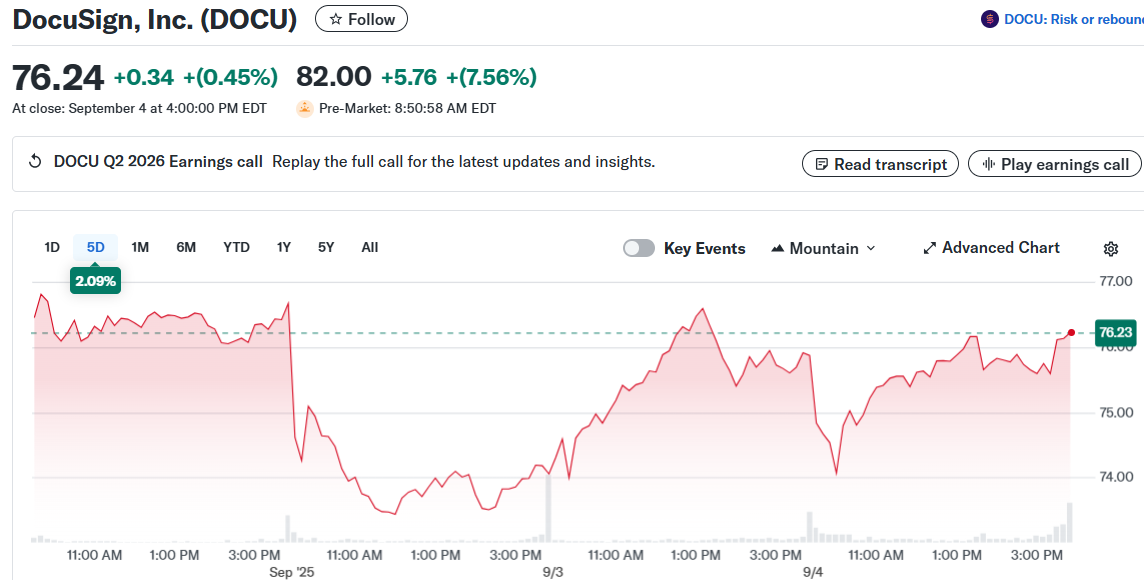

Stock: Earnings Winning Streak Hits Four Quarters Despite 15% YTD Decline")

TLDR

- DocuSign (DOCU) beat Q2 earnings expectations with $0.92 per share versus $0.84 expected

- Revenue hit $800.64 million, exceeding estimates by 2.78% with 9% year-over-year growth

- Evercore ISI raised price target to $92 from $90 while maintaining “In Line” rating

- International revenue grew 13% and now represents 29% of total revenue

- Company raised full-year revenue guidance to $3.19-$3.20 billion from previous $3.16 billion estimate

DocuSign delivered another solid quarter, proving the electronic signature company still has some fight left despite a rough year. The company posted earnings of $0.92 per share for Q2, handily beating analyst expectations of $0.84.

This marks the fourth consecutive quarter where DocuSign has topped earnings estimates. Last quarter, the company surprised analysts by 11.11% when it delivered $0.90 per share against expectations of $0.81.

Revenue came in at $800.64 million for the quarter ending in July. This beat the consensus estimate and represented a 9% increase from the same period last year when revenue was $736.03 million.

The company has now beaten revenue estimates for four straight quarters. Billings reached $818 million, growing 13% and crushing the expected $762.5 million.

Strong International Growth Powers Results

International markets continue to be a bright spot for DocuSign. International revenue jumped 13% year-over-year and now makes up 29% of total revenue.

The Asia-Pacific region emerged as the fastest-growing market for the company. This international expansion helps diversify DocuSign’s revenue base beyond its core U.S. market.

The company also landed its largest deal of the quarter through the Microsoft Azure Marketplace. It secured a new partnership with the General Services Administration as well.

Net retention improved by 100 basis points sequentially to 102%. This improvement came primarily from stronger gross retention in the eSignature business.

DocuSign showed progress in its Contract Lifecycle Management offerings. The company also maintained momentum in Identity and Access Management services.

Analyst Upgrades Follow Strong Performance

Following the earnings beat, Evercore ISI raised its price target on DocuSign stock. The firm bumped its target to $92 from $90 while keeping an “In Line” rating.

The analyst upgrade reflects confidence in DocuSign’s execution improvements. The company’s go-to-market strategy appears to be gaining traction after previous struggles.

DocuSign raised its full-year revenue guidance based on the strong Q2 results. The company now expects revenue between $3.19 billion and $3.20 billion for the full year.

This represents approximately 7% growth compared to the previous guidance of $3.16 billion. The guidance raise shows management’s increased confidence in business momentum.

Operating margins did decline 240 basis points year-over-year to 29.8%. Management attributed this to higher cash compensation and cloud migration costs.

These margin pressures appear temporary according to company leadership. The cloud migration should provide long-term benefits once complete.

Despite the strong quarter, DocuSign stock remains down about 15.6% year-to-date. This compares poorly to the S&P 500’s 9.6% gain over the same period.

The stock carries a Zacks Rank of #3 (Hold), suggesting shares should perform in line with the market. Current consensus estimates call for $0.89 per share on $795.56 million in revenue for the next quarter.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants