Moneybox aims to make investing easy for the average person. The platform consists of an application that you download onto your smartphone.

The application then helps you automatically save money in small quantities that you are unlikely to even notice. Instead of just letting that saved money sit in a savings account, Moneybox invests it, so you can experience a more dramatic increase in wealth.

There are multiple choices for risk level, and this method is designed to help the average person begin investing with minimal knowledge.

Moneybox launched in 2016 with a team of marketers, entrepreneurs, developers, and designers who have a proven track record of assisting others with money management and building mobile applications. The co-founders are Ben Stanway and Charlie Mortimer.

How Does Moneybox Work?

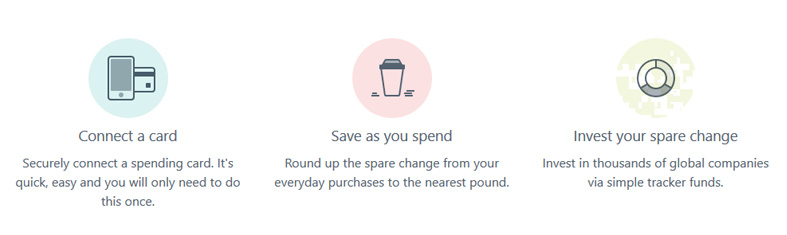

With Moneybox, you automatically round all purchases up to the next pound. Then, the difference between the actual price and what you pay gets stored in a Stocks and Shares ISA. Moneybox advertises that you can start investing in major companies with as little as £1 in your account.

To start using Moneybox, you just connect your chosen card to the Moneybox application. The application will automatically take care of the rounding up of purchases for you, so you can invest the spare change.

Read: What is a Stocks and Shares ISA?

How Do You Add Money to Your Stocks and Shares ISA?

The Moneybox application will automatically add funds to your Stocks and Shares ISA as you use your card, so you do not have to do anything. You just let the application round up the purchases and invest the change. If you want to speed up the investing process, you can also contribute to the Stocks and Shares ISA with a one-time payment or via weekly deposits.

What Investing Options Does Moneybox Offer?

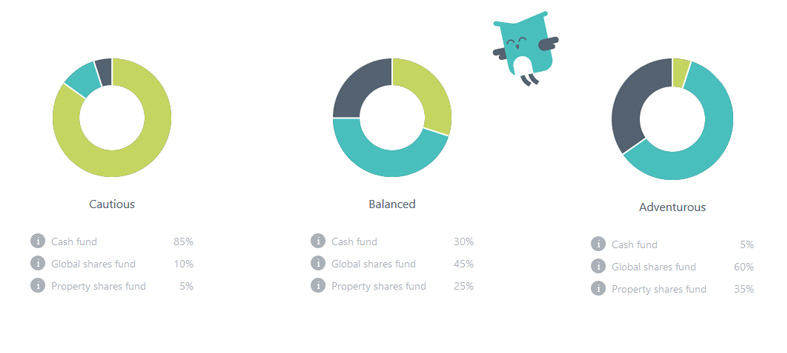

When you set up Moneybox, you will be able to choose from three different trading options with varying levels of risk, known as “Cautious,” “Balanced,” and “Adventurous.”

Each of these options includes investments in the same three different tracker funds: a cash fund, a global shares fund, and a property shares fund. The difference is the proportion of the investment allocated to each fund.

- With the Cautious approach, 85 percent of the investment goes to the cash fund, 10 percent goes to the global shares fund, and 5 percent goes to the property shares fund.

- The Balanced approach divides it with 45 percent to the global shares fund, 30 percent to the cash fund, and 25 percent to the property shares fund.

- Finally, the Adventurous option puts 60 percent in the global shares fund, 35 percent in the property shares fund, and 5 percent in the cash fund.

What Kind of Performance Do the Funds Deliver?

Investment always has an element of risk, and past performance does not relate to current performance in any way, nor does it predict it.

Even so, Moneybox does offer examples of how much £1,000 initially invested in 2007 with each approach, plus £50 added monthly, would be worth at the end of 2016.

This would be worth £7,963 with the Cautious approach, £10,899 with the Balanced approach, or £12,322 with the Adventurous approach.

Remember that those figures just show a single situation to give you an idea of the differences between the various options and in no way indicate what Moneybox users will actually experience.

How Do You Open a Moneybox Stocks and Shares ISA?

Only those who are UK tax residents and at least 18 years old can open a Moneybox Stocks and Shares ISA. To sign up, download the application on your mobile device then enter your bank details, so you can set up the direct debit function.

If you plan to take advantage of roundups, you will also need your credit card or online banking details. If you are opening a Stocks and Shares ISA, you will also need to enter your National Insurance Number; it is not needed for opening a GIA.

Remember that you can only have a single profile with Moneybox. If you choose to set up a Junior ISA, you can use the same profile as your Stocks and Shares ISA.

It is possible to transfer a current ISA to Moneybox or to transfer Moneybox to another ISA, both of which require filling out forms.

Are there Investment Limits for the Moneybox ISAs?

For the 2022-23 tax year, you can contribute a maximum of £20,000 to an ISA. There is no annual limit for investing in GIAs but a weekly limit of £20,000.

The minimum to begin is just £1, making Moneybox very accessible. All withdrawals and deposits for your Moneybox account are done via direct debit.

What Is the Junior ISA?

In addition to the standard Stocks and Shares ISA, Moneybox offers a Junior Stocks and Shares ISA, also called the Junior ISA. This type of account works nearly identically to the standard Stocks and Shares ISA.

You link a card then round up purchases to the next pound and save the change, investing it in more than 6,000 companies via tracker funds. The main difference is that this particular offering is designed to help you save money for your child’s future.

You get the same three choices of Cautious, Balanced, and Adventurous; the same fees; and the same regulation and security.

The only real difference between a Junior ISA and the standard ISA is that Junior ISAs are opened on behalf of those under 18 years old. Each Junior ISA can only have the name of a single child, which means that you can open multiple Junior ISAs if you have multiple children.

What Do You Need to Open a Junior ISA?

To open a Junior ISA, you need to provide your name, date of birth, mobile number, residential address, and email address. You must also provide the child’s name, date of birth, National Insurance Number (when known), and residential address.

What Else Should You Know about Junior ISAs?

Moneybox has an extensive FAQ section with more information on Junior ISAs, but the accounts are fairly straightforward. To open a Junior ISA for your child, you must live in the United Kingdom, be at least 18 years old, and have parental responsibilities for a child under 18.

That child must not have a Child Trust Fund or a Junior Stocks and Shares ISA and must also be a UK resident. If your child already has a Junior Stocks and Shares ISA, you must transfer it into the new Moneybox Junior ISA. When you open a Junior ISA on behalf of your child, you manage it until they turn 18 and are the “Registered Contact.”

At the moment, only a Registered Contact can contribute to a Moneybox Junior ISA. Soon, however, the platform will let others contribute, including grandparents, family, and friends. All contributions are gifts, so they are not returnable.

The minimum contribution for a Moneybox Junior ISA is £1 with a maximum annual contribution of £4,260 in accordance with HM Revenue and Customs. Since the funds in a Junior ISA belong to the child, it has no impact on your own ISA allowance.

You can choose to cancel a Junior ISA within 30 days of opening it. In the case where you already invested assets before canceling, you will get back the original contribution with any shortfalls already subtracted. If profits were made, you still receive the original contribution.

As Junior ISAs are for the child they are registered under; you cannot withdraw money from them. Only the child can withdraw that money, and they must reach age 18 to do so. The child automatically takes control of the account at age 18, at which point it converts into a Stocks and Shares ISA.

What Is a Lifetime ISA?

Another option is a Moneybox Lifetime ISA. With this type of account, you can save as much as £4,000 annually and receive a 25 percent government bonus. Those bonuses can be a significant advantage for those who open a Lifetime ISA.

Keep in mind that Lifetime ISAs are new products that the government designed and are intended to be used to buy your first home or for retirement.

If you withdraw money from the Moneybox Lifetime ISA for any reason that is not purchasing a first home or retiring past age 60, you pay 25 percent in the form of a government charge. Between the bonus and this 25 percent charge, the result is that withdrawing for an unsupported reason makes you lose £6.25 for every £100 you invest without accounting for fees, losses, or gains. This charge does not apply to those who are terminally ill.

There are also a handful of other governmental restrictions on Moneybox Lifetime ISAs. The first home that you save for with this type of account must not have a value of over £450,000. If you and another first-time buyer purchase a home together, you can both use your Lifetime ISAs, but that home value limit does not change. Account holders need to be UK tax residents and cannot be U.S. citizens. They must be between the ages of 18 and 39 at the time of account opening, and they can only contribute until age 50. Lifetime ISAs have the same fees, security, and regulation as other Moneybox ISAs.

It is possible to transfer from a Moneybox Stock and Shares ISA into a Moneybox Lifetime ISA. You can have more than one ISA but can only pay into one of each type per tax year. Lifetime ISAs have a maximum annual contribution of £4,000, and all ISAs combined have a maximum of £20,000. Keep in mind that you can have both a Lifetime ISA and a Help to Buy ISA but are only able to use the bonus from one to buy a home.

What Platforms Does Moneybox Offer?

You cannot access Moneybox via its website. Instead, you must do so via one of the mobile applications. There are separate applications for Moneybox and Moneybox Junior ISAs. Moneybox is already available for Android and Apple, while Moneybox Junior ISA is currently only available for Apple with a waiting list for Android.

What Fees Does Moneybox Charge?

Moneybox charges minimal fees, but as this is its source of profit, it does need to charge something. There is a £1 subscription fee that is charged every month, with the first three months free. There is also a 0.45 percent platform fee that is charged annually and billed monthly but no fees for transactions or trading. There are also fund provider fees billed monthly but charged annually at 0.23 percent on average. You will not find a fee from Moneybox to exit or withdraw. The only exception is the rare case where clients transfer out in specie, in which case there is a £25 fee per holding.

Is Moneybox Regulated?

To give customers peace of mind, Moneybox is authorized as well as regulated by the Financial Conduct Authority (FCA). Additionally, investments have protection from the Financial Services Compensation Scheme (FSCS). This FSCS protection means that if Moneybox or a product provider declares bankruptcy, investments are covered up to £50,000. It is important to note that the FSCS protection does not apply to declines in the value of an investment.

How Does Moneybox Provide Security?

To ensure all information remains secure, Moneybox uses 256-bit TLS encryption on all personal information. Additionally, Moneybox never shares client details with third parties without first receiving consent to do so.

If your mobile device gets stolen or lost, you can contact the support team, who will suspend your account for you.

How Do You Contact Moneybox Customer Support?

You can contact Moneybox customer support directly via the chat function of the application. Alternatively, you can email the support address.

Conclusion

Moneybox is a solution for UK tax residents that helps them seamlessly save and start investing with minimal effort. It is an application for smartphones that lets you save money into a Stocks and Shares ISA, Lifetime ISA, or Junior ISA, via both direct deposits and rounding up purchases. Moneybox is regulated by the FCA and is protected under the FSCS.

Moneybox is a great way to get started with investing if you have no prior experience, the app is very easy to setup and use and offers a range of ways to add money to your account with them. The ability to roundup purchases made with your debit card is a nice feature which should add to your pot, but we recommend you setup a weekly or monthly payment as well and maybe also use their “Payday Boost” to add a little extra.

ISAs are a great way to save money for UK citizens as your profits will be tax-free.

Of course, it should be noted that the value of your investments can also go down as they rely on the stock markets.

MoneyBox

Pros

- Simple Easy to Use App

- Able to Set Risk Level

- Great for Beginner Investors

- FCA Regulated

Cons

- Capital at Risk

- UK Residents Only

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants

1 Comment

LOVE this. Microinvesting apps – especially the ones that round up your change – are something I’m really interested in right now. I’ve seen several pop up on the market, and so far no single one has stood out to me.

I do like that this one has in-app chat support, and that you can open an account for a child. Those are both noteworthy details. I’m going to have a look at a few more before I decide on one, but thanks for this review, super helpful!