Stock: Shares Fall Despite Record AI Revenue Beat. Here’s Why")

TLDR

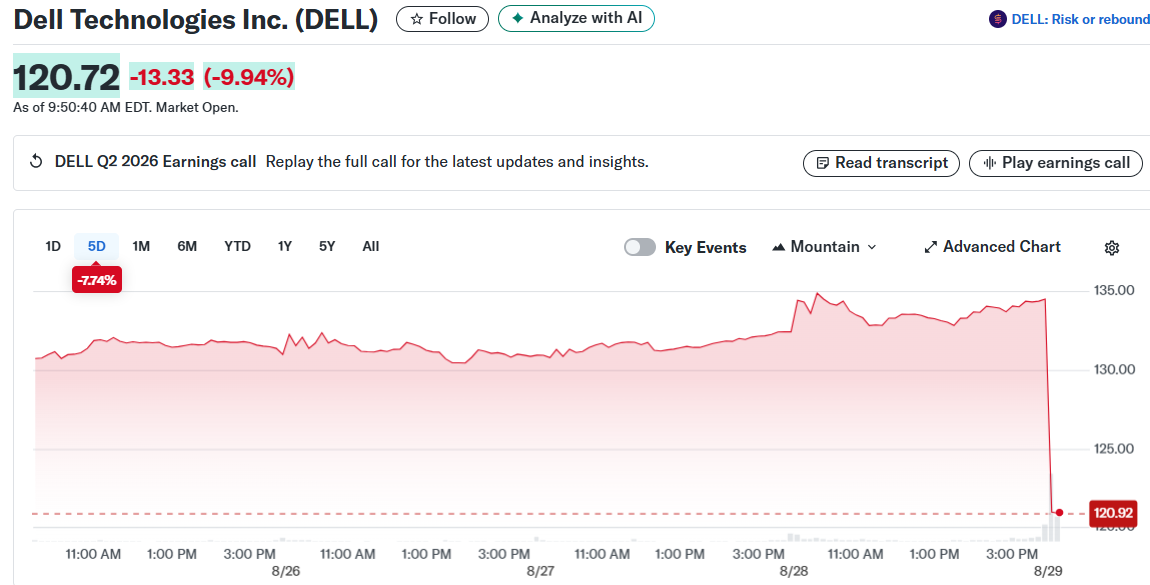

- Dell Technologies (DELL) shares dropped 7% in premarket trading despite beating Q2 earnings expectations with record $29.8 billion revenue

- Company raised AI server shipment guidance to $20 billion for full year, up from previous $15 billion target

- Dell shipped $10 billion in AI solutions in first half of fiscal 2026, already exceeding all of fiscal 2025

- Q3 earnings projection of $2.45 per share came in below analyst expectations of $2.49

- AI server backlog declined to $11.7 billion from $14.4 billion in Q1, raising concerns about order momentum

Dell Technologies delivered a mixed bag of results that left investors scratching their heads. The company posted record second-quarter revenue of $29.8 billion, up 19% year-over-year, and beat earnings expectations across the board.

Adjusted earnings per share hit $2.32, marking a 19% increase from the previous year. Cash flow from operations nearly doubled to $2.5 billion, showing the company’s operational muscle.

The real star of the show was Dell’s AI server business. The company shipped $8.2 billion worth of AI servers during the quarter alone. That brought first-half shipments to $10 billion, already exceeding all of fiscal 2025.

AI Business Momentum Builds

Dell’s AI momentum prompted management to raise their full-year AI server shipment guidance. The new target sits at $20 billion, up from the previous $15 billion forecast.

Chief Operating Officer Jeff Clarke highlighted the “exceptional” demand driving these numbers. The company ended Q2 with an $11.7 billion backlog of AI server orders.

Dell was first to deliver Nvidia’s GB300 NVL72 systems to CoreWeave in July. This positions them well in the competitive AI infrastructure market.

The servers and networking business grew 69% during the quarter. This division has become Dell’s growth engine as companies rush to build AI capabilities.

Yet investors chose to focus on the concerning signals. Dell’s third-quarter earnings guidance came in at $2.45 per share, below the $2.49 analysts expected.

Margin Pressure Creates Concerns

Non-GAAP gross margins slipped to 18.7% in Q2 from 22.4% a year earlier. The decline reflects the reality of AI server economics, where margins run thinner than traditional enterprise products.

Dell’s PC segment also struggled, with sales falling 3% below consensus forecasts. Citi analysts noted the company “likely lost share in PCs” during the quarter.

The AI server backlog dropped from $14.4 billion in Q1 to $11.7 billion in Q2. While still substantial, the decline sparked questions about whether order momentum might be plateauing.

Analysts see Dell’s AI success benefiting other tech companies. Nvidia makes up 88% of Dell’s AI server sales, while Micron Technology accounts for 17%.

Dell expects traditional server business to grow in the second half but below earlier expectations. This tempers some of the enthusiasm around the AI gains.

Shares fell 7% in premarket trading Friday after closing Thursday up 16% for the year. The stock reaction shows how quickly sentiment can shift when guidance disappoints.

Dell’s management expressed confidence in their pipeline and competitive position. The company continues to ramp production to meet AI infrastructure demand while managing margin pressure.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants