Stock Downgraded to Underperform by Jefferies on iPhone 18 Concerns")

TLDR

- Jefferies downgraded Apple stock from Hold to Underperform, lowering the price target to $205.16 from $205.82

- The firm believes investor expectations for the foldable iPhone 18 and the replacement cycle are unrealistic and already priced into the stock

- Jefferies raised iPhone unit growth forecasts to 7% for FY2025, 1% for FY2026, and -1% for FY2027

- Analysts expect a $100 price increase for iPhone 18 Pro and Pro Max models, which could pressure margins without major new features

- The new iPhone Air’s thin design has not resonated with consumers, making bullish predictions on foldable models risky

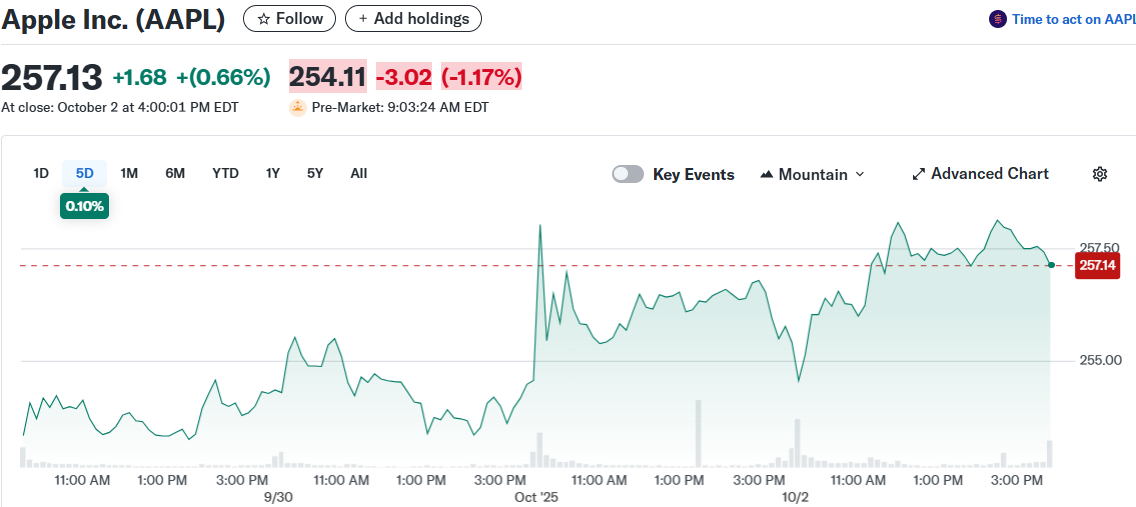

Jefferies downgraded Apple stock from Hold to Underperform on Friday, sending shares down 1.1% to $254.34 in premarket trading. The firm reduced its price target to $205.16 from $205.82.

The downgrade centers on what analyst Edison Lee calls “excessive expectations” for upcoming iPhone models. Current stock prices already reflect improved demand for the iPhone 17, according to the firm.

Jefferies believes the market has gotten ahead of itself regarding the foldable iPhone 18. The firm estimates iPhone 18 Fold sales will reach 12.5 million units per year.

Apple’s current stock price implies more than double that volume, creating unrealistic expectations. The stock was trading at $257.13 with a market cap of $3.82 trillion at the time of the downgrade.

The firm actually raised its iPhone unit growth forecasts. New projections show 7% growth for fiscal 2025, 1% for fiscal 2026, and -1% for fiscal 2027.

These numbers represent an upgrade from previous estimates of 5%, -3%, and 0%. Yet Jefferies still sees problems ahead.

Price Increases Without Innovation

A planned $100 price hike for iPhone 18 Pro and Pro Max models sits at the heart of Jefferies’ concerns. Without envelope-pushing features to justify the increase, demand could falter.

The firm argues that price-driven replacement cycles lack sustainability. This approach could squeeze margins if consumers balk at higher prices without compelling new technology.

Jefferies ran a discounted cash flow analysis after incorporating the iPhone 18 price increase. The result showed little change in fundamental value despite the higher prices.

iPhone Air Falls Flat

The iPhone 17 series introduces the iPhone Air, marketed as the thinnest iPhone ever made. Consumer response has been lukewarm at best.

This poor reception makes any optimistic view on foldable models risky, Jefferies warned. If buyers don’t care about ultra-thin designs, why would they embrace foldable phones?

The iPhone 17 is expected to benefit from a price cut on the base model. Jefferies attributes improved demand projections partly to this discount rather than innovative features.

The firm’s FY2025 revenue growth forecast stands at 6%. Financial health scores remain solid at 2.88 out of 5, but valuation concerns persist.

Apple stock trades near its 52-week high of $260.10. Jefferies considers the stock overvalued at current levels given the challenges ahead.

The firm’s cautious stance for fiscal years 2026 and 2027 reflects both the price increase strategy and conservative foldable iPhone projections. Market futures for the S&P 500 and Nasdaq Composite remained flat following the downgrade announcement.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants