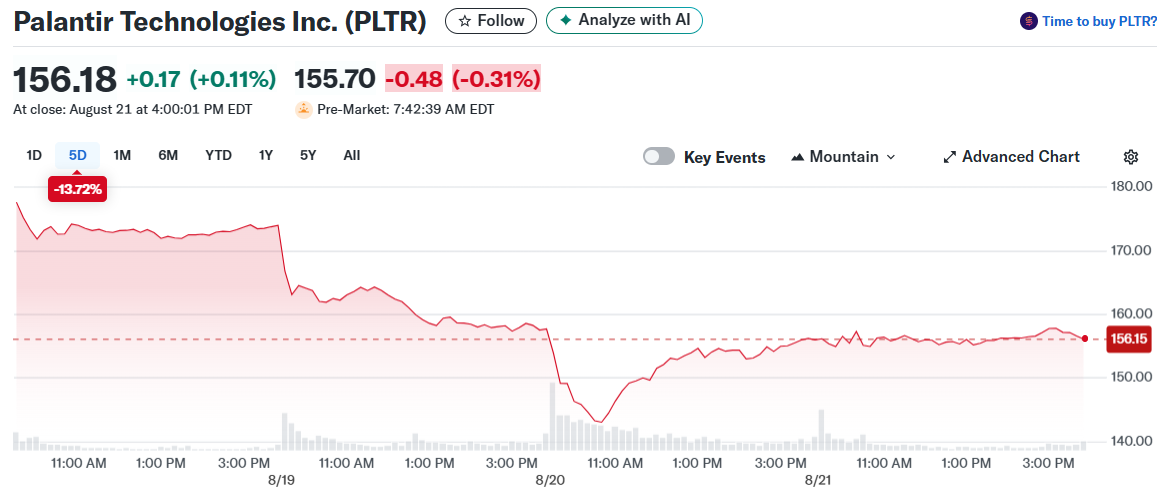

Stock Plunges 13% Despite CEO’s Bold 10x Revenue Growth Promise")

TLDR

- Palantir stock fell 13% this week following broader tech sell-off and valuation concerns

- CEO Alex Karp targets 10x revenue increase while cutting workforce by 12%

- Company secured $2.27 billion in Q2 contracts, up 140% year-over-year

- Citron Research criticizes PLTR’s 500x earnings multiple vs OpenAI’s 17x sales ratio

- Revenue jumped 48% in Q2 as company leads $153 billion AI software platforms market

Palantir Technologies stock has tumbled 13% this week as investors grapple with the AI company’s stretched valuation despite impressive growth metrics. The data analytics giant dropped 5% Wednesday after losing nearly 8% Tuesday, even as fundamentals remain strong.

CEO Alex Karp recently outlined an ambitious expansion strategy during a CNBC interview. The company plans to multiply revenue by 10 times while simultaneously reducing headcount by 12%. This aggressive target reflects Palantir’s confidence in its AI platform capabilities and operational efficiency.

The revenue goal appears within reach based on historical performance. Palantir generated $1.1 billion annually in 2020. By Q2 2025, the company produced over $1 billion in a single quarter. Full-year 2025 revenue is projected at $4.1 billion, representing nearly 4x growth in five years.

This translates to a 30% compound annual growth rate since 2020. Achieving 10x growth from current levels would require reaching approximately $41 billion in annual revenue. Given the AI software platforms market is expanding at 41% annually toward $153 billion by 2028, Karp’s target seems realistic within a decade.

Strong Contract Momentum Fuels Growth

Palantir’s contract performance showcases robust demand for its AI solutions. The company signed $2.27 billion in new deals during Q2, jumping 140% year-over-year and exceeding quarterly revenue. This contract backlog positions Palantir for sustained growth ahead.

Revenue acceleration has been particularly strong since launching commercial AI offerings two years ago. Q2 revenue climbed 48% year-over-year, demonstrating the company’s ability to capitalize on AI adoption trends.

Operating margins improved eight percentage points in the first half of 2025. This margin expansion stems from growing customer base and increased spending per client. Analysts project 58% earnings growth in 2025 to $0.65 per share.

Valuation Reality Check Hits Stock

Short-seller Citron Research targeted Palantir’s valuation in a recent report. The firm highlighted the stark difference between Palantir’s nearly 500x earnings multiple and OpenAI’s 17x sales ratio following its latest funding round.

This comparison gained traction as investors question whether Palantir deserves a premium valuation over the company driving the AI revolution. OpenAI’s lower multiple despite being the AI sector’s epicenter raises questions about Palantir’s current pricing.

Broader economic concerns have intensified pressure on high-multiple tech stocks. Recent jobs data suggesting economic slowdown prompted rotation away from richly valued technology companies. Palantir’s premium valuation makes it particularly vulnerable during market uncertainty.

Early investors have seen remarkable gains, with $100 invested at the 2020 public debut now worth $1,660. However, this 1,560% return has pushed shares to levels that require continued exceptional execution to justify.

The company’s market capitalization now sits at $371 billion, trading at $156.02 per share as of Wednesday’s close.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants