If you are looking for another crowdfunding platform for your P2P portfolio, you should consider about EstateGuru.

The company is a trustworthy P2P lending platform with a solid track record. P2P lending is a growing industry, and it offers investors some advantages over other forms of debt-based investments.

One of the biggest things that P2P lending allows investors to do is access a market that has been off-limits to small-scale investment.

Lending to real estate borrowers has traditionally been limited to banks, but P2P lending is changing that. If you want to take advantage of this trend, EstateGuru is worth learning more about.

Like any form of investment, P2P lending does have risks. When you decide to loan a person or company money, there is a risk of total loss.

While some P2P lending platforms have safeguards in place to limit the chance of a catastrophic default, it is very important to understand how these investments are structured. EstateGuru’s loans are generally backed up by real estate, or some other form of collateral.

EstateGuru has put together a good P2P lending platform that may be a good fit for your investing style. Let’s have a look at what it offers, and how you could make money with P2P lending.

EstateGuru at a Glance

| EstateGuru - Visit |

|---|---|

| Product Type | Real Estate Crowdfunding |

| Potential Return | 12% |

| Fees | No Fees for Investors, 2% for Secondary Market |

| Min Investment | €50 |

| Loan Types | bridge loan, business loan, development loan, refinancing loan, reconstruction loan, sale advance loan, construction loan |

| Available to | EU |

What is EstateGuru?

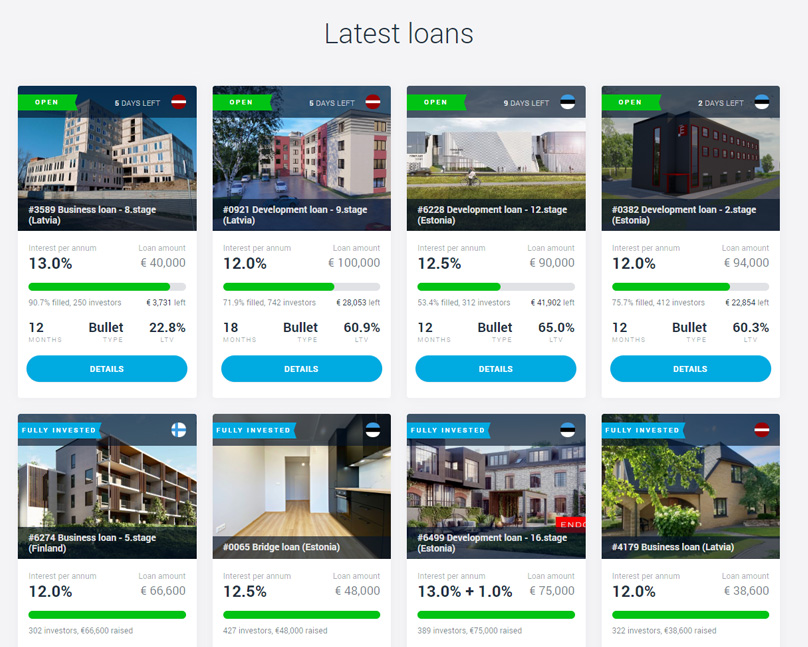

EstateGuru is a European marketplace for short-term, property-backed loans. There are several loan types that you can find, including development, refinancing, construction and bridge loans on their platform.

Real estate lending has some advantages over other kinds of P2P investment. In general, a real estate backed loan will be more secure than another form of debt, as properties are used as collateral. This may be more appealing to risk-averse investors who prioritize the return of capital over return on capital.

EstateGuru was established in 2014 and based in Tallinn, Estonia. The platform now has over 38,000 investors from 45 countries registered. It has an easy to understand interface and a simple sign-up process. In terms of its age, it is somewhere in the middle of the P2P lenders.

Most P2P lending platforms came into existence after 2008, although many have entered the marketplace in the last couple of years. Investors need to understand the chain-of-custody, and how they would be repaid in the event of a default.

How does EstateGuru Work?

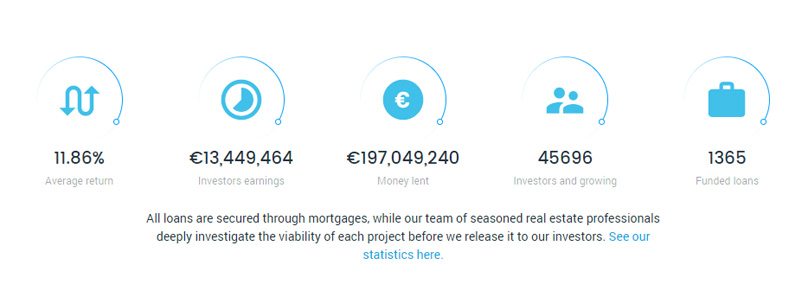

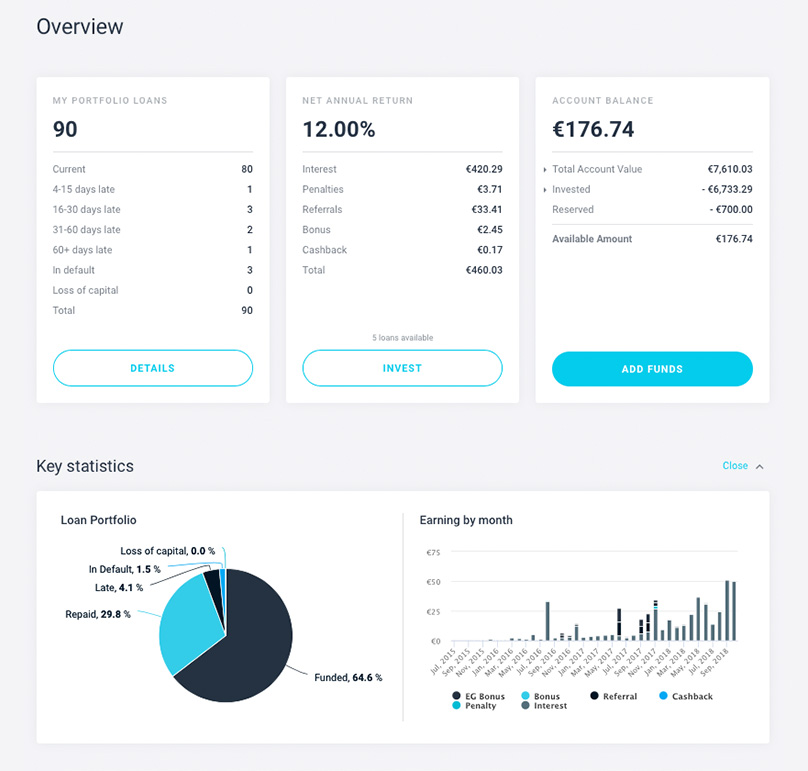

EstateGuru has grown quickly and has become one of the largest P2P investment sites in the European marketplace. It has a good track record and investors have achieved average returns over 12% to date. The platform mainly helps developers and business owners gain access to P2P lenders.

Loans are made to developers which fund the development of a property or provide a bridge loan that is secured against a completed asset.

Loans to businesses usually provide working capital and are secured by commercial assets which are often hotels and restaurants, or residential property (often the house of one of the company’s directors).

Loan Duration and Locations

The loans that are available on EstateGuru are made for a short period of time and are made for 12-18 months. This makes rolling over your investments simple, although it is more work for investors who want to have a high degree of control over their investments.

The average loan-to-value (LTV) ratio on EstateGuru is around 58% (according to the company). This is a little higher than other platforms, such as Bulkestate, a similar P2P marketplace. Moreover, because EstateGuru has a lot more loans on its platform, it is easier to get all your money invested.

Since the platform is based in Estonia, the loans on the platform are primarily issued to borrowers in the Baltic countries. A small percentage of the loans are issued to borrowers from other countries, including Latvia, Lithuania, Finland, and Spain. Portugal also joined this list in August.

You can start investing in EstateGuru from only €50. Your money is secured by something that has a market value in most cases, such as physical collateral, the personal guarantee of the borrower or a mortgage.

Who Can Invest via EstateGuru?

Anyone who is over 18 years old and has a bank account in EEA member states or Switzerland can invest with EstateGuru, as long as they can pass the KYC checks. It is very easy to get started with the platform.

If you meet the necessary requirements, you can start investing by following the steps below:

- Create an account

- Add funds to your account

- Pick loans and start investing

Investing in EstateGuru is Safe?

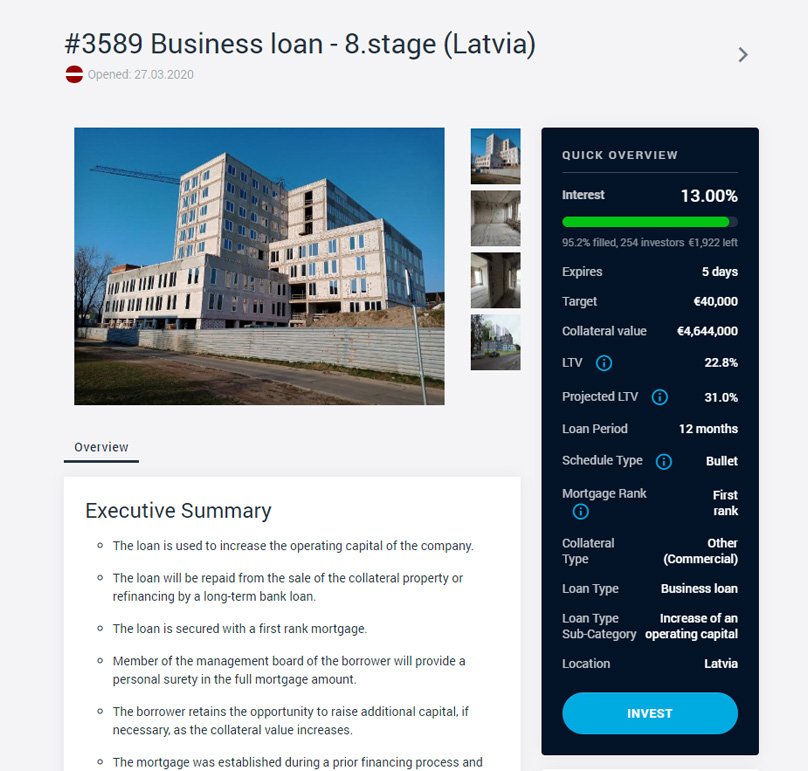

EstateGuru conducts thorough due diligence of each loan. The platform checks borrowers on the basis of a credit rating, and also ensure there is some form of collateral in the event that the borrower is unable to repay the loan.

If the borrower does not meet the requirements of EstateGuru, no loans are issued. In this way loans on the platform are more secure than a platform that doesn’t require collateral, as borrowers are protected by the assets that back up the P2P loan.

From a legal point of view, EstateGuru is not a finance provider, they are a facilitator. Therefore, asset management is not something they do

All the loan contracts will be written between the borrower and the investors, so the creditworthiness of the platform isn’t as important as other platforms that act as a counterparty.

Investor funds are kept separate from EstateGuru’s accounts. If EstateGuru were to go out of business, the investors’ money could still be withdrawn from the platform, as a contractual entity will take over the management of the contracts.

This arrangement makes EstateGuru safer for investors than a structure that puts the platform in the middle of investors and borrowers.

EstateGuru Risk & Returns

EstateGuru works directly with the borrower, which is not as common in the P2P lending niche.

Other popular P2P platforms like Mintos or Peerberry work together with loan originators which take a cut from the investor’s interest. This arrangement is ok in some regards, as it offers a loan originator as a counterparty, which makes buyback guarantees a little bit easier to create.

The real estate projects on EstateGuru are more secured by mortgages as opposed to unsecured personal loans on other platforms, in this regard, EstateGuru has an advantage.

The risk of losing your investments on EstateGuru is generally lower when compared to loans that are not secured by any collateral, which makes EstateGuru a great alternative for investors that only want to invest in secured P2P loans.

Investors have not suffered any losses when loans have defaulted so far. If EstateGuru can maintain this, it will be a very successful site in the long run. It is important to remember that past performance is no guarantee of future returns, as market conditions can impact borrowers’ ability to repay debt.

The average historic return for investors at EstateGuru is around 11.89% which is more than most other P2P platforms offer.

When comparing the EstateGuru’s risks and returns to other P2P lending sites, it looks positive. You can earn more than 11% on your investments in property-backed loans, which is a very attractive deal.

EstateGuru Features

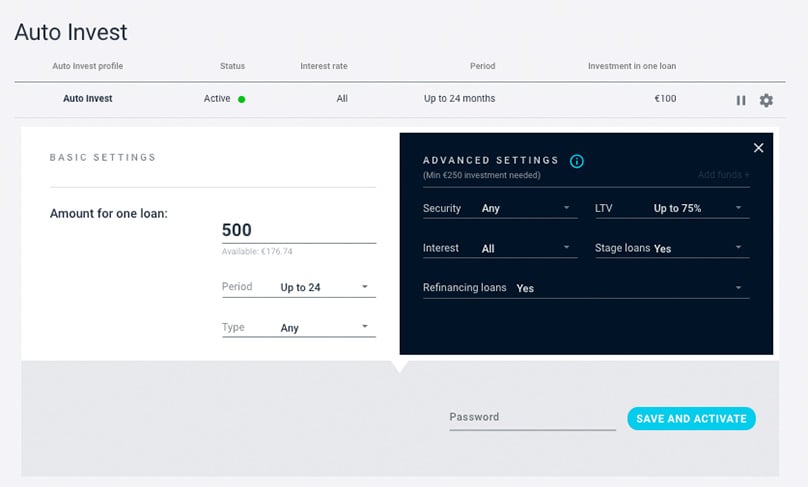

EstateGuru Auto Invest

The Auto Invest function is one of the most basic automated investment tools in the P2P lending platform. There are not many options to filter and some of the options are only available to investors with a minimum investment of €250.

That said, if you want to save time, this is a handy feature. Many P2P investors don’t want to spend loads of time picking through every loan, and the auto invest feature eliminates this issue.

Secondary Market

EstateGuru launched the Secondary Market feature late last year. This feature has great potential for those who are looking to withdraw money early from a loan they bought via EstateGuru. There are a few hundred loans for sale on this market, and most of them are actually sold at a premium.

However, there are a few things you need to keep in mind when using the EstateGuru Secondary Market. In some ways, it may be better to look for new loan offerings, as the secondary market may be more expensive.

When using the Secondary Market, sellers will be charged a 2% fee. Buyers cannot sell their claims within 30 days from the purchase on the Secondary Market. Investments on the Secondary Market are not automated included in the auto invest feature, so you will have to sort through them if you are interested.

Overall it is a good feature, but it may not offer great value for investors.

International Expansion

The platform is currently translated into six languages, which helps investors from other countries to access the site. The platform is also expanding in new territories to help diversification, and offer credit to new borrowers.

EstateGuru Loan Options

EstateGuru is currently offering the following options:

- 7 Loan Types include bridge loan, business loan, development loan, refinancing loan, reconstruction loan, sale advance loan, construction loan

- Minimum Investment: €50

- 6 Countries are Estonia, Latvia, Lithuania, Spain, Finland, Portugal

- Loan Period is from 6 to 36 months. Most of the loans have a loan duration of 12 to 24 months.

- Buyback Guarantee: No

- Auto Invest: Yes

EstateGuru’s basic Auto Invest feature has one drawback.

Investors that want to diversify and automate their investments and are not willing to invest at least €250 per project that cannot use the advanced Auto Invest settings, which means you will be only allowed to define the investment amount, loan period and loan types.

If you invite at least 50 friends to invest in EstateGuru, then you can unlock all the Auto Invest functions even if you only invest €50. Advanced options such as LTV, Security, Interest, Stage loans, and Refinancing are only able to access by the investors who invest at least €250 in one project.

EstateGuru Pros & Cons

EstateGuru is a compelling option for P2P investors that want to create a short-duration loan portfolio that focuses on a limited geographic region.

The platform is easy to use, and it is pretty easy to qualify for the platform as an investor. The initial required investment is low, but there are some drawbacks to just depositing the minimum.

Let’s have a look at what EstateGuru does well, and what could be improved on:

Pros

- All loans are secured.

- Higher liquidity with the secondary market.

- Risk assessment is very good. Collateral like completed buildings are used to secure loans.

- Easy Sign-Up and fast money transfer.

- Large loan volume and no investment fee.

- History of successfully repaid loans and an efficient recovery process. The quality of the information provided about each loan is excellent.

- High level of transparency. EstateGuru has an excellent lending record. Though there have been defaults, investors have achieved a full recovery on their investment so far.

- LTVs are reasonable which is generally around 60%.

- The number of loans listed has been increasing.

- The number of countries where loans are sources is growing.

- The website is well made and is easy to use.

- The website offers multiple languages.

Cons

- The Secondary Market is not free to use, investors are charged a 2% fee for early withdrawals.

- Not suitable for short-term investments.

- Not a ton of diversification options.

- Restricted auto investment tools for small portfolios. The auto-invest function does not have sufficient filters and requires a minimum investment of €250 per loan to unlock basic filters.

- It can take time to build up a large, diversified portfolio.

- Investment opportunities are mainly biased towards the Baltic region of Europe, which may not suit some investors.

- Risk level can change substantially from loan to loan.

EstateGuru Support

All of the questions should be answered within a few days. You can contact the EstateGuru support via email at info@estateguru.co.

The P2P Market

The world of P2P lending has been on a steady trajectory upward.

The reasons for this are simple, and will likely help P2P lending platforms to grow further.

People can borrow at competitive rates from private investors, and circumvent the major banks. There has been a monopoly on lending for a long time, and this has created a situation that is making P2P lending very attractive for everyone involved.

It is important to remember that there are many ways to make debt-based investments, and P2P lending is only one of them. The world of corporate bonds has seen a shock over the last few months, and there could be some good deals emerging in that space.

While market-wide downturns are rare, they do happen. When an economy is highly focused on a few sources of debt, a faltering global financial system can create chaos at every level.

The crisis in 2008 was an example of this, and it may happen again. In the event of a massive global sell-off, you will be happy that you have a well-diversified portfolio.

Always make sure that any debt or equity investment comes after your liquid investments, which are what ensures that there is always money to pay your bills. You should have liquid capital to cover your living expenses for at least six months before you consider buying riskier investments.

Conclusion

EstateGuru is a legit European P2P lending company and has a longer track record than some of the other real estate P2P lending platforms. It has been fairly safe for its investors so far and also delivers a high rate of return.

It is easy to deploy larger amounts of money with EstateGuru, although it isn’t a great idea to take on concentrated positions in any market. Whenever you decide to invest your money, diversification is extremely important.

The vast majority of the loans on the platform are in the Baltic region, but there are plans to grow in the UK, Portugal, Ireland, and Spain, which is a positive development for investors. The volume of loans has been increasing on EstateGuru. However, it still takes time to build a diversified portfolio.

A portfolio of at least 15-20 loans is a good place to start.

It is vital that investors use a basket of loans to reduce the potential impact of a single default. Even though LTVs are low, investors still can select on which loans to invest. Some loans will be better than others.

If your overall portfolio is large and you want to create higher returns, you should consider which P2P lending platforms would work for your goals.

There is nothing wrong with spreading your money out over a number of platforms, even if it seems like you don’t have loads. Start practicing good investment habits now, and reap the rewards later on.

If you have some saved money and are looking for a new investment channel, EstateGuru gives you a good opportunity to let your money work for you and earn up to 12% of interest every year. It is unlikely that you will face catastrophic losses on its platform, and the company itself is never your counterparty.

Any money you invest with EstateGuru is protected by real estate. Not every P2P lending site can say the same. The platform is easy to use, and many investors have chosen to make P2P loans with it.

EstateGuru

Pros

- All loans are secured.

- Higher liquidity with the secondary market.

- Large loan volume and no investment fees

- History of successfully repaid loans

- Excellent lending record

Cons

- 2% Fee on Secondary Market

- Restricted auto investment tools

- Risk level can change substantially from loan to loan.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants