Stock: Why This Analyst Sees 50% Crash Coming")

TLDR

- Monness analyst maintains Sell rating with $175 price target, implying 50% downside potential

- Company’s premium over Bitcoin holdings has compressed from 1.8x to 1.34x

- $3.4 billion in high-interest bond offerings create pressure on equity holders

- Stock fell 3.73% in pre-market trading following negative analyst coverage

- Despite concerns, Wall Street consensus remains Strong Buy with $575.83 average target

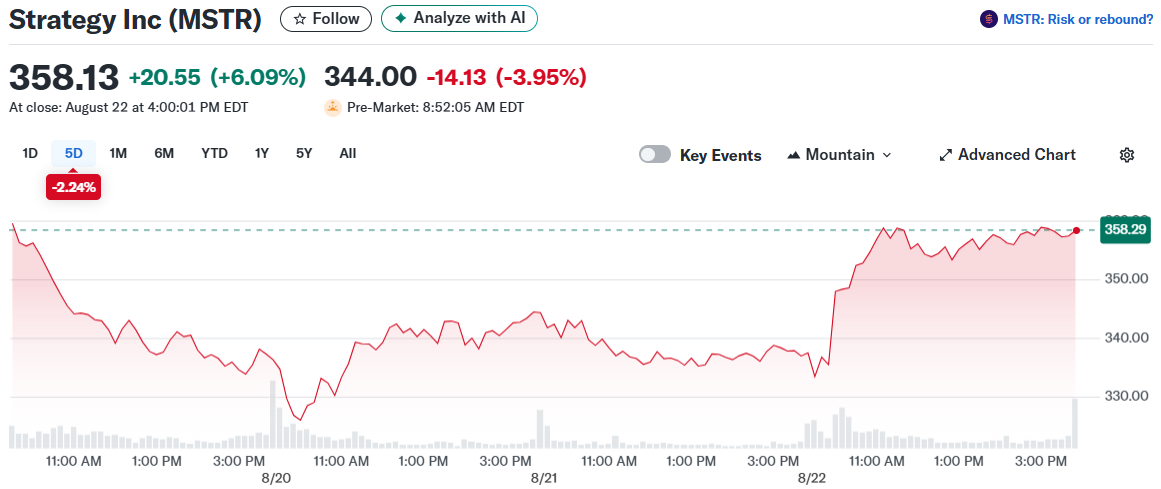

MicroStrategy’s stock took a hit in pre-market trading on August 25, falling 3.73% after analyst warnings about the company’s valuation premium. The decline came as investors questioned whether the Bitcoin proxy stock can maintain its elevated trading multiple.

Monness analyst Gus Gala kept his Sell rating on MSTR with a $175 price target. This represents about 50% downside from current levels. Gala warned that the company’s premium over its Bitcoin holdings has room to shrink further.

The stock has delivered strong returns over the past year, climbing 152% and gaining 16% year-to-date. However, Gala sees mounting risks in the company’s funding approach and valuation metrics.

Funding Model Creates Shareholder Risks

MicroStrategy’s “42/42 Capital Plan” relies heavily on convertible debt and bond offerings to finance Bitcoin purchases. The company has issued about $3.4 billion in bonds as convertible debt becomes less attractive due to lower volatility.

These bond deals carry high interest costs that put pressure on equity holders. Gala expects the company will continue issuing new shares to fund Bitcoin acquisitions since traditional debt markets remain limited.

This approach creates dilution for existing investors. The constant share issuance weighs on the stock’s valuation multiple over time.

The analyst noted that MicroStrategy’s strategy is no longer unique. More companies are adopting similar Bitcoin treasury models, reducing the company’s competitive advantage.

Premium Compression Continues

The stock’s premium to its Bitcoin holdings has already started shrinking. MSTR’s multiple fell to 1.34x from a recent peak of 1.8x, though it still trades above the peer group median of 1.21x.

Gala stressed that this valuation pressure will likely persist. The heavy reliance on stock issuance creates downward pressure on the multiple, limiting potential gains for shareholders.

Bitcoin’s price movements are increasingly driven by broader economic factors rather than company-specific actions. This leaves MicroStrategy more exposed to general market swings beyond its control.

The pre-market decline on August 25 reflected investor concerns about the company’s performance relative to Bitcoin’s recent rally. Some questioned why MSTR wasn’t keeping better pace with the cryptocurrency’s gains.

Despite the negative analyst coverage, MicroStrategy maintains its focus on Bitcoin investment. The company continues to hold its position as a leader in corporate crypto reserves.

Wall Street analysts remain divided on the stock’s prospects. The consensus rating stands at Strong Buy based on 11 Buy recommendations and one Sell rating from the past three months.

The average price target of $575.83 implies 70.58% upside potential from current trading levels. This contrasts sharply with Gala’s bearish outlook and $175 target price.

MicroStrategy’s stock closed the previous session with gains but faced pressure in extended trading following the analyst note publication.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants