Stock: AI Revenue Surge Expected in September Earnings Report")

TLDR

- Broadcom reports Q3 2025 earnings Sept. 4 with AI revenue projected to jump 60% year-over-year to $5.1 billion

- Piper Sandler analyst increased price target from $300 to $315, maintaining overweight rating

- Stock trades at elevated P/S ratio of 24.3 and P/E ratio of 108.4, raising valuation concerns

- Three major customers plan 1 million AI accelerators each by 2027, creating $60-90 billion market opportunity

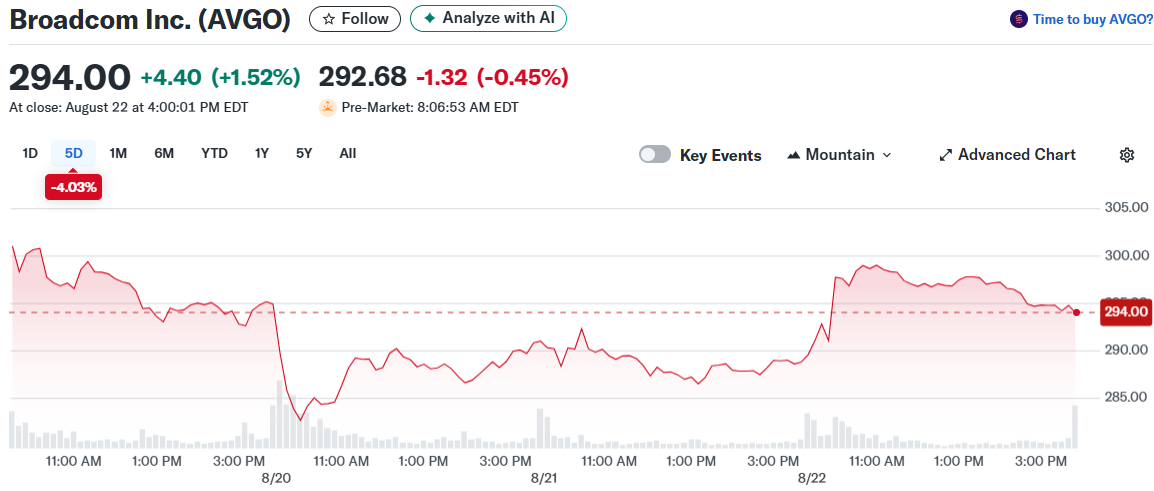

- AVGO shares gained 1.5% Friday as investors prepare for earnings results

Broadcom stock rallied 1.5% Friday ahead of its fiscal Q3 2025 earnings report scheduled for Sept. 4. The semiconductor company expects to deliver another quarter of explosive artificial intelligence revenue growth.

Management forecasts total revenue of $15.8 billion for the quarter ending July 30. AI revenue is projected to soar 60% year-over-year to $5.1 billion, accelerating from Q2’s 46% growth rate.

Piper Sandler analyst Harsh Kumar boosted his AVGO price target to $315 from $300 Friday. Kumar maintained his overweight rating, citing strong demand for AI-suitable semiconductor components.

The analyst models 60% year-over-year growth for Broadcom’s key semiconductor division in Q3. While non-AI business remains flat, Kumar sees signs of potential recovery ahead.

Hyperscale AI Accelerator Demand Drives Growth

Major tech companies increasingly choose Broadcom’s custom AI accelerators over standard GPUs from competitors. These specialized chips offer greater flexibility for specific AI workloads.

At least three hyperscale customers plan deploying up to 1 million AI accelerators each by 2027. This creates a serviceable market worth $60-90 billion in 2027 alone.

Broadcom also supplies critical data center networking equipment. The company’s Ethernet switches regulate data flow between devices, with the Tomahawk Ultra offering industry-leading performance specs.

Recent Q2 results showed strong profitability trends. GAAP net income surged 134% year-over-year to $4.9 billion. Adjusted EBITDA climbed 35% to $10 billion, stripping out one-time expenses.

Management expects Q3 adjusted EBITDA around $10.4 billion, indicating continued momentum in operational performance.

Valuation Concerns May Limit Upside

Despite strong fundamentals, AVGO trades at premium valuations that could cap short-term gains. The stock’s price-to-sales ratio of 24.3 sits near record highs, almost triple its 10-year average of 8.4.

Trailing earnings of $2.67 per share translate to a P/E ratio of 108.4. This makes Broadcom three times more expensive than the Nasdaq-100’s 33.5 P/E multiple.

High valuations reflect investor optimism about AI growth prospects but may limit upside even with strong earnings results. The company needs sustained AI revenue growth to justify current price levels.

Recent MIT research questioned enterprise AI investment returns, though this likely reflects implementation challenges rather than technology limitations. Businesses continue learning to optimize AI deployments effectively.

Broadcom’s Sept. 4 earnings will provide fresh insight into whether AI demand can sustain the company’s growth trajectory and support elevated stock valuations through 2025.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants