Stock: Tumbles as EV Giant Slashes 2025 Sales Target by 16%")

TLDR

- BYD cut its 2025 vehicle sales target from 5.5 million to 4.6 million vehicles, a 16% reduction

- Company’s Hong Kong shares fell 3.2% following the news of the target cut

- BYD reported a 30% drop in quarterly profit last week, its first decline in over three years

- Sales growth is slowing due to intense competition from rivals like Geely and new market entrants

- The revised target would represent BYD’s slowest annual growth since 2020

BYD Company has quietly cut its 2025 vehicle sales target to 4.6 million units, down from the 5.5 million vehicles it projected to analysts in March. The 16% reduction marks a turning point for China’s largest automaker, which has experienced explosive growth over the past four years.

The revised target was communicated internally to company staff and select suppliers last month. Two sources familiar with the matter confirmed the change, though they noted the figure could still shift based on market conditions.

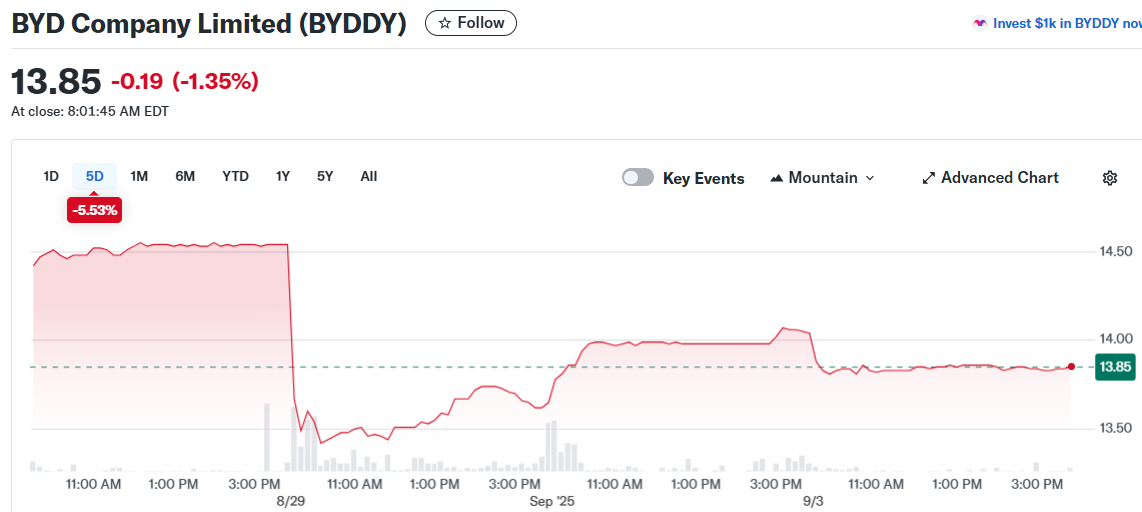

BYD’s Hong Kong-traded shares dropped 3.2% after Reuters first reported the target cut. The stock had already been down 1.4% before the news broke. American depositary receipts trading under ticker BYDDY fell 1.35% in US markets.

The lower sales goal comes after a challenging period for the Tesla rival. Last week, BYD reported a 30% drop in quarterly profit, marking its first decline in more than three years. The company has only achieved 52% of its original 5.5 million vehicle target through the first eight months of 2025.

Competition Heats Up in Chinese Market

BYD faces mounting pressure from established rivals and new entrants in China’s crowded electric vehicle market. Geely Automobile has been particularly aggressive, with its economy car sales jumping 90% year-over-year in July while BYD’s sales in the same segment fell 9.6%.

Geely recently raised its own 2025 sales target to 3 million vehicles from 2.71 million. Other competitors like XPeng and newcomer Xiaomi are also gaining traction with their latest model launches.

The competition has intensified as Beijing moved to limit the heavy discounting that BYD and other manufacturers used to defend market share. This regulatory shift has removed one of BYD’s key competitive weapons during the ongoing price war.

BYD’s production has also shown signs of strain. Manufacturing output declined for the second consecutive month in August, representing the first back-to-back monthly contraction since 2020. The company has reportedly slowed production and delayed capacity expansion at its Chinese facilities.

Analysts Remain Cautiously Optimistic

Despite the challenges, some analysts view the target reduction as a necessary recalibration rather than a fundamental problem. Bernstein analyst Eunice Lee called the lower sales goal a “near-term clearing event” for the stock.

Lee suggested the new target aligns more closely with investor expectations and may be more achievable given current market conditions. The revised goal still represents a 7% increase from last year’s sales, though it would mark BYD’s slowest annual growth rate since 2020.

Deutsche Bank expects BYD to sell 4.7 million vehicles this year, while Morningstar forecasts 4.8 million units. Both estimates are close to the company’s new internal target.

Wall Street maintains a generally positive outlook on BYD stock. Analysts have assigned a Moderate Buy consensus rating based on five Buy recommendations and one Hold rating issued over the past three months. The average price target of $17.56 per share suggests potential upside of 26.51%.

The next few months will prove critical for BYD as the peak sales season approaches. September and October traditionally represent the strongest period for vehicle sales in China, giving the company an opportunity to demonstrate whether it can compete effectively without relying on aggressive discounting strategies.

BYD’s economy vehicle segment, which accounts for the bulk of its domestic sales, will face particular scrutiny. Cars priced under 150,000 yuan ($21,000) have become the primary battleground for Chinese EV manufacturers.

The company built its reputation by keeping production costs low through vertical integration, manufacturing many components in-house. This strategy allowed BYD to offer cutting-edge features while maintaining competitive pricing.

BYD’s deliveries in July and August remained flat compared to the same period last year. Production data for August showed continued weakness, extending the company’s recent manufacturing slowdown into a second consecutive month.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants