Whether you’re looking to invest a lump sum or save a bit at the end of each month – savings accounts allow you to earn guaranteed income. Although the yields on offer are typically very low, most savings accounts come with the benefit of FSCS protection. As such, the first £85,000 that you invest per institution is risk-free.

With that being said, how do you know which savings account to go with? Moreover, what do you do if you want to invest in multiple savings accounts, but don’t want to go through the hassle of opening and managing your money with several providers?

The answer could be Raisin – an online marketplace that allows you to invest in multiple UK savings accounts through a single provider.

The process works by signing up with Raisin, depositing funds, and then choosing which UK savings account you want to distribute your funds to. Crucially, all of the accounts that the platform has partnered with are FSCS protected, so your money is always safe.

Fancy finding out more about what Raisin is and how the platform works? If so, be sure to read our in-depth Raisin Review.

What is Raisin?

Launched in the UK in 2018, Raisin is an online marketplace that allows you to find the best savings account deals. However, unlike other savings marketplaces – which simply list the best deals, Raisin offers a proprietary account. By this, we mean that you can actually use the platform to invest money with your chosen savings account provider.

This is highlight beneficial, as it allows you to access multiple providers without needing to open an account with each one. Instead, you simply need to deposit funds into your Raisin account, and then you get to choose where you want to distribute the money.

For example, you might decide to invest 50% with Aldermore, 30% with ICICI Bank, and the remaining 20% with GateHouse Bank. Either way, all of the banks, building societies and credit unions that the platform has partnered with are FSCS protected.

As we noted above, this means that your money is 100% safe in the event the provider goes bust – up to the first £85,000. It is important to note that Raisin is not a bank or building society. On the contrary – it has partnered with UK challenger bank Starling. This allows it to collect and manage deposits on your behalf.

Nevertheless – and as we’ll cover in more detail further down, Raisin allows you to invest in a range of different saving accounts. This starts with short-term deposits at just three months, up to longer-term arrangements with a 5-year term.

The vast majority of accounts are fixed-rate accounts, meaning that you will be somewhat restricted in being able to withdraw your cash before the term matures. You’ll also have access to a small selection of notice accounts.

So now that you know what Raisin is, let’s take a look at how the process works in more detail.

How Does Raisin Work?

Signing up, depositing funds, and subsequently investing in savings account providers through Raisin is a seamless process. We’ve outlined the main step-by-step process below.

Step 1: Sign Up With Raisin

First and foremost, you will need to head over to the Raisin website and open an account. You will be required to fill in a range of personal information, much like you would when going direct with a UK savings account provider.

Why? Well, every time you decide to invest funds with a provider via Raisin, the platform will automatically forward your personal details on. This is great, as it means you are not required to open accounts manually.

Here’s what you’ll need to provide Raisin with:

- First and Last Name

- Home Address

- Time at Current Address

- Nationality

- Date of Birth

- Telephone Number

- Contact Number

Take note, when you apply for an account with Raisin, you are effectively opening an account with Starling Bank. This is because Starling is responsible for storing and managing your money. Furthermore, it’s likely that you will be sent an email from Raisin asking you to supply supporting documentation. This will usually need to be a copy of your passport or driver’s license.

Step 2: Browse Savings Accounts

Once your Raisin account has been opened and verified, you will then be able to browse the many savings accounts it has partnered with. We’ll unravel the different savings accounts that the platform hosts later, albeit, this covers a range of fixed and notice accounts – with both short-term and long-term plans covered.

You’ll be able to get a full breakdown of each savings account via Raisin, such as how much interest it pays, what the terms are on accessing your cash early, and what the lock-up period is.

Step 3: Transfer Funds Into Raisin

Once you have chosen a savings account that you like the look of, you will then need to deposit some funds into your Raisin account. Your account will come with a sort code and account number, much like a traditional current account.

You will then need to transfer the deposit amount from your personal bank account. This needs to be a nominated bank account that you will be asked to set up with Raisin. If in the future you decide to top-up your Raisin account with an alternative bank account, you’ll need to link it up via your account portal.

You also need to ensure that your transfer goes through the Faster Payments Network. Although the vast majority of UK banks and building societies offer this by default, a very small number of providers still use BACS and/or CHAPS. If this is the case, the transfer will be rejected.

You won’t be required to transfer the full amount in one go. For example, let’s say that you wish to invest £5,000 into a specific UK savings account. You could do this through multiple deposits until you reach the full amount, for example, two deposits at £1,500 and one at £2,000.

Step 4: Raisin Applies for Your Savings Account

Once your full deposit amount has been funded, Raisin will then apply to your chosen savings account provider on your behalf. As they already have your personal information, this means that you are not required to deal with the provider directly.

Instead, Raisin applies on your behalf, and will then inform you if the provider requires further information. In most cases, the information you have already submitted at Raisin will be sufficient.

Ultimately, you can repeat the above process as many times as you like. Every time you come across a new provider, all you need to do is enter the amount you wish to invest, and then transfer the funds into your Raisin account. In doing so, the platform will take care of the rest.

Types of Savings Account

On the one hand, Raisin has partnered with dozens of financial institutions in the UK, which gives you a decent amount of choice when it comes to browsing deals. However, Raisin is not currently offering any Easy Access accounts on its platform. Instead, you’ll need to choose from fixed-rate bonds or a notice account.

This is somewhat disappointing, as the platform won’t be suitable for those of you that want instant access to your cash as and when you see fit. With that said, Raisin does note that it is in the process of adding Easy Access accounts into its portfolio, although it doesn’t give an indication of when.

Nevertheless, let’s explore what savings accounts you can currently get through Raisin.

Fixed-Rate Savings Bonds

Fixed-rate savings bonds refer to savings accounts that offer a fixed rate of interest. Also referred to as a fixed deposit account, such accounts typically come with restrictions when it comes to accessing your cash. Ordinarily, you will need to agree to a minimum lock-up period.

At the time of writing, this starts at a minimum term of 3 months, up to a maximum of 5 years. In some cases, even though you are locked up to a minimum term when you choose your preferred fixed-rate savings account, some providers allow you to withdraw your money early.

However, in the vast majority of cases, you will be financially penalized for this. You will likely lose some, if not all of the interest that you would have otherwise earned had you waited for the term to mature.

Moreover, providers normally force you to close the entire account if an early cashout is required. As a result, you should only choose a term if you are 100% certain you won’t need to touch the funds before the maturity date.

Here’s the general gist of the fixed-rate savings accounts available at Raisin.

- Short-term accounts range from 3, 6, 9, and 12 months

- Long-term accounts range from 2, 3, and 5 years

- All interest yields are fixed for the entire term

- Most accounts cannot be touched until the term matures

- You will be financially penalized for accessing your money early, if applicable

Here are a few examples of fixed-rate savings bonds currently available through Raisin:

Aldermore – 3 months – 0.90% AER

The best deal available on a 3-month term is currently with Aldermore. You’ll get 0.85% AER, meaning that a £20,000 investment would yield £20,042.50. The account is protected by the FSCS, and no early withdrawals are permitted.

FCMB Bank – 2 Years – 0.88% AER

If you’re looking for a slightly better rate – and you’re happy to lock your funds away for 2 years, then the highest paying deal yields 1.75% AER. This means that a £10,000 investment would return £353.06 in interest. Backed by FCMB Bank, your money is 100% safe via the FSCS.

GateHouse Bank – 5 Years – 2.10% AER

If you’re looking for a slightly better rate – and you’re happy to lock order to get the highest paying yields with a fixed-rate savings account, you will need to lock your money away for 5 years. The best deal currently listed is with GateHouse Bank, which is paying 2.10% AER.

This would return £1,050 in interest over the course of the term, based on a £10,000 principal. Once again, your deposit is protected by the FCSC. The minimum investment is £1,000.

Notice Accounts

Notice accounts operate in a different manner to fixed-rate savings bonds, insofar that you will be able to make a withdrawal without being financially penalized. However – unlike an Easy Access account, notice accounts come with limitations.

At the forefront of this is that you will need to give a minimum amount of notice before you can actually access the funds. The best deals hosted by Raisin – at least in terms of yields, come with notice periods of up to 95 days.

This means that you would need to wait more than three months to get your money out, which is unlikely to be suitable in the event of a short-term financial emergency.

As such – and much like a fixed-rate savings account, only invest in a notice account if you are confident you won’t need the money before it becomes available.

It is also important to note that once notice has been given, the savings account provider will likely close your account. This means that you won’t be able to withdraw partial amounts. On the contrary, you are requesting the full amount – including earned interest, to be withdrawn.

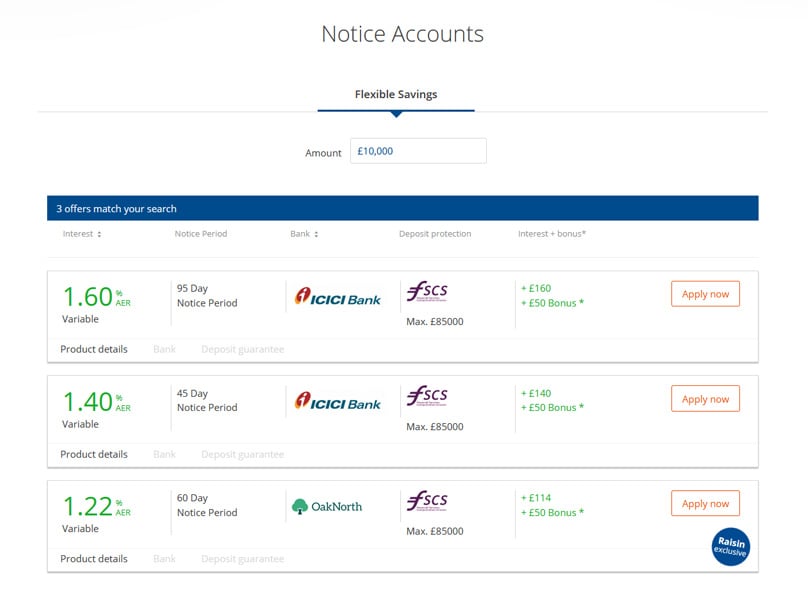

Here’s the general gist of the notice accounts available at Raisin.

- Just four notice accounts are available

- Providers include Cambridge & Counties Bank, OakNorth, and ICICI Bank – all FSCS partnered

- Notice period of either 45, 60, or 95 days

- Highest rate on offer is 1.60% AER (ICICI Bank, 95 days)

- Shortest notice period of 45 days also offered by ICICI Bank (1.40% AER)

- All notice period accounts come with a variable interest rate

Receiving Your Money Back Through Raisin

When it comes to getting your money back from a savings account investment, this will come in two forms – your principal and the interest yield. Regarding the former, this is the original amount that you invested into the savings account.

Fixed-Rate Account

If opting for a fixed-rate savings account, you will only get the principal back once the term matures. For example, if you invested £5,000 into a 3-year term, you will get the £5,000 back in 3-years time. In terms of your interest payments, this is usually paid at the end of each year.

For example, let’s say that you invested £10,000 into a 2-year term at 1.5% AER. In theory, this means that you will get £150 at the end of year one, and again at the end of year two. However, as the term also concludes after year two, you’ll also get your £10,000 back.

Notice Account

In the case of a notice account, you’ll get the principal amount back once notice has been given, and the notice period has concluded. For example, let’s say that you invested £4,000 into a savings account with a 60 day notice period. The date that you give notice is day 0, so you’d need to wait 60 days thereon before the funds are received.

In terms of the interest, this is usually paid on a monthly basis when opting for a notice account. Moreover, during the notice period, you will still earn interest on your deposit. However, you might need to wait an additional month post-maturity to get the funds.

How do I Receive the Principal and Interest?

Any payments that are owed to you will be sent to your Raisin account. As we discussed earlier, all Raisin customers will get a unique sort code and account number. As such, this is the account that the savings account provider will transfer both your principal and interest payments.

Once the money is in your Raisin account, you are free to withdraw it back to your personal bank account. Don’t forget, you need to set up a nominated account with Raisin – so if you’ve since changed bank accounts, you’ll need to link the new account.

Fees and Tax Deductions

On top of having the capacity to invest funds with multiple providers without needing to keep opening new accounts manually, Raisin also stands out for its fee-free service. As such, you won’t need to pay any fees when you make an investment. Instead, Raisin makes its money from the financial institutions that it has partnered with.

In terms of the tax on your interest payments, Raisin – nor the respective savings account provider, will deduct this for you. On the contrary, it is your responsibility to declare and pay any subsequent tax obligations that arise from your investments.

Note: If you’re a basic-rate taxpayer in the UK, you can earn up to £1,000 in savings interest without paying any tax.

Raisin Bonuses

From time to time, Raisin will offer new customers a bonus as a means to entice you to its platform. At the time of writing, this consists of a £200 welcome bonus.

| Account type | Deposit amount | Bonus amount |

| Fixed Rate Bond or Notice Account | £5,000 to £9,999 | £20 |

| Fixed Rate Bond or Notice Account | £10,000 to £39,999 | £50 |

| Fixed Rate Bond or Notice Account | £40,000 to £74,999 | £100 |

| Fixed Rate Bond or Notice Account | £75,000 to £85,000 | £200 |

The bonus funds will be deposited into your Raisin account, which you can then use to invest in a savings account of your choice. Take note, not everyone will be eligible for the bonus, as you’ll need to meet some minimum requirements.

For example, you need to apply for a savings account via Raisin and keep it active for at least 6 months. Moreover, you will need to deposit a minimum of £5,000 to qualify.

This is well worth considering if you have the means, not least because you will be able to boost your annualized yield.

Sharia Banking Options at Raisin

If you’re a follower of the Islamic faith, then you’ll know first-hand that charging interest is prohibited by the religion. With that said, Raisin now offers the option to open a Sharia-compliant account. It does so by offering products that come with an ‘expected profit rate’, as opposed to interest rates.

Although the profit rate is a target, Raisin will let you know if it expects the rate to change. If it does, you will have the option to close your account and receive your principal amount back, plus any profit that you’ve earned up to that point.

Customer Support at Raisin

Whether you already have an account with the platform or you simply want more information on its products and services, Raisin offers a number of support channels.

This includes a live chat facility for non-account related queries. You can email the team at service@raisin.co.uk, although Raisin notes that replies can take up to three business days.

This means that an email enquiry sent on Friday might not be replied to until Wednesday. As such, your best bet is to call Raisin directly on 0161 601 0000.

Raisin Review: The Verdict?

In summary, Raisin is well worth a closer look if you’re interested in investing money into a UK savings account. Not only will you be presented with some of the best deals currently available in the space, but Raisin gives you the opportunity to invest in multiple accounts at the click of a button.

Ordinarily, you would be required to open up and manage an account with each provider independently. However, by simply signing up with Raison, you can invest with as many providers as you see fit, with no requirement to apply yourself. Instead, Raisin will submit the application on your behalf with the information you provided during the registration process.

It is also notable that Raisin only deals with financial institutions that are partnered with the FSCS. This ensures that regardless of the savings account provider you go with, your money is always 100% safe – up to the first £85,000.

If we were to find fault with Raisin, it would have to be that the platform doesn’t currently offer Easy Access accounts. Although Raisin states that this is a work in progress, it remains to be seen when this will be offered.

Raisin

Pros

- Multiple Providers via Single Interface

- Exclusive Savings Deals

- Up to £200 Welcome Bonus

- FSCS Protection

- Easy to Use & Manage Savings

Cons

- Doesn't Cover Whole Market

- Online Only

- No Easy Access accounts

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants