TLDR:

- Moody’s downgraded U.S. debt from AAA to Aa1 on Friday, May 16, 2025

- Markets largely shrugged off the news with major indices closing flat or slightly up on Monday

- Treasury yields saw minimal movement despite the downgrade

- This follows similar market reactions to previous downgrades by S&P (2011) and Fitch (2023)

- Experts suggest corporate earnings, not credit ratings, are more important for stock market direction

On Friday, May 16, 2025, Moody’s became the third and final major credit rating agency to downgrade U.S. government debt, reducing it from AAA to Aa1. This completed a trifecta of downgrades after S&P’s action in 2011 and Fitch’s in 2023. Despite the news making international headlines, investors showed minimal concern in Monday trading.

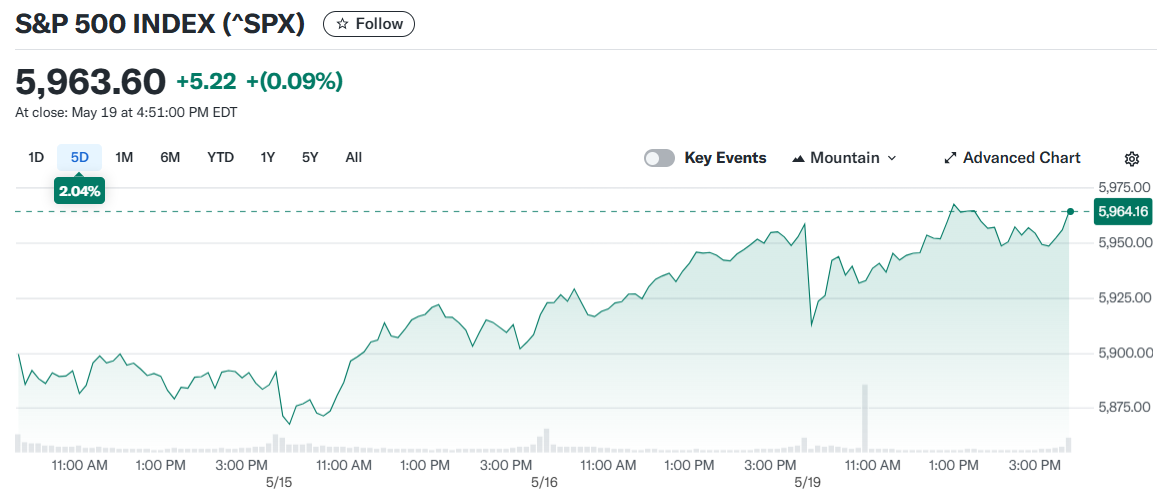

The major stock indices closed with small gains. The Dow Jones Industrial Average added more than 130 points (0.32%), while the S&P 500 rose 0.09% and the Nasdaq gained 0.02%. These modest increases suggest institutional and retail investors alike saw little reason for alarm.

Treasury markets, which would theoretically be most affected by a credit rating change, remained stable. The yield on the 10-year Treasury note climbed slightly to 4.46%, staying well below last month’s high of 4.59%.

“The downgrade itself doesn’t seem so far to have made much of a market splash,” noted analysts at Capital Economics. They pointed out that similar market reactions followed the previous two U.S. credit downgrades.

Impact on Consumers and Housing Market

While stocks and bonds showed resilience, the housing market felt some impact. Mortgage rates jumped, with the average 30-year fixed-rate loan reaching 7.04% on Monday—the highest level since April 11, according to Mortgage News Daily.

Matthew Graham, Chief Operating Officer at Mortgage News Daily, commented that lenders had to account for market movements from Friday’s closing minutes plus additional weakness Monday morning. However, he emphasized this jump “does very little to change the bigger picture” for mortgage markets.

Deficit Concerns Drive Downgrade

Moody’s cited America’s eroding fiscal control as the primary reason for the downgrade. “Successive U.S. administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” the agency stated in its announcement.

Budget experts, including the Congressional Budget Office and Penn Wharton Budget Model, have warned that current spending legislation working through Congress likely fails to address the fundamental fiscal problems facing the U.S.

Corporate Earnings May Matter More

Market analysts suggest investors would be wise to focus on corporate earnings rather than sovereign credit ratings when evaluating stocks. Morgan Stanley analyst Michael J. Wilson noted that “earnings revision breadth,” a measure comparing downward and upward earnings revisions by Wall Street analysts, has improved from -25% in mid-April to -15% currently.

“The combination of upside momentum in revisions breadth and last week’s deal with China has placed the S&P 500 firmly back in our pre-Liberation Day range of 5500-6100,” Wilson wrote.

Sectors showing the strongest rebounds include media and entertainment, materials, capital goods, and tech hardware. Meanwhile, consumer durables, autos, and consumer services continue to lag.

Retail Investors Remain Bullish

Individual retail investors appear to be providing crucial support for the market. These buyers have helped fuel the broader market recovery since President Trump’s “Liberation Day” tariffs announcement temporarily sent stocks tumbling.

A popular Vanguard investment instrument that serves as a proxy for retail buying remained flat on Monday, suggesting little appetite for selling among individual investors.

Economic Warning Signs

Despite the market’s apparent calm, prominent voices are raising concerns. JP Morgan CEO Jamie Dimon warned investors Monday that he believes the odds of stagflation—”basically a recession with inflation”—are roughly double what the market anticipates, a scenario he predicts would cause corporate earnings to decline.

Consumer sentiment has also weakened. On Friday, the University of Michigan reported its consumer sentiment index slipped to 50.8, the second-lowest reading in more than 40 years.

Citi analysts have been underweighting consumer stocks due to tariff policy risks. They note that while “a worst-case policy impact has seemingly been alleviated, recent signs of consumer slowing are concerning.”

White House Dismisses Concerns

The White House has pushed back against deficit worries. In a Monday call with reporters, officials dismissed concerns about the deficit, saying critics fail to account for potential growth from Trump’s economic policies, ongoing government spending cuts by the Department of Government Efficiency, and revenue from tariffs.

Some market observers remain skeptical of this optimistic view. Mike Goosay of Principal Asset Management noted that while “in the short run, the U.S. is still the world’s reserve currency and store of wealth,” the long-term outlook could change if “global investors start to question the U.S. role in the global order.”

The S&P 500 hit its all-time high of 6144 on February 19, 2025, and investors are watching closely to see if improving corporate earnings can drive the index back to those levels in the coming months.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants