Stock: Why Rocket Lab Crashed Back to Earth on Wednesday")

TLDR

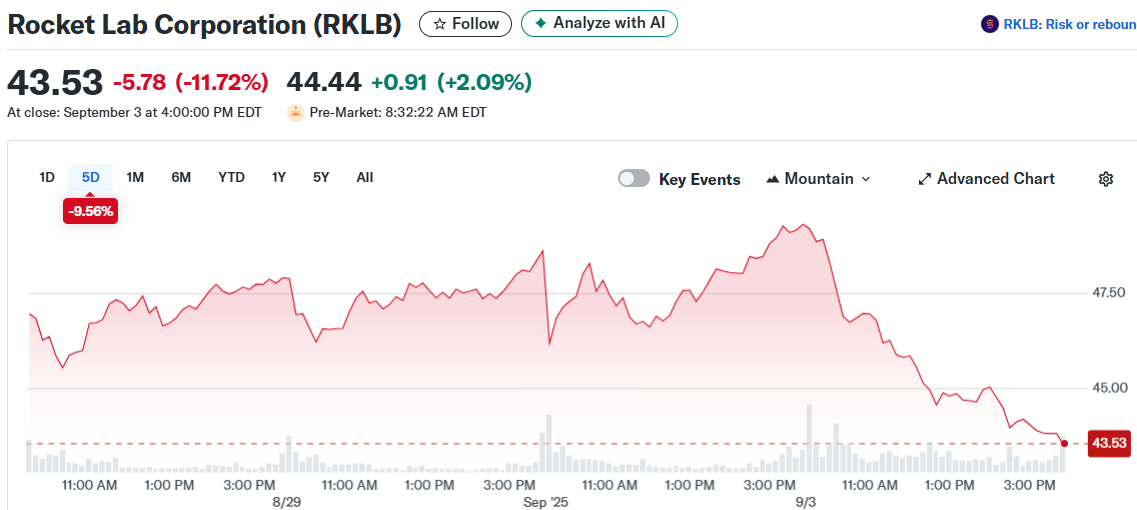

- Rocket Lab stock fell 12% on Wednesday despite no direct company news, potentially due to SpaceX receiving expanded launch approvals

- The company reported record Q2 revenue of $144.5 million, up 36% year-over-year, though losses widened to 13 cents per share

- Stock remains up over 70% year-to-date with strong institutional buying and 540 mutual funds holding shares

- Analysts maintain Strong Buy rating with average price target of $30.20, though some targets reach $60

- Neutron rocket development continues on track for late 2025 launch with infrastructure already in place

Rocket Lab stock took a nosedive Wednesday, falling 12% in what appears to be a reaction to competitive pressures rather than company-specific news. The space launch company rebounded 2.7% in Thursday’s pre-market trading, suggesting investors view the decline as an overreaction.

The selloff may have been triggered by the FAA’s approval of SpaceX’s plan to more than double Falcon 9 launches from Florida. This regulatory green light gives SpaceX expanded capacity with its rocket that will directly compete with Rocket Lab’s upcoming Neutron vehicle.

Falcon 9 launches 28 @Starlink satellites from Florida pic.twitter.com/mSLcPg7I58

— SpaceX (@SpaceX) September 3, 2025

The timing of the approval creates additional competitive pressure as Rocket Lab prepares for Neutron’s debut in late 2025. SpaceX’s head start with increased launch frequency could make it harder for Rocket Lab to capture market share in the medium-lift rocket segment.

Despite Wednesday’s drop, Rocket Lab continues to show strong operational momentum. The company posted record second-quarter revenue of $144.5 million, representing 36% growth from the previous year.

The revenue boost came from both launch services and its space systems division. Rocket Lab has completed 70 launches to date and operates three launchpads across New Zealand and the United States.

However, profitability remains elusive. The company’s second-quarter loss of 13 cents per share was its largest in eight quarters, though analysts expect improvement ahead.

Financial Outlook Improves

Wall Street projects losses will narrow to eight cents per share in the third quarter. The deficit should continue shrinking to three cents per share over the following four quarters.

For 2025, analysts forecast a full-year loss of 43 cents per share. That figure is expected to drop dramatically to just nine cents per share in 2026, suggesting the company is approaching profitability.

Management guided for third-quarter revenue between $145 million and $155 million. CEO Peter Beck expressed confidence that strategic investments will drive growth opportunities toward long-term profitability.

The stock shows strong institutional support despite recent volatility. Rocket Lab holds an A+ Accumulation/Distribution Rating, indicating heavy institutional buying over the past 13 weeks.

Mutual fund ownership has grown for four consecutive quarters. As of June, 540 funds held positions in the stock, including major players like Fidelity Contrafund.

Analyst Sentiment Remains Positive

Five-star analyst Sujeeva De Silva from Roth MKM recently raised his price target from $50 to $60 with a Buy rating. He cited progress on Neutron development and noted that both support systems and launchpad infrastructure are already operational.

The analyst consensus remains bullish with nine Buy ratings and three Holds issued over the past three months. The average price target sits at $30.20, though individual targets range much higher.

Rocket Lab stock carries a 99 IBD Relative Strength Rating, the highest possible score. The company has gained approximately 81% year-to-date, making it one of the top performers in the aerospace sector.

The stock trades with high volatility, showing a 21-day Average True Range of 7.4%. This exceeds IBD’s preferred 5% threshold but reflects the dynamic nature of the space industry.

Management owns 11% of outstanding shares, demonstrating leadership confidence in the company’s direction. The insider ownership provides additional alignment between executives and shareholders.

Technical analysis shows the stock consolidating in an early-stage pattern with a potential buy point at $53.44. The recent pullback brought shares near the 21-day exponential moving average while holding above the 50-day line.

Volume patterns support the bullish thesis, with heavier trading on up days as institutional investors accumulate positions. The 1.5 up/down volume ratio over 50 days indicates positive demand dynamics.

Rocket Lab’s most recent launch occurred in late August from its New Zealand facility, maintaining its operational cadence. The company has 233 satellites currently deployed through its launch services.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants