Stock: Gets VIP Pass to Nvidia’s “Cool Kids Club” Says Analyst")

TLDR

- Loop Capital initiated coverage on CoreWeave with a Buy rating and $165 price target, seeing 36% upside potential

- Analyst calls CoreWeave the largest “Neocloud” being invited into Nvidia’s “Cool Kids Club”

- Stock has risen over 25% in the past month and 211% since March IPO

- CoreWeave recently secured a $6.3 billion order from Nvidia for cloud computing capacity

- Wall Street maintains Moderate Buy consensus with average price target of $142.32

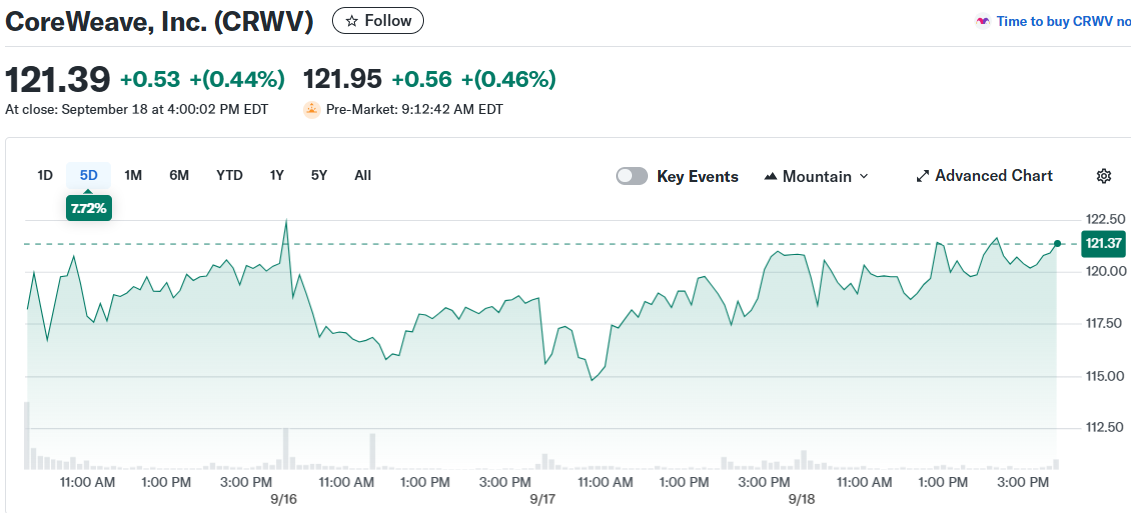

CoreWeave shares climbed 0.3% to $121.70 in premarket trading Friday following fresh analyst coverage from Loop Capital. The investment firm started coverage with a Buy rating and set a price target of $165.

The price target represents roughly 36% upside from the stock’s previous close. Loop Capital joins Raymond James in recent coverage initiations, with Raymond James assigning an Outperform rating and $130 price target just days earlier.

Loop Capital analyst Ananda Baruah expects CoreWeave to deliver material profit upside compared to current Wall Street estimates. The five-star analyst sees expansion potential in the company’s enterprise value to EBITDA multiple.

CoreWeave has gained over 25% in the past month alone. The stock has been one of this year’s biggest IPO success stories, climbing more than 211% since going public in March.

The rally picked up steam this week after CoreWeave disclosed a new agreement with Nvidia. The deal provides Nvidia access to unsold cloud computing capacity from CoreWeave’s infrastructure.

Analyst Sees “Cool Kids Club” Invitation

Baruah described CoreWeave as the largest of several “Neoclouds” getting invited into what he calls a “Cool Kids Club.” This exclusive group includes chip giant Nvidia, major hyperscalers, and leading AI laboratories.

The analyst believes the market underestimates how committed hyperscalers and AI labs remain to pushing innovation forward. He also cited Nvidia’s upcoming Blackwell platform as a positive factor for neocloud companies.

Baruah projects CoreWeave will generate $17.9 billion in revenue and $12.8 billion in EBITDA by 2027. These forecasts slightly exceed Wall Street’s consensus estimates of $17.8 billion and $12.7 billion respectively.

His price target uses a 10x enterprise value to EBITDA multiple based on 2027 estimates. The analyst expects this valuation framework to gain importance as 2026 approaches.

Recent Business Developments

CoreWeave recently secured a major $6.3 billion order from Nvidia for cloud computing services. This agreement strengthens the partnership between the two companies and provides CoreWeave with substantial revenue visibility.

The company has also committed to investing in UK data center infrastructure. This investment forms part of a broader $42 billion pledge from major US tech companies including Nvidia, Microsoft, and OpenAI.

Currently, nine of 25 analysts covering CoreWeave rate it Buy or higher. Thirteen analysts assign Hold ratings while three rate it Sell or Strong Sell, according to Koyfin data.

The average analyst price target stands at $127.56 across all coverage. This suggests Wall Street sees continued upside potential despite the stock’s strong year-to-date performance.

Citizens JMP recently upgraded CoreWeave from Hold to Buy, adding to the positive analyst sentiment. The upgrade reflects growing confidence in the company’s position within the AI infrastructure market.

Wall Street maintains a Moderate Buy consensus rating on CoreWeave stock based on 13 Buy recommendations, 12 Holds, and two Sell ratings.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants