Key Highlights

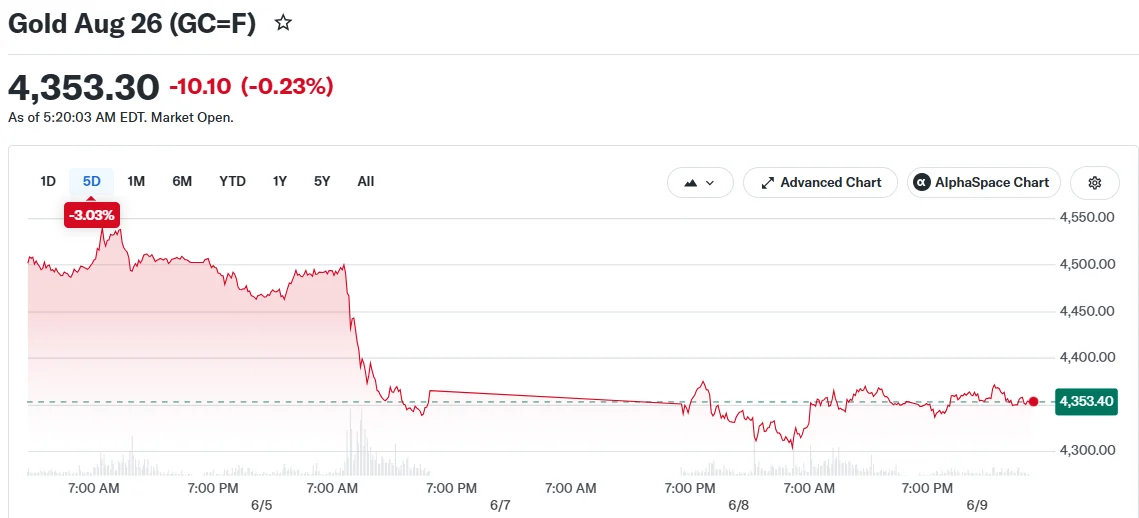

- The precious metal is trading close to an 11-week bottom, fluctuating between $4,328 and $4,333 per ounce following last week’s nearly 5% decline.

- A ceasefire agreement between Iran and Israel has reduced geopolitical tensions that previously supported bullish sentiment.

- Robust U.S. employment figures have bolstered the case for the Federal Reserve maintaining elevated interest rates longer than anticipated.

- Traders are now assigning approximately 70% probability to a Fed rate increase before year-end.

- Wednesday’s U.S. consumer inflation report and Thursday’s producer price index could determine gold’s near-term trajectory.

The yellow metal has faced considerable headwinds recently. Prices collapsed to their weakest point since March 23 during last week’s session, declining nearly 5% amid the most severe escalation of Middle Eastern conflict since the April ceasefire took effect.

During Tuesday’s Asian trading session, spot gold prices remained confined within a narrow range of $4,328 to $4,333 per ounce. Meanwhile, U.S. Gold Futures experienced a modest decline, settling around $4,358 per ounce.

The selloff was primarily triggered by last week’s unexpectedly strong U.S. employment report. These figures have intensified speculation that the Federal Reserve may maintain its restrictive monetary policy stance for an extended period, which generally undermines gold’s attractiveness as it generates no interest income.

Current market pricing suggests approximately 70% odds that the Fed will implement a rate hike before December arrives.

The U.S. Dollar Index climbed to a two-month peak before retreating 0.2% on Tuesday, creating additional headwinds for dollar-priced commodities including gold.

Middle East Ceasefire Reduces Risk Premium

Gold received modest support following the announcement that Iran and Israel have committed to suspending military operations after last weekend’s violence escalation.

President Donald Trump declared Monday night that the United States was approaching a “total victory” declaration regarding the Iran situation and predicted a significant decline in crude oil prices.

The conflict, now entering its fourth month, has interfered with energy transportation through the Strait of Hormuz, elevated crude oil valuations, and heightened worries about worldwide inflation.

This inflationary dynamic has worked against the precious metal. Elevated oil prices have maintained upward pressure on Treasury yields and dollar strength, diminishing the attractiveness of assets that don’t generate income.

Complicating matters further, Yemen’s Houthi movement, backed by Iran, declared a blockade targeting Israeli vessels in the Red Sea on Monday, introducing additional regional instability.

Rhona O’Connell, who leads market analysis at StoneX Group, indicated that fundamental questions surrounding the conflict remain “unresolved” and mentioned the firm is monitoring for potential bargain-buying activity.

Inflation Reports Take Center Stage

Market participants are now concentrating on Wednesday’s U.S. consumer price index release, with producer price data following Thursday.

These economic indicators will provide crucial insight into whether elevated energy expenses are translating into wider inflation pressures. The outcomes could substantially alter Federal Reserve policy expectations and influence gold’s direction accordingly.

Silver registered gains of approximately 0.4–0.5%, reaching roughly $68 per ounce. Platinum climbed 0.3% to trade at $1,767 per ounce. Copper prices advanced across both London Metal Exchange and U.S. futures platforms.

Gold continues navigating between competing dynamics: diminishing geopolitical tensions in the Middle East providing downward pressure, while elevated U.S. interest rate expectations maintain resistance to upward movement.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants