Earnings Propel Tech Stocks Higher Amid Middle East Tensions")

Key Takeaways

- Intel delivered an exceptional first-quarter earnings performance, driving shares to unprecedented levels

- Major indices showed mixed results: Nasdaq climbed 0.7%, S&P 500 advanced 0.3%, Dow Jones declined 0.3%

- Semiconductor stocks extended their winning streak to an unprecedented 18 consecutive sessions

- Crude oil markets showed signs of relief as diplomatic hopes emerged regarding US-Iran relations

- Cryptocurrency markets weakened amid persistent Middle Eastern geopolitical concerns

Intel delivered impressive first-quarter financial results that exceeded analyst expectations, propelling the stock to all-time highs during Friday’s trading session. This performance catalyzed significant momentum throughout the technology sector and provided substantial support for the Nasdaq Composite.

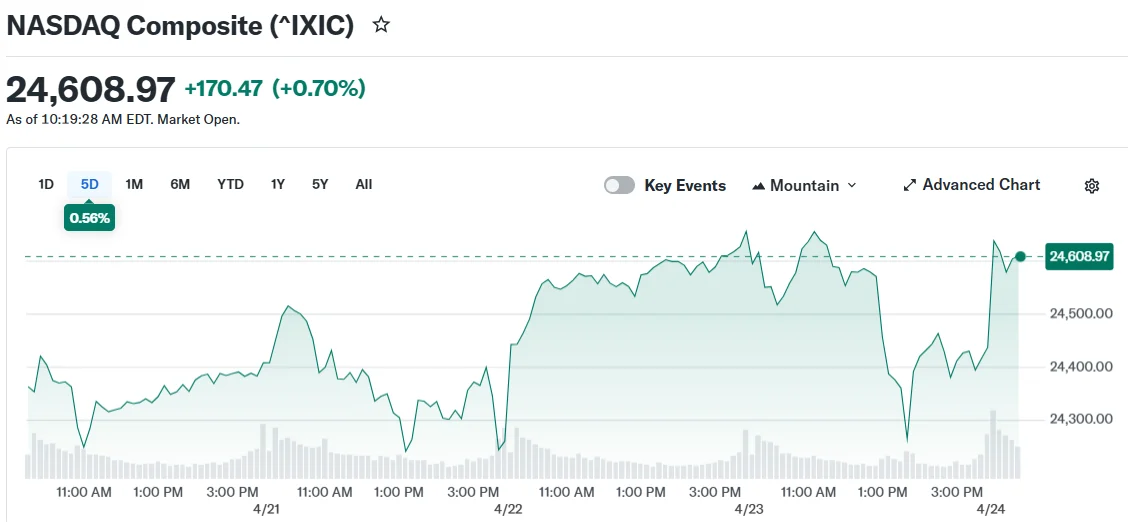

The technology-heavy Nasdaq Composite climbed 0.7% during the session. The broader S&P 500 index posted a 0.3% gain. Meanwhile, the Dow Jones Industrial Average retreated approximately 0.3%, hampered in part by its limited semiconductor sector representation.

The blue-chip index’s decision to substitute Nvidia for Intel in 2024 meant it couldn’t capitalize directly on Intel’s impressive rally. Additional headwinds from other major semiconductor manufacturers further pressured the index downward.

Texas Instruments enjoyed a particularly robust week as well. The company’s shares surged by their largest margin in a quarter-century on Thursday following impressive quarterly results, reinforcing the bullish sentiment pervading the semiconductor industry.

The PHLX Semiconductor Index extended its winning streak to an eighteenth straight session. Market data from Dow Jones indicates this represents an unprecedented achievement in the benchmark’s entire trading history.

Established Chipmakers Reap AI Infrastructure Rewards

Market analysts interpret the robust quarterly performances from Intel and Texas Instruments as evidence that the artificial intelligence infrastructure expansion is delivering benefits to traditional semiconductor manufacturers, not exclusively to emerging industry participants.

Both corporations serve as critical suppliers for expansive data center infrastructure projects. Their financial disclosures are being interpreted by market participants as confirmation that procurement activity throughout the semiconductor ecosystem continues at elevated levels.

Robust technology sector earnings provided market participants with justification to minimize concerns about continuing geopolitical instabilities across the Middle Eastern region. The Strait of Hormuz blockade persists, maintaining elevated anxiety within petroleum markets.

Brent crude futures retreated to levels just beneath $100 per barrel. West Texas Intermediate declined to approximately $95 per barrel. Market participants are closely monitoring whether diplomatic negotiations between the United States and Iran can advance productively.

President Trump declared a three-week prolongation of the Israel-Lebanon cessation of hostilities. Financial markets are evaluating whether this development might facilitate more comprehensive diplomatic engagement with Iran.

Energy and Digital Assets Face Headwinds

The President’s communications via social media platforms have been perceived by some observers as introducing complexity into diplomatic initiatives, despite the ceasefire’s continuation. The Strait of Hormuz impasse persists in affecting energy supply considerations.

Natural gas valuations were tracking toward a 16% weekly appreciation linked directly to Hormuz-related concerns. Energy sector equities experienced gains earlier in the week as the critical waterway remained inaccessible.

Bitcoin experienced downward pressure on Friday. Ongoing Middle Eastern uncertainties prompted certain investors to maintain distance from speculative assets, including digital currencies.

U.S. Treasury yields edged modestly lower as geopolitical complications remained prominent. The greenback maintained stability notwithstanding the ongoing international standoff.

Quarterly financial disclosures from Procter & Gamble, HCA Healthcare, and Norfolk Southern are scheduled for Friday release. Market participants are additionally monitoring the concluding April reading of the University of Michigan’s consumer sentiment gauge.

The Nasdaq Composite requires a closing price exceeding 24,657 to establish a fresh weekly closing record. The S&P 500 must surpass 7,137 to accomplish an equivalent milestone.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants