TLDR

- NIO stock has surged 35% in the past month and 49% year-to-date, driven by strong demand for new SUV models including the ES8 flagship and Onvo L90

- Wall Street expects Q2 earnings on September 2 to show a loss of $0.31 per share on revenue of $2.73 billion, with Q2 deliveries up 26% year-over-year to 72,056 vehicles

- Two major analyst upgrades from JPMorgan and Macquarie moved NIO to “Buy” ratings, citing competitive pricing and upcoming product launches

- The company’s Battery-as-a-Service model and expanding swap station network (3,400 in China, 59 in Europe) are strengthening its market position

- Key catalysts ahead include Q2 earnings, NIO Day on September 20, and the Guangzhou Auto Show in November where the new Onvo L80 will be showcased

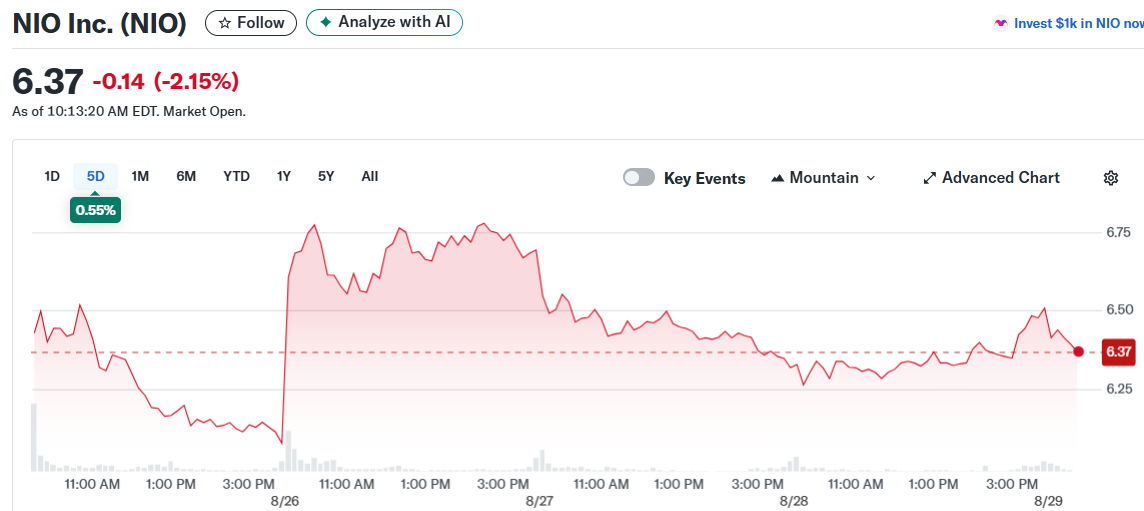

NIO stock climbed 2.68% on August 28 with trading volume reaching $480 million. The Chinese electric vehicle maker has posted gains of 35% over the past month.

The stock now sits 49% higher year-to-date. Strong demand for the company’s new SUV models has fueled the recent rally.

NIO’s Q2 deliveries reached 72,056 vehicles, marking 26% growth compared to the same period last year. The quarter-over-quarter jump was even more impressive at 71%.

The company’s sub-brands contributed to these numbers. Onvo delivered 17,081 vehicles while FireFly added 7,843 units to the total.

Analyst Upgrades Drive Optimism

JPMorgan analyst Nick Lai upgraded NIO to Buy from Hold this week. He raised his price target to $8 from $4.80.

Lai placed the stock on “positive catalyst watch” ahead of several key events. These include Q2 earnings, NIO Day on September 20, and the Guangzhou Auto Show starting November 21.

The analyst expects the company to showcase its upcoming Onvo L80 at the auto show. This new 5-seater SUV will compete directly with Tesla’s Model Y.

Macquarie analyst Eugene Hsiao also upgraded NIO to Buy from Hold. He believes the L90 model at RMB 265.8k offers strong value compared to competitors.

Hsiao sees the L90 as particularly competitive against Li Auto’s i8 model. The NIO vehicle offers similar features at a 17% lower entry price.

The analyst raised his volume estimates for NIO. He now expects 347,000 deliveries in 2025 and 500,000 in 2026.

Strategic Moves Support Growth

NIO’s Battery-as-a-Service model continues to attract customers. The approach reduces upfront costs while creating recurring revenue streams for the company.

The battery swap network has expanded to 3,400 stations in China. An additional 59 stations operate across Europe.

This infrastructure addresses range anxiety concerns that often deter EV buyers. The swap stations provide a competitive edge in the crowded Chinese market.

Recent price cuts across NIO’s long-range lineup reflect the competitive pressure. The company reduced prices to compete with Tesla’s new six-seat Model Y L SUV.

Wall Street expects NIO to report a Q2 loss of $0.31 per share when results are released September 2. Revenue is forecast at $2.73 billion for the quarter.

The consensus rating remains Moderate Buy based on four Buy ratings, six Holds, and one Sell. The average price target of $5.19 suggests 20.3% downside from current levels despite recent analyst upgrades.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants