TLDR

- Meta Platforms remains JPMorgan’s top pick with increased price target to $675, driven by AI enhancements in advertising

- Amazon reported better than expected Q1 results with AWS operating margin reaching all-time high of 39.5%

- Roku is positioned well in the connected TV industry with increasing diversification of platform revenue

- Nvidia’s stock price has decreased to 26x forward earnings estimates, down from 50x earlier this year

- Target has grown earnings despite consumer challenges and has invested in store renovations and digital fulfillment

Market Volatility Creates Investment Opportunities

In the midst of ongoing market volatility, top Wall Street analysts are pointing to several tech stocks that show solid growth potential. Despite the Federal Reserve’s caution about economic uncertainty and the impact of tariff wars shaking global markets, certain companies continue to demonstrate resilience and strong performance.

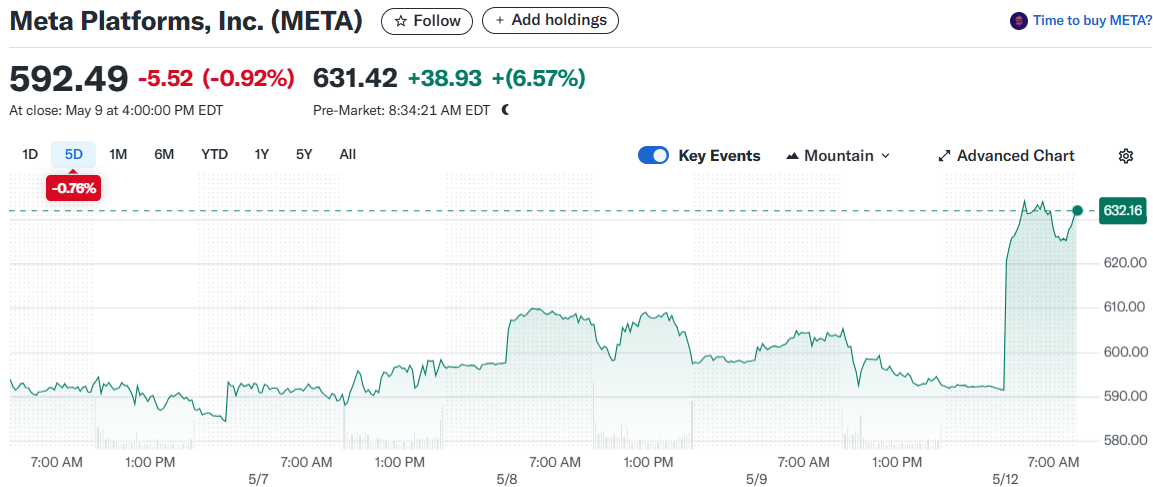

Meta Platforms (META) has emerged as a standout performer, surpassing analysts’ estimates for the first quarter of 2025. JPMorgan analyst Doug Anmuth has reaffirmed Meta as his firm’s top pick, raising the 12-month price target to $675 from $610.

The social media giant’s success can be attributed to its artificial intelligence ad enhancements, such as Andromeda and GEM, which are having a major impact on monetization. Meta’s CEO Mark Zuckerberg stated that the company is well-positioned to navigate ongoing challenges.

Meta’s scaled advertiser base, high-performance platform, and vertical agnostic inventory make it particularly well-suited for tough macro environments. AI is driving early gains in Meta’s advertising and engagement, with future progress expected in business messaging and Meta AI.

While Meta increased its full-year capital expenditure guidance, the company has a track record of generating returns on increased spending. This justifies the higher investment given the company’s strong results and progress on its AI roadmap.

Cloud Computing Giants Show Strength

Amazon (AMZN) also delivered better-than-expected Q1 2025 results, although it issued softer guidance for the second quarter, citing tariff concerns. JPMorgan maintained a buy rating on Amazon and raised its price target to $225 from $220.

Amazon’s AWS cloud computing division saw revenue growth deceleration to 17% in Q1 from 19% in Q4, but this was offset by strong profitability. AWS operating margin reached an all-time high of 39.5% in the first quarter.

The e-commerce and cloud giant has taken measures to mitigate tariff impacts, including pulling forward inventory. Amazon remains focused on broad selection, low pricing, and fast delivery, with the company typically emerging from uncertain macro periods with greater market share gains.

Amazon’s revamped cost structure and shift to a regional fulfillment model have helped lower overall costs. The company’s investments in AI have brought AWS to a $117 billion annual revenue run rate, offering customers a broad range of AI products and services.

In the streaming sector, Roku (ROKU) reported a modest revenue beat and narrower-than-anticipated loss for Q1, though it trimmed its full-year revenue outlook. Wedbush Securities analyst Alicia Reese remains bullish, highlighting that Roku maintained its Platform revenue and adjusted EBITDA guidance.

Roku’s acquisition of Frndly TV for $185 million in cash is expected to close in Q2, adding a subscription streaming service with live TV, on-demand video, and cloud-based DVR to its portfolio.

Investment Opportunities Amid Market Uncertainty

The current market uncertainty presents opportunities for long-term investors to purchase quality companies at reasonable prices. Nvidia (NVDA), the leading AI chip company, now trades at 26x forward earnings estimates, down from 50x earlier this year.

Despite economic uncertainty, the AI boom continues with analysts forecasting the market to reach $2 trillion in less than 10 years. Nvidia’s dominance in the AI chip market, focus on innovation, and successful rollout of its Blackwell chip architecture position it well for continued growth.

Target (TGT) has also shown resilience, growing earnings despite challenges in the retail sector. The company has invested in store renovations and digital sales, resulting in almost $30 billion in sales growth over the past five years.

Target’s portfolio of owned brands contributes to its success, with more than 40 brands and about a quarter generating at least $1 billion in sales annually. These brands allow Target complete control over production and marketing, keeping costs low and profits high.

Amazon’s e-commerce and cloud computing businesses continue to benefit from strategic decisions made in recent years. The company’s regional fulfillment model has lowered costs, and AWS investments in AI are yielding strong results.

In the most recent quarter, Amazon’s net sales rose 9% to over $155 billion. Trading at only 31x forward earnings estimates, Amazon presents an attractive opportunity for investors.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants