Stock: Why This 23% Drop Could Be a Buying Opportunity")

TLDR

- AMD stock has fallen 23% over the past year but shows momentum for a potential breakout toward $200 all-time highs

- Data Center revenue jumped 57% year-over-year to $3.7 billion in Q1, driven by AI demand and partnerships with Microsoft, Meta, and Oracle

- Client segment surged 68% to $2.3 billion in Q1, powered by new Ryzen AI processors across 50+ laptop models

- Recent AI event showcased MI350 series and MI400 “Helios” rack-scale solution, with OpenAI’s Sam Altman endorsing the MI450X

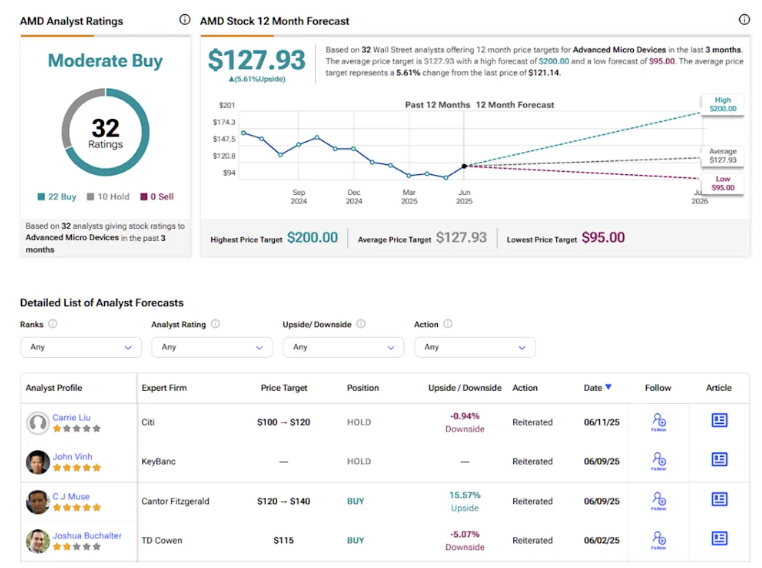

- Wall Street maintains Moderate Buy rating with $127 average price target, though some analysts see greater upside potential

Advanced Micro Devices faces a pivotal moment as the chip maker attempts to prove its AI credentials. The stock has dropped 23% over the past year, leaving investors wondering if the company can capitalize on the artificial intelligence boom.

Recent quarterly results paint a different picture than the stock performance suggests. AMD’s Data Center segment generated $3.7 billion in revenue during Q1, marking a 57% year-over-year increase.

The growth comes from surging demand for EPYC CPUs and Instinct GPUs. CEO Lisa Su highlighted partnerships with tech giants Microsoft, Meta, and Oracle as key drivers.

🚨 $MSFT announces its new portable Xbox, ROG Ally

Powered by the latest $AMD APU pic.twitter.com/MepXCQoRG3

— Daniel Romero (@HyperTechInvest) June 10, 2025

These hyperscalers increasingly rely on AMD chips to power their AI workloads. The momentum represents more than a temporary spike in demand.

Data center revenue nearly doubled in 2024 to $12.6 billion. Q1 results continue this upward trajectory, suggesting sustainable growth ahead.

Data Center Dominance Drives Growth

AMD strengthens its position through strategic acquisitions like Untether AI and Brium. These moves expand capabilities in both AI hardware and software development.

The upcoming Instinct MI350 series generates buzz for potentially rivaling Nvidia in AI infrastructure. Industry watchers see this as a critical test for AMD’s competitiveness.

Seven of the ten largest AI players now use AMD chips. This includes early adopter Oracle, which plans to implement AMD’s upcoming rack-scale solutions.

The Client segment also shows impressive recovery. Q1 client revenue surged to $2.3 billion, up 68% year-over-year.

New “Zen 5” Ryzen processors drive strong adoption across laptops and desktops. AMD’s Ryzen AI Max chips power over 50 AI-enabled laptop models expected this year.

Recent AI Event Shows Mixed Results

AMD’s recent Advance AI event failed to ignite investor enthusiasm despite showcasing new technology. The company unveiled the MI350 series and ROCm 7 software improvements.

The event also teased the upcoming MI400 “Helios” rack-scale solution. OpenAI’s Sam Altman made a surprise appearance, endorsing the MI450X chip.

Cowen analyst Joshua Buchalter sees the muted market reaction as missing the bigger picture. He believes AMD is laying important groundwork for AI market participation.

Buchalter compares the current MI350 and MI400 developments to AMD’s early CPU platforms. Those products eventually led to the company’s breakthrough against Intel.

The analyst acknowledges this remains a “show-me” story requiring proof of execution. AMD must demonstrate it can scale rack-scale solutions successfully.

Altman’s enthusiasm for the MI450X provides early validation. The OpenAI CEO highlighted the chip’s potential for both inference and training applications.

AMD showcased upgrades in ROCm 7 and pointed to its growing developer community. These improvements address previous barriers to wider Instinct GPU adoption.

At current valuation levels, AMD trades at 31 times this year’s consensus earnings per share of roughly $4. Analysts project 44% EPS growth by 2026 to an estimated $5.71.

This forward growth would bring the price-to-earnings ratio down to 22 times 2026 estimates. The multiple appears reasonable for a company positioned to benefit from multi-year AI trends.

Wall Street maintains a Moderate Buy consensus rating with 22 Buy and 10 Hold recommendations. The average price target of $127.23 suggests 11% upside potential.

Cowen’s Buchalter assigns a Buy rating with a $115 price target. His analysis suggests AMD is making necessary moves to become the merchant alternative to Nvidia.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants