Stock: Ackman Bets Big as Tariff Delays Boost Shares")

TLDR

- Amazon stock jumped 2.7% after Trump postponed 50% EU tariffs from immediate implementation to July 9, 2025, providing relief for companies with European business ties

- Bill Ackman’s Pershing Square invested nearly $1 billion in Amazon during Q1 2025, betting on the company’s long-term prospects despite current headwinds

- AWS revenue grew 17% year-over-year to $25 billion in Q1 2025, with operating income nearly doubling to $9.4 billion as cloud services drive profitability

- Amazon’s retail segment showed resilience with domestic revenue up 12% to $86.3 billion and operating income reaching $5 billion for the quarter

- Wall Street maintains a Strong Buy rating with an average price target of $240.62, implying 17% upside potential from current levels

Amazon shares have been making moves lately, and for good reason. The e-commerce and cloud giant caught a break when President Trump pushed back those hefty EU tariffs that had investors sweating.

The stock popped 2.7% in afternoon trading after news broke that the planned 50% tariff on European Union imports got delayed until July 9, 2025. Companies doing business across the pond breathed a collective sigh of relief.

This tariff reprieve comes at a perfect time for Amazon. The company has substantial European operations that would have felt the pinch from immediate cost pressures.

The shares closed at $206, marking a 2.5% gain from the previous session. Not bad for a single day’s work.

But here’s where things get interesting. While regular investors were celebrating the tariff delay, billionaire investor Bill Ackman was already making his move.

Ackman’s Pershing Square Capital Management dropped nearly $1 billion on Amazon stock during the first quarter of 2025. That’s not pocket change, even for a hedge fund legend.

$AMZN Bill Ackman announced yesterday that Pershing Square bought Amazon stock in April

The stock bottomed at a P/OCF of 16.9x on April 10 but remains close to decade lows pic.twitter.com/oVnCzF4y2j

— Stock Unlock (@stock_unlock) May 23, 2025

The timing of Ackman’s bet raises eyebrows. Amazon has been dealing with slowing AWS growth, fierce AI competition, and those tariff headaches that have kept the stock down year-to-date.

AWS Powers Through Despite Headwinds

Amazon Web Services continues to be the company’s cash cow. The cloud division posted $25 billion in revenue during Q1 2025, marking a solid 17% jump from the previous year.

Even more impressive was the profit picture. AWS operating income nearly doubled from $5.1 billion to $9.4 billion year-over-year.

That’s the kind of growth that gets investors excited. AWS now represents about 17% of Amazon’s total sales, but it punches way above its weight in terms of profitability.

The cloud computing market isn’t slowing down anytime soon. Industry projections show the sector growing at a 20.4% annual rate and potentially hitting $1 trillion in the coming years.

Amazon isn’t resting on its laurels though. The company is doubling down on AI through initiatives like its Bedrock platform and custom chips called Trainium. These moves should help AWS stay competitive against Microsoft Azure and Google Cloud.

Retail Division Shows Surprising Strength

While everyone focuses on AWS, Amazon’s retail business quietly delivered solid results. Domestic revenue climbed 12% year-over-year to $86.3 billion in the first quarter.

The real surprise was profitability. Amazon’s retail segment generated $5 billion in operating income, showing this historically low-margin business has found its groove.

Years of investment in fulfillment infrastructure are paying off. Faster shipping and lower transportation costs have transformed the economics of Amazon’s retail operations.

Amazon still dominates U.S. e-commerce with a commanding 37.6% market share. Walmart sits in distant second place at 6.4%. Competition from players like Temu is heating up, but Amazon’s lead remains substantial.

The company’s advertising business, largely tied to its retail ecosystem, grew 24% year-over-year. This high-margin revenue stream continues boosting overall profitability.

Amazon trades at a price-to-earnings ratio of 32.8, which looks reasonable compared to its historical range of 40 to 80. The stock has dropped 6.5% year-to-date and sits 14.9% below its 52-week high of $242.06.

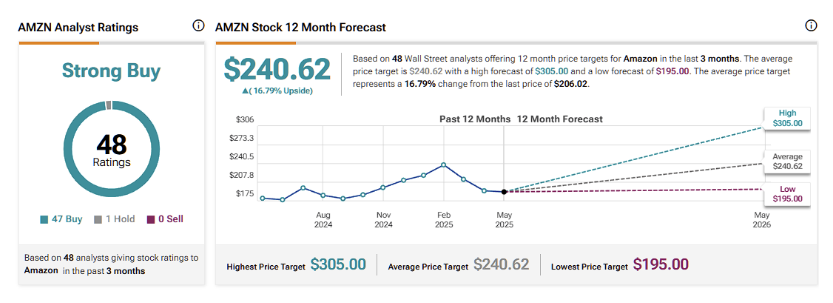

Wall Street analysts remain bullish with a Strong Buy consensus rating based on 47 Buy ratings, one Hold, and zero Sell recommendations. The average price target of $240.62 suggests 17% upside potential over the next twelve months.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants