Stock: Wall Street Gets Excited About Wednesday’s Big Reveal")

TLDR

- Micron reports fiscal Q3 earnings Wednesday with analysts expecting profits to more than double year-over-year

- Revenue projected at $8.85-8.86 billion, up 30% from last year, driven by AI and data center demand

- Wells Fargo and Wedbush both raised price targets to $150 ahead of earnings

- Stock has surged 46% year-to-date and over 30% in the past month

- Company announced $200 billion U.S. investment plan for manufacturing and R&D

Micron Technology prepares to release its fiscal third-quarter earnings Wednesday after market close. Wall Street expects the memory chip maker to deliver strong results driven by artificial intelligence demand.

Analysts project revenue of $8.85 to $8.86 billion for the quarter. This represents a 30% increase from the same period last year. The company’s adjusted earnings per share are expected to reach $1.59 to $1.61.

These numbers would more than double last year’s results of $0.62 per share. The dramatic improvement reflects the recovery in memory chip markets and growing AI infrastructure needs.

Micron’s stock has responded positively to these expectations. Shares have gained 46% year-to-date and jumped over 30% in just the past month. The stock closed Friday at $123.60.

The memory maker benefits from partnerships with major tech companies. Nvidia serves as a key partner, helping drive demand for high-bandwidth memory products. Data center sales have been particularly strong, with previous quarters showing triple-digit growth.

Tech giants like Microsoft, Meta, and Amazon continue expanding their AI data centers. This creates sustained demand for Micron’s specialized memory products. High-bandwidth memory has become essential for AI applications and machine learning workloads.

Analyst Upgrades Signal Confidence

Wells Fargo analyst Aaron Rakes recently raised his price target from $130 to $150. He expects the Q3 results to show continued strength in data center and AI-driven DRAM demand. Rakes maintains his positive outlook despite some weakness in NAND flash memory.

Wedbush also increased its price target to $150 while maintaining a Buy rating. The firm sees improving memory pricing trends supported by stronger enterprise and server demand since April. Wedbush expects both DRAM and NAND pricing to improve in coming quarters.

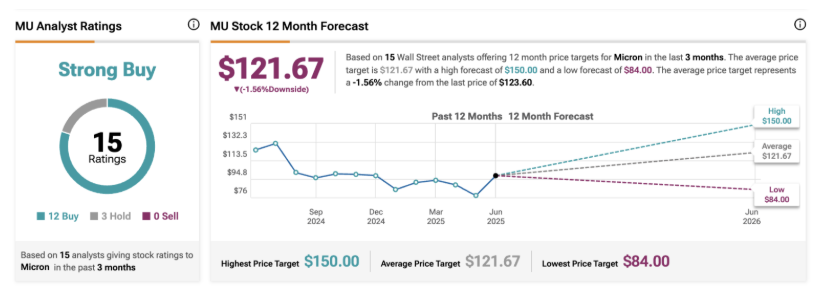

Of 11 analysts tracked by Visible Alpha, nine rate Micron stock a “buy.” Two analysts maintain “hold” ratings. The consensus price target sits near $121, slightly below current trading levels.

The positive analyst sentiment comes after strong results in March. Micron’s previous quarter topped revenue expectations thanks to data center sales growth. AI demand drove much of this performance.

Investment Plans Support Growth

Micron announced plans to invest $200 billion in U.S. operations earlier this month. The company will spend $150 billion on memory manufacturing and $50 billion on research and development. Most funds will support new fabrication facilities across multiple states.

Micron To Invest $200 Billion In America To "Reinforce" Global Chip Dominance | ZeroHedge

Micron Technology announced massive plans to expand its U.S. investments to $200 billion—allocating $150 billion toward domestic memory manufacturing and $50 billion to R&D—across Idaho,… pic.twitter.com/4zNoRF1e5o

— Owen Gregorian (@OwenGregorian) June 13, 2025

The investment includes two new high-volume fabs in Idaho. Up to four additional fabs are planned for New York. The company will also expand and modernize its existing Virginia facility.

These facilities will focus on leading-edge memory production. Micron plans to advance its high-bandwidth memory packaging capabilities as part of the expansion. The investment timeline spans multiple years.

The semiconductor industry has seen increased government support for domestic manufacturing. Micron’s plans align with federal initiatives to strengthen U.S. chip production capabilities.

Memory pricing has shown signs of stabilization after a difficult period. Industry observers note improving supply-demand balance across memory categories. This trend supports revenue growth expectations for the coming quarters.

Wall Street maintains a Strong Buy consensus on Micron stock based on 12 Buy ratings and three Hold ratings assigned in recent months.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants