Stock: Design Platform Drops 6% Before First Earnings Report. Here’s Why")

TLDR

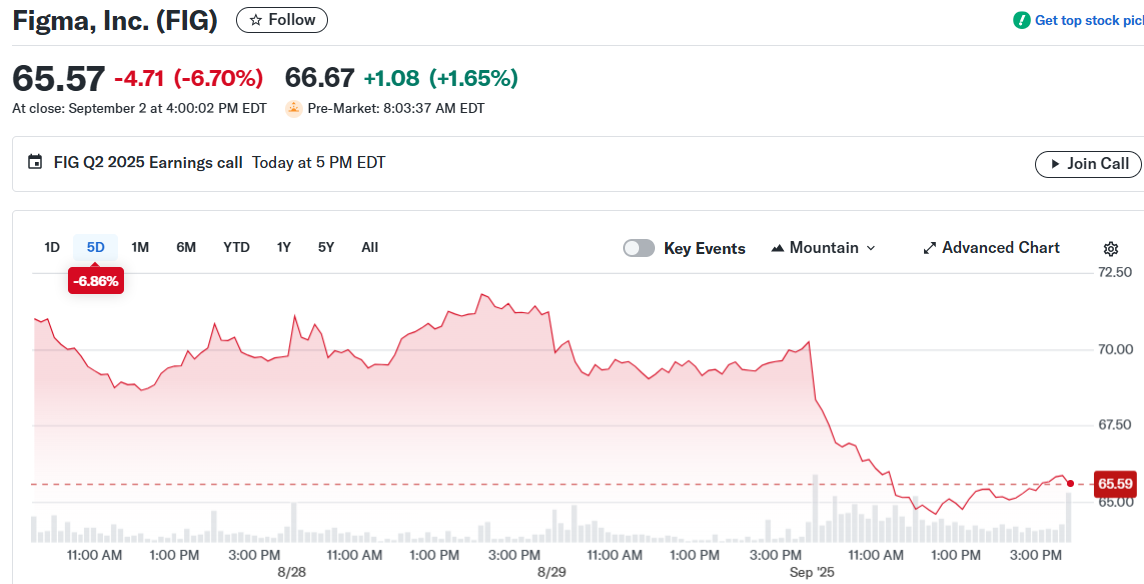

- Figma (FIG) shares fell 6.7% to $65.57 with $520M trading volume before Wednesday earnings

- Company expects Q2 earnings of 9 cents per share on $250M revenue, up 40% year-over-year

- Stock trades at 200+ times earnings while rival Adobe trades at 17 times earnings

- Only 4 of 11 analysts rate Figma as Buy due to valuation concerns

- Key metrics include 132% Net Dollar Retention and 1,031 customers paying over $100K annually

Figma stock dropped 6.7% Tuesday ahead of the design software company’s first earnings report as a public company. Shares closed at $65.57 with trading volume reaching $520 million.

The design collaboration platform will release second-quarter results Wednesday after market close. Wall Street expects earnings of 9 cents per share on revenue of $250 million, representing 40% growth from last year.

Figma went public July 31 at $33 per share and soared 250% on its debut day. The stock hit a peak near $143 before settling at current levels around $70.

The company now holds a market value of nearly $35 billion. This puts the stock at over 200 times this year’s earnings estimates.

Analysts Express Caution

Wall Street remains divided on Figma’s prospects. Only four of eleven analysts rate the stock a Buy, while seven assign Hold ratings.

BofA Securities analyst Brad Sills noted Figma trades at a “big premium to the large-cap software group.” He rates the stock Neutral, believing “near-term upside is largely priced in.”

Rival Adobe trades at just 17 times forward earnings for comparison. Adobe attempted to acquire Figma for $20 billion in 2022, but regulators blocked the deal over antitrust concerns.

RBC Capital Markets analyst Rishi Jaluria also rates Figma as Sector Perform. He views shares as “fully valued” and suggests investors “wait for a better entry.”

Growth Metrics Under Scrutiny

Investors will focus on Figma’s Net Dollar Retention rate of 132% as of March 2025. This metric shows how much existing customers increase their spending over time.

The company raised prices in March 2025, which should boost revenue and retention numbers. Analysts expect this impact to fade by early 2026.

Figma’s enterprise customer base continues expanding. The number of customers paying over $100,000 annually grew 47% year-over-year to 1,031.

Gross margins currently sit at 91%, reflecting the profitable nature of software businesses. However, AI investments may pressure margins to 87% in 2025 and 83% in 2026.

Figma lost money in the second quarter of 2024, making the path to profitability a key focus area. The company develops AI tools like Figma Make to stay competitive.

Competition concerns include established players like Adobe and newer AI-powered design platforms. How Figma navigates these challenges will determine investor confidence.

The stock joins other recent IPOs that saw massive first-day gains before cooling off. Circle Internet Group peaked near $300 after going public at $31 but now trades around $132.

Figma’s earnings report will test whether the company can justify its premium valuation through strong execution and growth metrics.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants