Stock: Rallies as Investors Rush In Before Make-or-Break Earnings Report")

TLDR

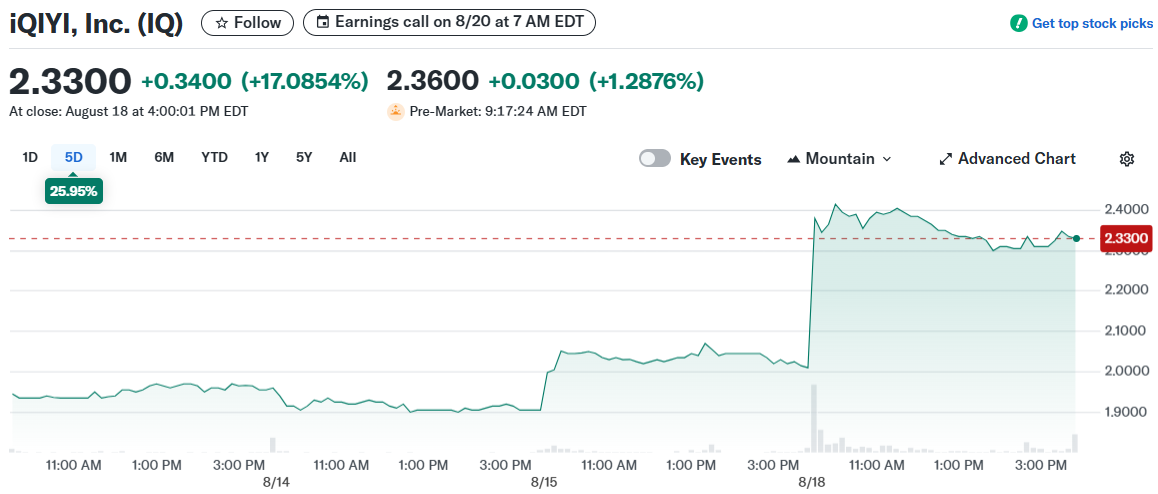

- iQIYI stock jumped 10% in pre-market trading on August 18, ahead of its Q2 earnings report scheduled for August 20

- CLSA upgraded the stock from Hold to Outperform, raising price target to $2.45 from $1.70 due to improved regulatory outlook in China

- The analyst expects Q2 revenue to decline 11% year-over-year to 6.6 billion yuan, with membership revenue dropping 9%

- Advertising revenue likely fell 13% during the quarter due to weak demand during the 618 shopping period

- Content costs expected to remain flat at 3.79 billion yuan, pressuring gross profit margins lower

iQIYI stock rocketed 10% in pre-market trading on August 18, 2025. The Chinese streaming platform caught investor attention ahead of its second-quarter earnings report.

The company is set to announce Q2 2025 results on August 20. Trading volume spiked as investors positioned themselves before the earnings release.

CLSA analysts upgraded iQIYI from Hold to Outperform on August 19. They raised their price target to $2.45 from $1.70, representing a 44% increase.

The upgrade reflects CLSA’s removal of a 20% valuation discount. This change stems from potential regulatory relaxation in China’s streaming sector.

Revenue Pressures Expected in Q2

CLSA expects total revenue to decline 11% year-over-year to 6.6 billion yuan. Membership revenue is projected to drop 9% year-over-year to 4.1 billion yuan.

The revenue decline comes from reduced premium content during the traditional low season. Fewer blockbuster releases typically hurt subscriber growth and retention.

Advertising revenue likely fell 13% year-over-year during the quarter. Weak demand for performance ads during the 618 shopping period hurt results.

Brand advertising revenue may have recovered quarter-over-quarter. Popular variety shows like Kings of Comedy helped drive advertiser interest.

Content Costs Remain Elevated

Content costs are expected to stay flat quarter-over-quarter at 3.79 billion yuan. This level of spending will pressure gross profit margins.

CLSA projects gross profit margin to hit 20.6% in Q2. This represents a decline of 3 percentage points year-over-year and 4.2 percentage points quarter-over-quarter.

The company faces a balancing act between content investment and profitability. High-quality content drives subscriptions but weighs on margins.

Second-quarter adjusted operating profit is projected at 80 million yuan. This marks a sharp decline from 501 million yuan in the same period last year.

The profit drop reflects the challenging operating environment for Chinese streaming platforms. Competition remains fierce while content costs stay elevated.

CLSA maintains its 2025 adjusted operating profit forecast at 1.08 billion yuan. The firm expects sequential improvement supported by upcoming drama and film releases.

The analyst upgrade suggests growing confidence in iQIYI’s regulatory environment. Chinese authorities appear to be easing pressure on tech companies.

The stock currently trades at $2.33 with a market capitalization of $1.92 billion. It has posted a 25.95% return over the past week, showing strong momentum.

iQIYI reported first-quarter revenue that exceeded analyst expectations earlier this year. However, earnings fell short of forecasts, creating mixed investor sentiment.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants