Semiconductor exposure represents the optimal approach for capitalizing on artificial intelligence trends currently. Alternative segments within the AI investment theme present elevated risk profiles.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants