Key Takeaways

- Stock index futures declined Wednesday morning following the Dow’s record close and impressive Nasdaq performance

- Both the S&P 500 and Nasdaq posted gains of 15% and 21% respectively in the second quarter — their strongest showing since 2020

- Federal Reserve Chairman Kevin Warsh is addressing a European Central Bank conference, with traders seeking insights on monetary policy direction

- Thursday’s June employment data release could influence Federal Reserve interest rate decisions

- Crude prices hover near pre-conflict territory despite ongoing concerns about Iran’s Strait of Hormuz threats

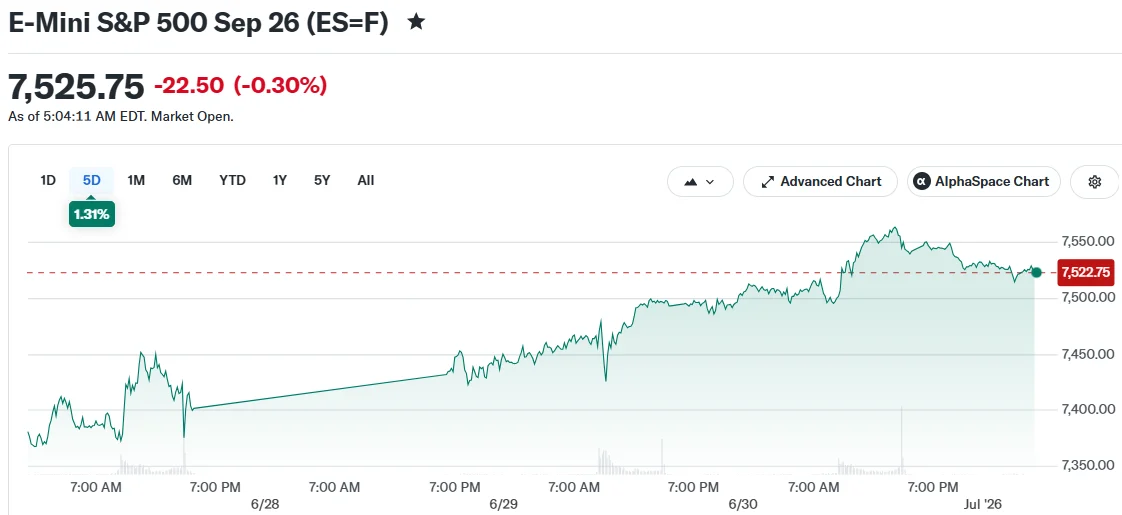

Wall Street futures traded lower Wednesday morning as market participants took profits following an exceptional conclusion to the second quarter. Early trading showed futures contracts for the Dow, S&P 500, and Nasdaq declining by 0.2% to 0.7%.

The previous session delivered a milestone for the Dow Jones Industrial Average, which reached an all-time high. Meanwhile, the S&P 500 capped off its strongest three-month period since 2020 with a 15% surge in Q2. The tech-heavy Nasdaq Composite jumped 21% during the same timeframe, matching its best quarterly performance since 2020. The Dow’s 13% quarterly advance marked its strongest showing since 2022.

Market Focus Turns to Warsh’s Rate Remarks

Federal Reserve Chair Kevin Warsh was scheduled to deliver remarks at the European Central Bank’s yearly gathering in Sintra, Portugal, during Wednesday’s session. Traders are scrutinizing his comments for hints about potential interest rate increases before year-end.

Market observers suggest Warsh is unlikely to soften his restrictive monetary policy stance. According to ING’s Chris Turner, recent consumer sentiment data has exceeded expectations, while US stock markets continue posting strong gains approaching double digits for the year.

The benchmark 10-year Treasury yield was quoted at 4.471%. Meanwhile, the Japanese yen weakened to its lowest level versus the dollar in four decades, partially reflecting anticipation of additional Fed policy tightening.

Thursday brings the release of June’s employment figures. This critical economic indicator will provide market participants with updated labor market conditions and inform projections about potential rate adjustments in coming months.

Middle East Risks and Energy Markets

Oil prices remained anchored around $70 per barrel, approaching levels seen before recent geopolitical conflicts. Washington and Tehran continue diplomatic engagement, though underlying tensions persist.

President Trump has weighed military options but opted to pursue continued negotiations, according to reporting by The Wall Street Journal. Sources indicate Trump has signaled willingness to let discussions extend beyond the August 18 target date for reaching a nuclear agreement.

Iran’s Islamic Revolutionary Guard Corps has issued warnings about potentially shutting down the Strait of Hormuz once more without assurances regarding exclusive authority over the strategic waterway. This ongoing threat maintains vigilance among energy market participants.

Gold retreated beneath the $4,000 per ounce threshold Wednesday as concerns about rising interest rates pressured the precious metal, which generates no yield. The greenback strengthened as market participants increased wagers on Fed policy tightening.

Artificial intelligence and semiconductor equities powered substantial technology sector appreciation during the year’s opening half. Market strategists indicate only the tech segment appears well-positioned to maintain market leadership through the latter half of 2024.

Attention now shifts to Thursday’s employment report as the next critical economic release. Robust job creation numbers could intensify expectations for Fed rate hikes, while softer figures might diminish those concerns.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants