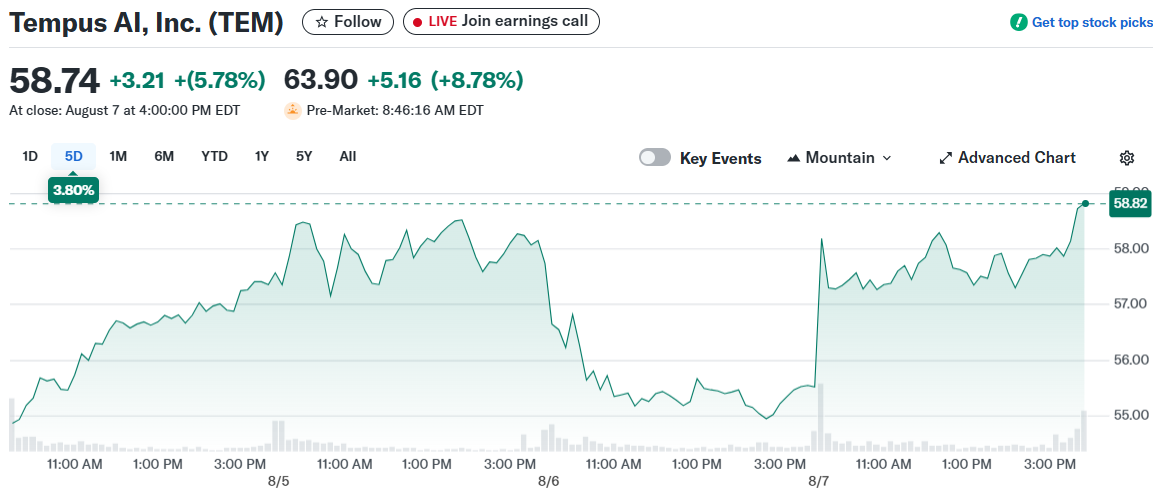

Stock Jumps 9% as Genetic Testing Volumes Surge")

TLDR

- Tempus AI reported Q2 EPS loss of $0.22, beating analyst expectations of $0.25 loss

- Revenue hit $314.6 million, surpassing consensus estimate of $297.8 million

- Genomics revenue jumped 115.3% year-over-year to $241.8 million

- Company raised full-year 2025 revenue guidance to $1.26 billion from $1.25 billion

- Stock surged 9% in premarket trading following the earnings beat

Tempus AI shares jumped 9% in premarket trading Friday following the company’s second-quarter earnings report. The genetic testing firm delivered results that exceeded Wall Street expectations on both earnings and revenue.

The company posted a loss of $0.22 per share for the quarter. This beat analyst expectations of a $0.25 loss per share.

Revenue came in at $314.6 million for the period. The figure topped the consensus estimate of $297.8 million.

The earnings beat was driven by strong performance across the company’s main business segments. Genomics revenue led the charge with impressive growth numbers.

Tempus AI continues to show monstrous growth. $TEM up 12% pre-market 🔥

EPS: (-0.22) vs (-0.25) est. ✅

Revenue: $314.6M vs $297.8M est. ✅

EPS up 65% YoY 💰

Revenue up 90% YoY 📈 pic.twitter.com/DGP6bGPbzb

— Farmer B (@BarmerFee) August 8, 2025

Genomics revenue surged 115.3% year-over-year to reach $241.8 million. This growth was powered by increased testing volumes in key areas.

Oncology testing volumes grew 26% during the quarter. Hereditary testing volumes expanded by 32% over the same period.

The company delivered more than 212,000 NGS tests during the quarter. This represented a 30% increase in clinical volumes.

Data Business Shows Strong Momentum

The data and services segment also delivered solid results. Revenue in this division rose 35.7% to $72.8 million.

The growth was supported by a 40.7% increase in Insights revenue. Insights represents the company’s data licensing business.

CEO Eric Lefkofsky highlighted the company’s improved financial performance. He noted that revenues and margins are growing faster than expected.

The company continues to show improvement in adjusted EBITDA on a year-over-year basis. This metric reflects the underlying profitability of the business.

Lefkofsky emphasized the company’s progress in artificial intelligence. He mentioned the development of what he called the largest foundation model in oncology.

Guidance Raised for Full Year

Management raised its full-year 2025 revenue guidance following the strong quarter. The company now expects revenue of $1.26 billion for the full year.

This represents an increase from the prior forecast of $1.25 billion. The new guidance also sits above the consensus estimate of $1.248 billion.

The company projects adjusted EBITDA of $5 million for the full year. This would mark an improvement of roughly $110 million compared to 2024.

Tempus approaches its 10th anniversary with what the CEO described as hitting their stride. The company has built a position in AI-powered precision medicine.

The strong quarter reflects growing demand for genetic testing services. Both oncology and hereditary testing showed robust volume growth.

The data licensing business continues to gain traction with customers. This segment provides higher-margin revenue compared to testing services.

Tempus delivered more than 212,000 NGS tests in the second quarter, representing 30% growth in clinical volumes as the company raised its full-year revenue guidance to $1.26 billion.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants