Key Takeaways

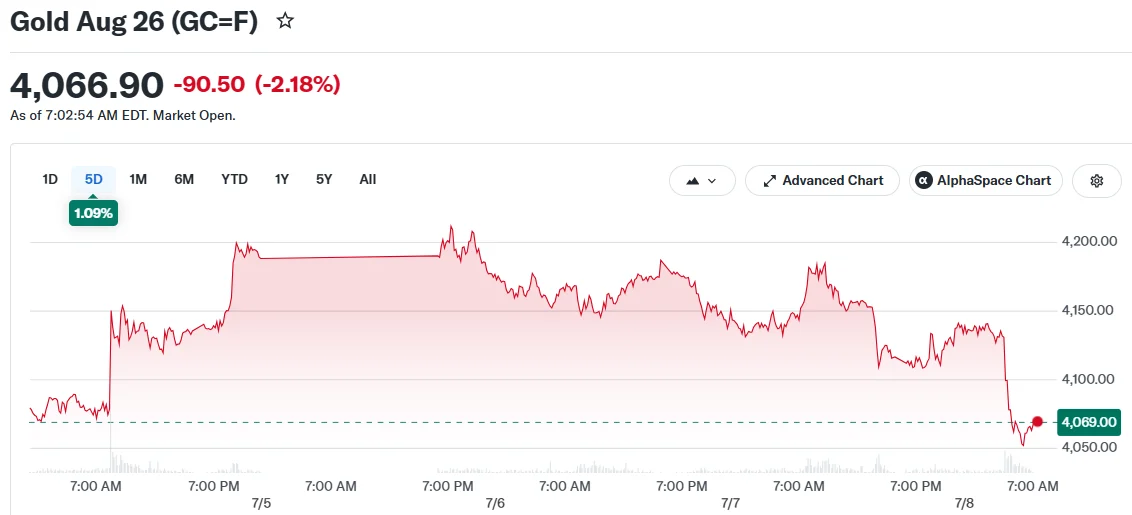

- Gold declined more than 1.3% to approximately $4,052 per ounce Wednesday

- President Trump announced the U.S.-Iran temporary peace agreement was finished during a NATO gathering in Turkey

- Iranian forces reported striking 85 American military installations across Kuwait and Bahrain

- Crude oil prices climbed amid heightened tensions, sparking renewed inflation concerns

- Silver tumbled 2.6%, platinum plummeted 3.5%, and palladium declined 3.2%

Precious metals experienced significant declines Wednesday following President Donald Trump’s declaration that the temporary peace agreement with Iran had collapsed, amid renewed military confrontations between the nations.

During early New York trading hours, spot gold decreased 1.2% to reach $4,057.09 per ounce. Gold futures contracts showed even steeper losses, falling 2.2% to $4,066.56 per ounce.

During his appearance at a NATO conference in Turkey, the President criticized Iran for publicly contradicting agreements allegedly reached in private negotiations.

“We make a deal, and everyone’s agreed. No nuclear weapons. We make a deal. They go outside, talk to the press, they say we never even talked about it. There’s something wrong with them. They’re cuckoo. As far as I’m concerned, it’s over,” Trump stated.

Iranian Forces Report Attacks on American Military Installations

The Islamic Revolutionary Guards Corps of Iran announced it conducted operations against 85 U.S. military facilities located in Kuwait and Bahrain, additionally claiming to have downed an American MQ-9 unmanned aerial vehicle.

The U.S. Department of Defense characterized its military operations as retaliation for Iranian aggression against commercial shipping vessels in the Strait of Hormuz, a critical waterway for international petroleum transport. According to U.S. Central Command, American forces targeted over 80 locations within Iranian territory and more than 60 Iranian small watercraft operating in and surrounding the strait.

Tehran has not acknowledged involvement in Tuesday’s attacks on vessels near the Omani coast, which affected a Saudi petroleum tanker and a Qatari ship transporting liquefied natural gas.

Crude Prices Climb, Stoking Inflation Worries

Oil prices advanced as geopolitical tensions intensified, recouping portions of the declines witnessed after the initial peace framework was established on June 17.

The uptick in crude oil values is reigniting concerns about accelerating inflation across global economies.

Market participants are now questioning whether the Federal Reserve will respond with interest rate increases. Expectations for Fed tightening had diminished following disappointing employment figures released last week, but strategists at Britannia Global Markets indicate those expectations are resurging in light of the recent military escalation.

Elevated interest rates generally diminish gold’s appeal among investors, as the precious metal generates no income. Additionally, a strengthening U.S. dollar could increase gold’s cost for international purchasers.

Lukman Otunuga, Head of Market Research at FXTM, characterized gold as standing at a “critical crossroads,” where geopolitical instability and inflation anxieties are competing against weaker U.S. economic indicators that may constrain the Fed’s policy options.

Investors are now anticipating the release of the Federal Reserve’s June meeting minutes, scheduled for later Wednesday. The central bank maintained its benchmark rate range at 3.5% to 3.75% during that session, although certain committee members forecast potential rate hikes in 2026.

Other precious metals also experienced significant losses. Silver declined 2.61% to $58.39 per ounce, platinum dropped 3.47% to $1,589.17, and palladium fell 3.19% to $1,212.94.

The President’s additional remarks regarding Greenland and Spain during the NATO summit contributed to broader uncertainties about global stability, applying further downward pressure on precious metals markets.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants