TLDR

- Greenback stabilized near a two-week trough following disappointing June employment figures that dampened Fed rate hike speculation

- Japanese currency hovers near four-decade weakest levels around 161-162 versus the dollar, sustaining intervention concerns

- Federal Reserve policy meeting minutes scheduled for release this week, though new Chair Kevin Warsh’s approach may limit forward guidance

- European currency maintained position near $1.1435 while British pound traded around $1.3351, both experiencing modest Monday declines

- Seoul introduced groundbreaking round-the-clock onshore dollar-won spot market on Monday

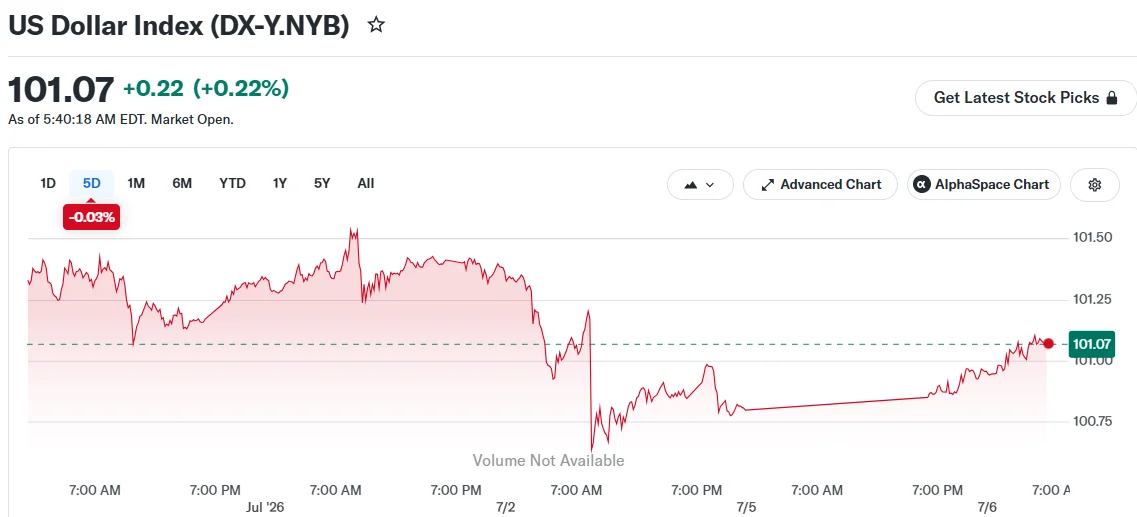

The greenback edged higher on Monday but continued trading near its two-week trough after last week’s disappointing U.S. employment data dampened speculation about additional Federal Reserve interest rate increases. Meanwhile, Japan’s currency remains perilously close to four-decade lows, keeping market participants vigilant for potential official intervention.

Greenback Weakens Following Disappointing Employment Report

The dollar gauge, measuring the currency against half a dozen major counterparts, traded around 100.9 during early Monday sessions. This followed a 0.5% weekly decline — marking its most significant weekly retreat since April.

The catalyst was June’s employment situation report, revealing substantially slower job creation. This development prompted questions regarding whether the Federal Reserve possesses sufficient justification for continued monetary tightening.

Nevertheless, declines remained limited. The jobless rate actually decreased, which OCBC currency strategists noted indicates continued labor market tightness. They retained their forecast of modest 2-3% dollar strengthening during the latter half of 2026.

The European currency stood at $1.1435, approaching a two-week peak. Britain’s pound traded at $1.3351. Both experienced approximately 0.1% Monday dips as the greenback regained some ground.

Declining oil prices have contributed to diminished inflation worries, which similarly factored into reduced rate-hike anticipation.

Market attention now turns toward the Federal Reserve’s June policy meeting minutes, scheduled for release later this week. Officials at that gathering reportedly adopted a more hawkish stance due to persistent inflation.

However, newly appointed Fed Chair Kevin Warsh has indicated the central bank has provided excessive forward guidance historically. Commonwealth Bank of Australia analysts cautioned the minutes may provide limited insight consequently.

Japanese Currency Near Four-Decade Low, Intervention Speculation Persists

Japan’s currency changed hands around 161.57-161.82 versus the dollar on Monday, barely removed from the 162.84 level reached last week — the weakest since 1986.

The Bank of Japan implemented a rate increase in June and hinted at potential additional tightening. Yet the substantial differential between American and Japanese borrowing costs continues exerting significant downward pressure on the yen.

Japanese authorities have issued verbal cautions against speculative yen weakness in recent weeks. Tokyo last conducted intervention operations in late April and early May, driving the dollar-yen exchange rate down toward 155. The pair rapidly rebounded above 160.

Currency analysts remain split on whether fresh intervention would produce enduring effects. OCBC strategists suggested intervention alone appears unlikely to alter the pair’s trajectory absent genuine shifts in underlying economic fundamentals.

ING analysts emphasized that more hawkish messaging from the Bank of Japan remains necessary to prevent dollar-yen from advancing further.

Marc Chandler of Bannockburn Global Forex observed that derivatives market activity indicates institutional investors have been purchasing short-dated dollar put options as insurance against unexpected intervention actions.

In other developments, South Korea’s won remained stable as Seoul initiated round-the-clock onshore dollar-won trading, representing progress toward achieving developed market classification on the MSCI index. China’s yuan and Singapore’s dollar both weakened marginally.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants