Stock: Wall Street Raises Targets ahead of Tuesday’s Earnings")

TLDR

- Micron reports Q4 earnings Tuesday with analysts expecting $2.86 EPS on $11.2 billion revenue, up 45% annually

- Company raised guidance in August due to strong AI data center demand for high-bandwidth memory

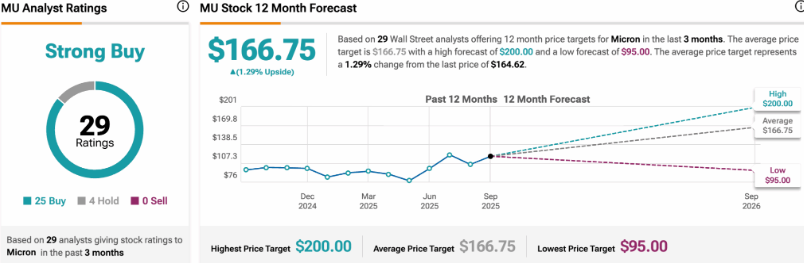

- 10 analysts raised price targets last week, with shares up 38% in September to $164.62

- Memory pricing expected to continue rising despite being deep in traditional cycle

- Wall Street consensus shows 25 buy ratings out of 29 analysts covering the stock

Memory maker Micron faces high expectations as it reports fourth-quarter earnings Tuesday afternoon. The company already surprised investors in August by raising guidance mid-quarter.

Wall Street expects adjusted earnings of $2.86 per share on revenue of $11.2 billion. This represents a massive jump from last year’s $1.18 per share earnings.

The AI investment boom has changed everything for memory companies. Traditional cycles brought sudden swings in demand and painful price drops.

This time looks different. AI data centers need premium memory products that carry better margins.

Micron raised its Q4 guidance just two months after issuing initial projections. This unusual move signaled demand was running ahead of plan.

Memory Pricing Defies Traditional Patterns

TD Cowen analyst Krish Sankar reported that memory prices should keep rising in coming quarters. This breaks the usual pattern where prices drop deep into an up-cycle.

Ten analysts raised price targets in the past week alone. The average target now sits at $166.44, just above current trading levels.

Shares climbed 38% in September to $164.62. This rally has priced in strong results and raised the bar for Tuesday’s report.

AI training requires stacks of high-bandwidth memory next to processors. This design shift altered the demand curve for memory suppliers.

Instead of relying on PCs and phones, Micron now ships more bits into data centers. These buyers value bandwidth and power efficiency over cost alone.

Supply Stays Tight Despite Two-Year Rally

Reports through September show tight supply in DRAM and improving trends in NAND. High-bandwidth memory remains the standout performer.

This backdrop explains why Micron felt confident lifting guidance in August. Companies rarely raise projections just weeks before quarter end unless results locked in better than expected.

The revenue mix has shifted upward and pricing discipline has strengthened. Inventory stayed leaner and buyers signed forward agreements to secure supply.

Investors want confirmation that pricing power lasts into 2026. Average selling prices, bit shipments, and gross margins will provide key clues.

If HBM ramps stay on schedule and yields improve, the pricing thesis gets stronger. Any cooling in pricing or higher costs could trigger a pullback.

The first-quarter outlook matters just as much as Q4 results. Street models look for $11.9 billion in Q1 revenue, up more than one-third from last year.

Management comments on capacity, customer visibility, and HBM supply will set the tone. Clarity on capital expenditures and manufacturing transitions also matters.

The competitive landscape stays in focus. Disciplined supply from peers and expanding cloud agreements would support margins.

Out of 29 analysts covering Micron, 25 rate it a buy and four call it a hold. None recommend selling the stock.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants