Eyes $14B US Listing Amid Surging AI Chip Demand")

Key Highlights

- SK Hynix submitted a confidential SEC filing for a 2026 US debut, potentially securing up to $14B in capital

- Company representatives report receiving exceptionally enthusiastic investor feedback regarding the planned US listing

- Strong HBM chip pricing dynamics anticipated to persist throughout the coming year

- Nvidia’s Vera Rubin platform LPDDR memory requirements may create supply constraints starting in 2027

- Intrinsic value analysis indicates shares trading at 47.3% below fair value, with current P/E of 21.58x against Fair Ratio target of 67.69x

SK Hynix (HXSCL) has been making the rounds with institutional investors, and the response has been decidedly bullish.

The memory semiconductor giant from South Korea shared with market participants this week that feedback on its US listing initiative has been “tremendously positive.” After submitting a confidential SEC filing in March, industry sources indicate the offering could generate as much as $14 billion in proceeds.

While SEC proceedings remain under review, the company acknowledged it cannot provide detailed updates at this stage. Management confirmed its intention to launch American Depositary Receipts sometime during 2026, though neither the exact scale nor precise timing has been finalized.

The investment thesis SK Hynix is presenting centers heavily on its strategic role within the artificial intelligence infrastructure ecosystem. As a leading producer of high-bandwidth memory solutions, the firm supplies critical HBM chips to Nvidia (NVDA). Its primary competitors in this specialized market include Samsung Electronics (SSNLF) and Micron Technology (MU).

Regarding HBM pricing trends, company officials indicated to investors that beneficial market conditions should extend through the next twelve months. Negotiations with major customers concerning future pricing for these sophisticated chips — essential components in AI accelerators — remain in progress.

Market Tightening Expected by 2027

Another significant development deserves attention. SK Hynix highlighted robust demand for LPDDR memory — low-power chips commonly deployed in mobile devices — from Nvidia for its upcoming Vera Rubin artificial intelligence platform.

According to the company, this demand trajectory could create supply constraints throughout the wider memory sector beginning in 2027. In anticipation, SK Hynix outlined plans to recalibrate capital expenditures and product allocation to optimize production capacity.

However, management provided a candid assessment: complete fulfillment of all anticipated demand cannot be assured, as projections suggest requirements will exceed available supply.

The Korean-listed shares (000660.KS) have delivered remarkable performance recently. The past month alone has seen gains of 58.2%. Year-over-year returns have been multiples higher — the kind of appreciation that naturally prompts questions about valuation.

Even after this significant rally, Simply Wall St’s valuation framework assigns the stock a score of 5 out of 6. A discounted cash flow model establishes intrinsic value at roughly ₩4,344,339 per share, suggesting current pricing represents a 47.3% markdown from that calculated figure.

Valuation Analysis

From a price-to-earnings perspective, SK Hynix currently carries a multiple of 21.58x. The broader semiconductor sector trades at an average of 24.42x, while the company’s peer group averages 71.00x. Simply Wall St’s proprietary Fair Ratio calculation for SK Hynix reaches 67.69x — substantially higher than present trading levels.

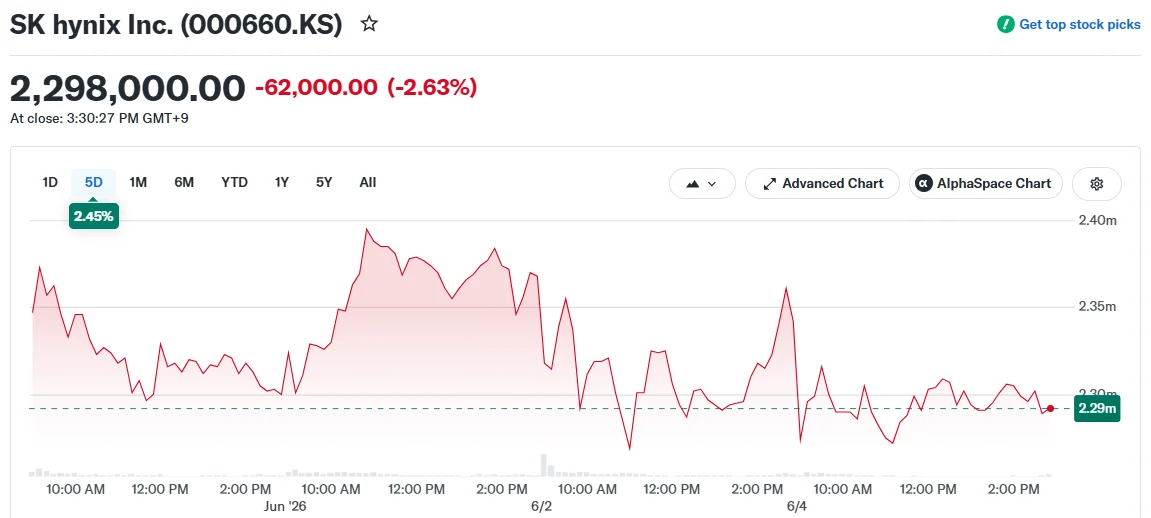

The HXSCL ADR experienced modest declines in recent sessions, mirroring the broader Korean equity market where 000660.KS dropped 2.63%.

SK Hynix maintains these trading levels as the SEC’s evaluation of its US listing application proceeds, with no definitive timeline established for regulatory approval or market debut.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants