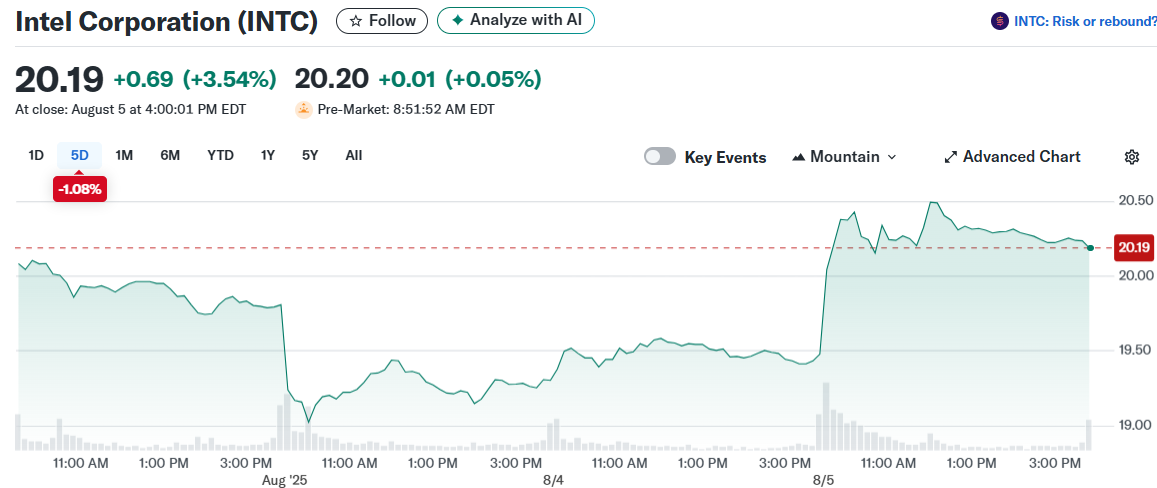

Stock: Climbs 3% as Investors Shrug Off Credit Downgrade")

TLDR

- Intel stock jumped over 3% Tuesday despite Fitch downgrading credit rating from BBB+ to BBB

- Fitch cited weak demand environment and constrained profitability growth as key concerns

- Credit recovery expected to take 12-24 months with stronger markets and successful product launches

- Intel’s 18A manufacturing process faces defect issues with Panther Lake chips showing three times expected problems

- Wall Street maintains Hold consensus with average price target of $22.25 implying 9.96% upside

Intel stock defied logic Tuesday, surging over 3% while getting slapped with a credit downgrade from Fitch Ratings. The chipmaker saw its long-term issuer default rating dropped from BBB+ to BBB.

Fitch kept the negative outlook in place, pointing to ongoing demand weakness. The rating agency said Intel’s credit profile remains under pressure from market headwinds.

The downgrade reflects a “more challenging demand environment than previously anticipated.” This environment is squeezing Intel’s profitability growth, Fitch analysts explained.

Despite the rating cut, investors seemed to focus on other factors. The stock rally suggests optimism around Intel’s strategic shifts in the foundry business.

Fitch acknowledged Intel’s updated foundry strategy as a positive move. The company now ties capital spending directly to customer demand, which the agency views favorably.

However, the road to recovery won’t be quick. Fitch estimates Intel needs 12-24 months to restore its credit metrics to acceptable levels.

Manufacturing Headaches Mount

Intel faces fresh challenges with its 18A manufacturing process. The upcoming Panther Lake chips are showing defect rates three times higher than expected.

This news adds to earlier reports about volume production issues with the 18A process. Intel planned to launch Panther Lake in the fourth quarter of this year.

The timing couldn’t be worse for Intel’s recovery plans. Fitch specifically mentioned that successful product launches are crucial for the company’s credit improvement.

The 18A process represents Intel’s attempt to regain manufacturing leadership. Technical setbacks here could derail broader turnaround efforts.

Market Response and Analyst Views

The stock’s positive reaction puzzled many observers given the mixed news flow. Investors may be betting on Intel’s long-term strategy despite near-term challenges.

Wall Street analysts maintain a Hold consensus rating on Intel shares. The rating is based on one Buy, 25 Holds, and three Sells from the past three months.

The average price target sits at $22.25 per share. This implies 9.96% upside potential from current levels.

Intel shares have declined 1.66% over the past year. The stock has struggled with competitive pressures and execution issues.

Fitch noted that credit metrics remain weak across the board. The agency wants to see both stronger end markets and successful product ramps before considering rating improvements.

The foundry strategy shift shows promise but carries execution risks. Intel must deliver on both technology and customer commitments to succeed.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants