Stock: Is It Too Late to Buy After Its Historic Rally?")

TLDR

- Nvidia stock jumped nearly 70% since April 4, recovering from a 20% Q1 2025 decline to trade near record highs around $160

- The company became the world’s largest by market cap last week, surpassing Microsoft with a valuation over $3.3 trillion

- Q1 2025 revenue hit $44 billion (up 70% year-over-year) with data center sales soaring 73% driven by AI demand

- Net income exploded to $18.7 billion with a 52% profit margin, while holding over $50 billion in cash

- Analysts expect the stock could reach $200 by year-end based on projected 54% revenue growth and strong AI market demand

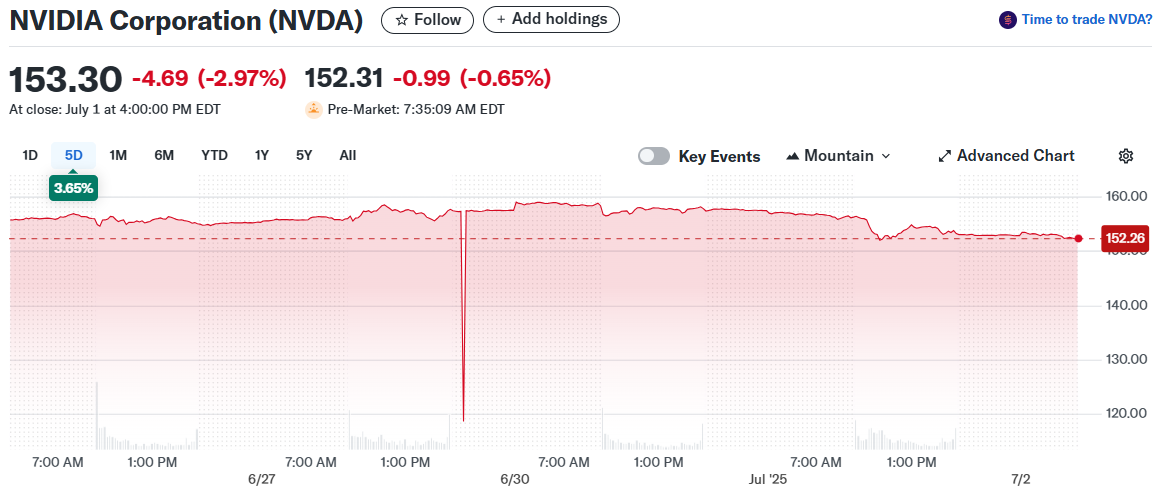

Nvidia stock has staged a remarkable comeback since its rough start to 2025. After falling 20% in the first quarter, shares have rocketed nearly 70% higher since April 4. That means investors who bought $10,000 worth of stock three months ago are sitting on almost $7,000 in profit.

The graphics chip maker now trades near record highs around $160 per share. It’s a stunning turnaround for a company that faced early-year concerns about competition from China’s DeepSeek chatbot and potential tariff impacts.

Last week marked a historic milestone. On June 27, Nvidia surpassed Microsoft to become the world’s largest company by market value. The achievement puts its total market capitalization above $3.3 trillion.

NVIDIA is now the world’s most valuable company after flipping Microsoft pic.twitter.com/V1mwQ4OHYY

— Dexerto (@Dexerto) June 25, 2025

Few would have predicted a graphics chip designer from California would eclipse tech giants like Apple and Microsoft. The company started in 1993 building processors for PC gaming but spotted the bigger opportunity in artificial intelligence hardware.

Financial Performance Powers Stock Rally

Nvidia’s latest quarterly results justify the stock price surge. Q1 2025 revenue reached $44 billion, up an impressive 70% from the same period last year. Data center sales drove most of the growth, jumping 73% as companies rushed to buy AI chips.

Net income hit $18.7 billion, giving Nvidia a 52% profit margin. That level of profitability rarely gets seen at this scale.

The balance sheet looks equally strong. Nvidia holds over $50 billion in cash with a debt-to-equity ratio of just 0.12. This financial flexibility gives management plenty of room to invest in new products and weather any market storms.

The AI boom continues to fuel demand for Nvidia’s processors. These chips power everything from ChatGPT to autonomous vehicles and data centers worldwide. The company controls between 70% and 95% of the high-end AI chip market, depending on estimates.

Wall Street expects the momentum to continue. Analysts project full-year revenue of $200 billion, representing a 54% increase from 2024. Earnings per share should jump 43% to $4.29.

New Products Maintain Competitive Edge

Management keeps launching upgraded chip architectures to stay ahead of competitors. The company’s Blackwell technology replaced the older Hopper design last year. Now Nvidia is already moving to Blackwell Ultra with plans for the next-generation Rubin chips in 2026.

This constant innovation helps maintain relationships with major clients like Microsoft and Amazon. While alternatives exist, the biggest tech companies rely on Nvidia’s most powerful processors for their AI operations.

The AI market opportunity continues expanding. Research firm Statista projects the sector will grow at a 26.6% annual rate over the next five years, reaching $1 trillion in total value. Nvidia stands to capture a large portion of that growth.

Some risks do exist. Company insiders, including CEO Jensen Huang, have sold over $1 billion worth of stock in the past year. More than $500 million got sold in June alone. This could represent normal portfolio diversification rather than lack of confidence in the business.

Current valuation metrics show Nvidia isn’t cheap. The stock trades at a price-to-earnings ratio around 50 and price-to-book ratio near 45. These numbers make it one of the most expensive mega-cap stocks on traditional measures.

Bulls argue the premium valuation makes sense given explosive growth rates and dominant market position. If current trends continue, the stock could hit $200 before year-end. That would represent a 27% gain from current levels around $153.

Management guided for second-quarter growth to slow but remain strong at 50% year-over-year. Wall Street expects earnings per share of $1.00, up from $0.68 in the same quarter last year. Nvidia has a track record of beating analyst expectations, which could drive shares even higher.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants