Stock: Why This Nvidia Partner’s Shares Are on a Wild Ride")

TLDR

- CoreWeave reported Q1 revenue of $981.6 million, exceeding analyst estimates of $862.3 million

- The company plans to spend $20-23 billion in 2025, higher than Wall Street’s projected $18.3 billion

- Stock initially jumped 11% after earnings but later dropped 8% in premarket trading due to capex concerns

- CoreWeave secured a new $4 billion deal with an unnamed “large AI enterprise”

- Despite revenue growth, the company reported an adjusted net loss of $150 million for Q1

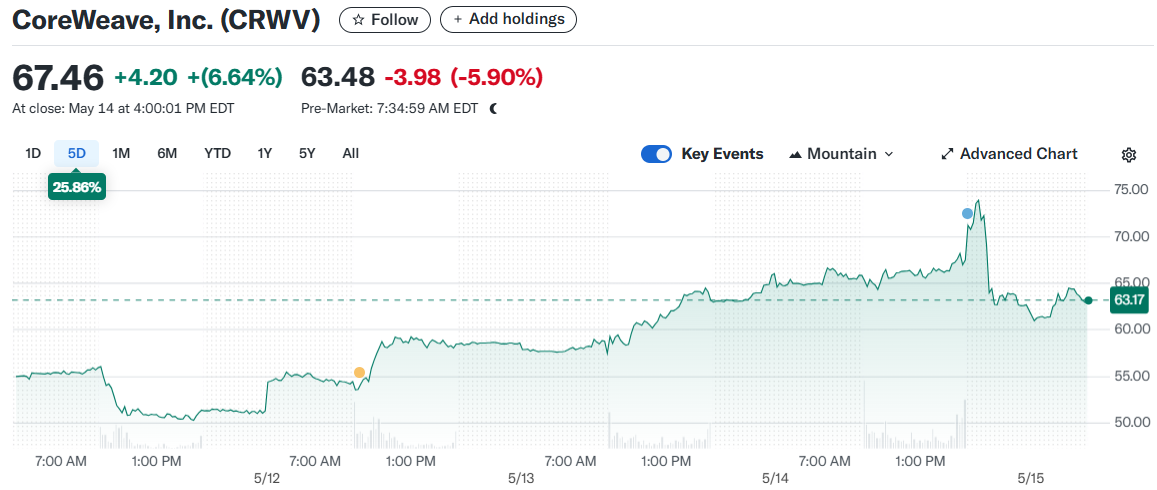

CoreWeave, the Nvidia-backed AI data center firm, released its first earnings report as a public company, revealing strong revenue growth but also plans for massive capital expenditure that sent its stock on a rollercoaster ride. The company’s stock initially jumped 11% after the earnings release on Wednesday but then dropped as much as 8% in premarket trading on Thursday as investors digested the higher-than-expected spending plans.

The company reported revenue of $981.6 million for the first quarter ending March 31, significantly exceeding Wall Street analysts’ expectations of $862.3 million. CoreWeave also provided an optimistic outlook for the year, projecting second-quarter revenue between $1.06 billion and $1.1 billion and full-year revenue between $4.9 billion and $5.1 billion.

These projections surpass analysts’ expectations of $1.04 billion for Q2 and $4.6 billion for the full year. The company attributed its higher revenue outlook to a deal with OpenAI and a new $4 billion agreement with what CEO Michael Intrator described as a “large AI enterprise” hyperscaler.

“Demand for our platform is robust and accelerating as AI leaders seek the highly performant AI cloud infrastructure required for the most advanced applications,” Intrator stated in the earnings release.

Capital Spending Concerns

What spooked investors, however, was CoreWeave’s capital expenditure plans. Company executives announced they expect to spend between $20 billion and $23 billion in 2025, exceeding the $18.3 billion projected by Wall Street analysts.

CFO Nitin Agrawal explained that the higher spending is “fundamentally driven by increased customer demand.” CoreWeave is one of the largest holders of Nvidia’s graphics processing units and rents its data center capacity to Big Tech companies such as Microsoft and Meta as they pursue their AI ambitions.

The spending plans raised concerns about the company’s financial structure, which some analysts describe as risky. According to DA Davidson analyst Gil Luria, CoreWeave has approximately $12 billion worth of debt commitments with high interest rates ranging from 10% to 14%.

CoreWeave uses this debt, borrowed against its store of Nvidia GPUs as collateral, to purchase more Nvidia chips. “The risk is this is a company that is borrowing at extraordinarily high interest rates in order to buy a product that depreciates very rapidly in terms of its economic value,” Luria told Yahoo Finance.

Profitability Challenges

Despite the impressive revenue figures, CoreWeave is still not profitable. The company reported an adjusted net loss of approximately $150 million for the first quarter, which was steeper than the $41.7 million loss expected by analysts.

Citi analyst Tyler Radke noted that not all financial metrics met expectations. The company’s capital expenditures for Q1 fell short at $1.9 billion compared to the anticipated $2.6 billion. CoreWeave’s Remaining Performance Obligations also saw a modest quarter-over-quarter decline, though this did not account for the OpenAI contract and the expected $4 billion expansion in the second quarter.

Radke also pointed out mixed results in profitability metrics. Adjusted EBIT margins came in below expectations, and earnings per share as well as net income were significantly lower than anticipated, owing to increased interest expenses due to less capitalization.

Customer Concentration

Another concern for analysts is CoreWeave’s customer concentration. According to regulatory filings, 77% of the company’s 2024 revenue came from just two customers, with Microsoft accounting for 62%. CoreWeave stated that no customer made up more than 50% of its revenue at the end of its first quarter but acknowledged that this will not be the case going forward with its new $4 billion deal.

DA Davidson’s Luria maintains skepticism about what he calls CoreWeave’s “risky” capital structure and high customer concentration. “As long as this demand for AI services continues to grow exponentially, they’ll be fine,” he said. But if demand wanes, “this doesn’t go well because this is a company with inherently low margins and low returns that is borrowing at very high rates.”

Financial Maneuvers

To strengthen its financial position, CoreWeave has expanded its financial capacity by amending its existing credit agreement, increasing its revolving credit facility from $650 million to $1.5 billion. This move extends the maturity of the facility to May 2, 2028.

The company is also reportedly in talks to raise approximately $1.5 billion in debt through high-yield bonds, with JPMorgan Chase potentially leading the effort. This comes after CoreWeave scaled down its initial public offering from a planned $4 billion to $1.5 billion due to market volatility.

Analyst Opinions

Analyst opinions on CoreWeave remain mixed. Seven analysts tracked by Bloomberg hold a Buy rating on the stock, while nine hold Neutral ratings. Hedgeye Risk Management holds a short position.

Northland has initiated coverage with an Outperform rating and a price target of $80, citing the company’s strong pricing strategies and long-term financial health. The firm projects a 31% long-term free cash flow margin and expects CoreWeave to capture a 10% market share in the AIaaS market by 2025.

Macquarie, on the other hand, has set a Neutral rating with a $56 target, highlighting CoreWeave’s proprietary Cloud Platform as a key differentiator in the AI cloud reselling market. The firm notes that CoreWeave’s current contracted client commitments, valued at approximately $27 billion, are expected to support revenue growth through 2030.

After falling to a closing price low of $35 in April, CoreWeave shares have soared nearly 55% over the past month, trading at $67 on Wednesday. The stock’s recent performance reflects investors’ optimism about the booming AI sector, tempered by concerns about the company’s spending plans and path to profitability.

CoreWeave’s upcoming capital expenditure of $20-23 billion in 2025 aims to meet growing customer demand for AI infrastructure services, with a new $4 billion client deal already secured.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants