Stock: Wall Street Eyes 20% Gains Ahead of August 29 Earnings. Here’s Why")

TLDR

- Alibaba stock has surged 47% year-to-date with analysts projecting over 20% additional upside potential

- The company reports Q1 FY26 earnings on August 29 with expected earnings of $2.06 per share on $35.35 billion revenue

- Hong Kong Stock Exchange approved initial plans for Alibaba to spin off autonomous driving unit Banma Network Technology

- Analysts warn of margin pressure from intense competition in food delivery and quick retail sectors

- Wall Street maintains Strong Buy consensus with 12 Buy ratings and average price target of $148.55

Alibaba’s stock has been on a tear this year, climbing over 47% as investors bet on the Chinese e-commerce giant’s AI and cloud initiatives. Wall Street analysts remain bullish heading into the company’s August 29 earnings report.

The consensus forecast calls for earnings of $2.06 per share on revenues of $35.35 billion for the first quarter. That represents a 5% revenue increase compared to the same period last year.

Alibaba’s cloud business has been a key growth driver, with analysts projecting 20% revenue growth for the June quarter. The company has committed over $50 billion over three years to AI infrastructure investments.

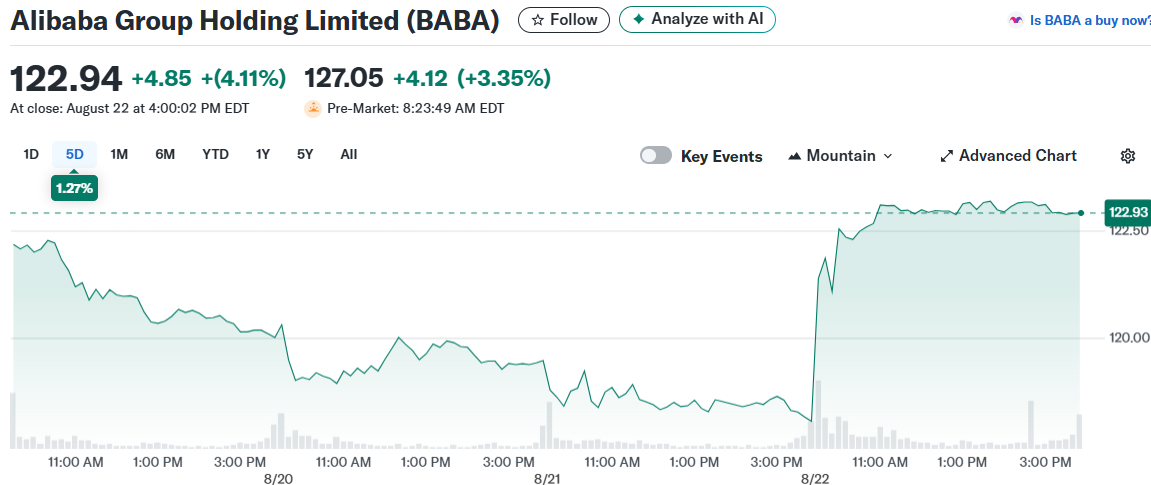

The stock recently broke back above its 21-day moving average after a strong Friday trading session. Shares gained more than 3% to reach $122.47, putting the stock near a technical buy point of $123.99.

Chinese tech stocks broadly rallied following the launch of DeepSeek’s new AI model optimized for domestic chips. This helped ease concerns about U.S. semiconductor export restrictions hampering Chinese AI development.

Strategic Moves and Spin-Offs

Alibaba received initial approval from Hong Kong regulators to spin off Banma Network Technology, its autonomous driving unit. The IPO would reduce Alibaba’s stake from 44.7% to roughly 30%.

This move could improve capital efficiency and allow Alibaba to focus resources on core cloud and AI operations. The spin-off would give investors clearer visibility into Banma’s standalone business performance.

The strategic restructuring comes as Alibaba faces mounting competitive pressure in its home market. Rivals like JD.com have intensified battles for market share in food delivery and quick commerce.

Margin Pressure Concerns

Top-rated Mizuho analyst Wei Fang recently cut his price target from $160 to $149, citing rising margin pressure. Competition in local commerce, particularly food delivery, is weighing on profitability across major players.

Fang expects Q1 margins to decline sharply from the previous quarter. He warns this margin strain could persist through 2025 and into 2026 without regulatory intervention to ease pricing wars.

Mizuho lowered its Q1 EBITDA forecast from 55 billion yuan to 45 billion yuan. The firm also reduced its fiscal 2027 EBITDA projection to 231 billion yuan.

Despite margin concerns, 92% of Wall Street analysts maintain bullish ratings on Alibaba’s fundamentals. They point to steady consumer demand as a supporting factor for long-term growth.

The average analyst price target of $148.55 implies 20.83% upside potential from current trading levels. Alibaba commands a Strong Buy consensus rating with 12 Buy recommendations and one Hold rating.

China’s broader economic headwinds continue to create uncertainty for consumer spending patterns. This backdrop has intensified competition among e-commerce platforms for wallet share.

The earnings report on August 29 will provide fresh insights into how well Alibaba is navigating these competitive dynamics while investing in future growth areas.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants