Stock: Can New CEO Elliott Hill Deliver Earnings Turnaround?")

TLDR

- Nike reports Q3 earnings Tuesday after market close with analysts expecting $11 billion revenue, down 5% year-over-year

- Company beat revenue expectations by 3.4% last quarter with $11.1 billion in sales, though down 12% annually

- Stock has declined 6.7% over the past month while broader consumer discretionary sector gained 1.2%

- Nike brought back longtime executive Elliott Hill as CEO to lead turnaround efforts

- Despite recent struggles, the company offers a 2.25% dividend yield and potential for long-term growth in developing markets

Nike faces a crucial earnings test this Tuesday as investors look for signs of recovery from the athletic apparel giant’s recent struggles. The company will report Q3 results after the market closes, with analysts expecting revenue of $11 billion.

This represents a 5% decline from the same quarter last year. However, this would mark an improvement from the 10.4% decrease Nike recorded in the prior year’s comparable quarter.

Last quarter, Nike managed to beat revenue expectations by 3.4%. The company reported $11.1 billion in sales, though this still represented a 12% year-over-year decline.

Analysts are projecting adjusted earnings of $0.27 per share for the upcoming quarter. Wall Street estimates have remained relatively stable over the past 30 days.

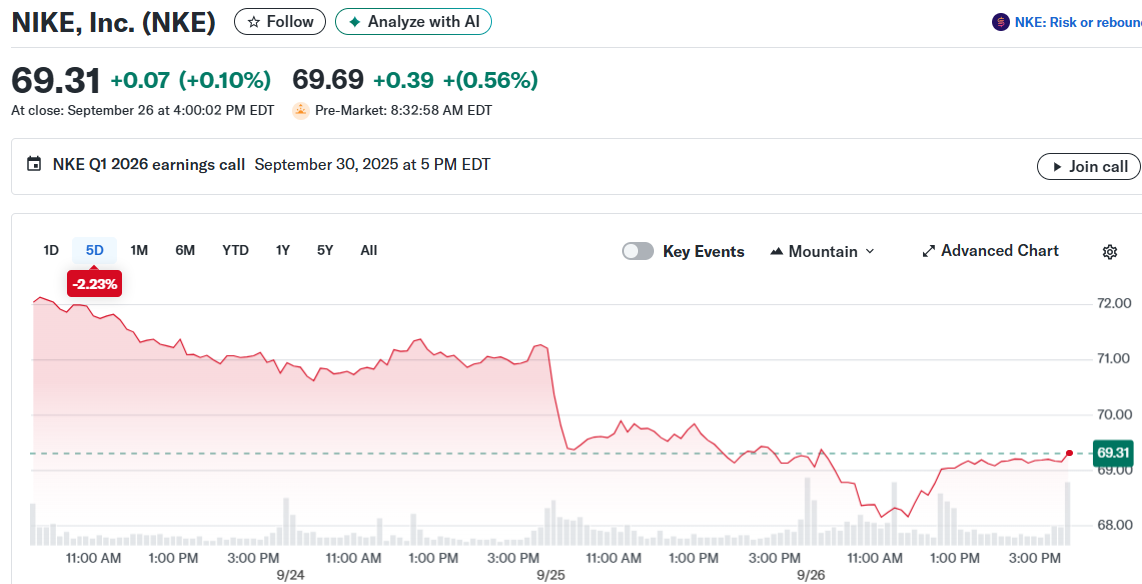

Nike’s stock performance has lagged the broader market recently. The shares have dropped 6.7% over the past month while the consumer discretionary sector has gained 1.2%.

The company currently trades at $69.31, well below the average analyst price target of $79.57. This gap suggests potential upside if Nike can deliver better-than-expected results.

Leadership Change Brings Hope

The company made a significant leadership move during fiscal 2025. Nike brought back longtime executive Elliott Hill to serve as CEO, replacing previous leadership.

Hill’s deep company knowledge and established relationships with key partners position him well for the turnaround effort. His return has generated optimism among investors who believe he can accelerate the recovery process.

Nike has faced multiple headwinds in recent years. These include a lack of product innovation, softer demand for sportswear, and strained relationships with wholesale customers.

The company’s recovery in China has also been slower than expected. Despite these challenges, Nike maintains strong brand recognition and pricing power globally.

Long-Term Growth Potential

Looking beyond the immediate earnings results, Nike offers compelling long-term prospects. The company continues to see opportunity in developing markets as middle-class populations expand.

China and Latin America represent particularly attractive growth regions. These markets offer large populations with increasing disposable income for athletic apparel and footwear.

Nike’s dividend yield of 2.25% provides income while investors wait for the turnaround to materialize. The company has historically maintained its dividend payments even during challenging periods.

The stock has declined 25% over the past three years. This sell-off has created what some analysts view as an attractive entry point for long-term investors.

Nike’s gross margin of 42.21% remains healthy despite recent pressures. The company’s market capitalization stands at $102 billion, reflecting its position as an industry leader.

Trading volume has been lighter than average recently. The stock’s 52-week range spans from $52.28 to $89.75, showing the volatility investors have experienced.

Elliott Hill’s appointment as CEO represents the most recent development in Nike’s turnaround strategy.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants