Key Highlights

- All three major index futures—Dow, S&P 500, and Nasdaq—declined Wednesday at the start of Q3 trading

- Federal Reserve Chairman Kevin Warsh delivers remarks at Portugal’s ECB forum; investors parse commentary for monetary policy direction

- Market participants increasingly anticipate Fed rate increases, pushing the 10-year Treasury yield to 4.471%

- Diplomatic efforts in Qatar collapse after Iranian representatives decline engagement with Trump administration officials

- Crude oil prices retreat approximately 1% following failed peace negotiations and renewed Strait of Hormuz concerns

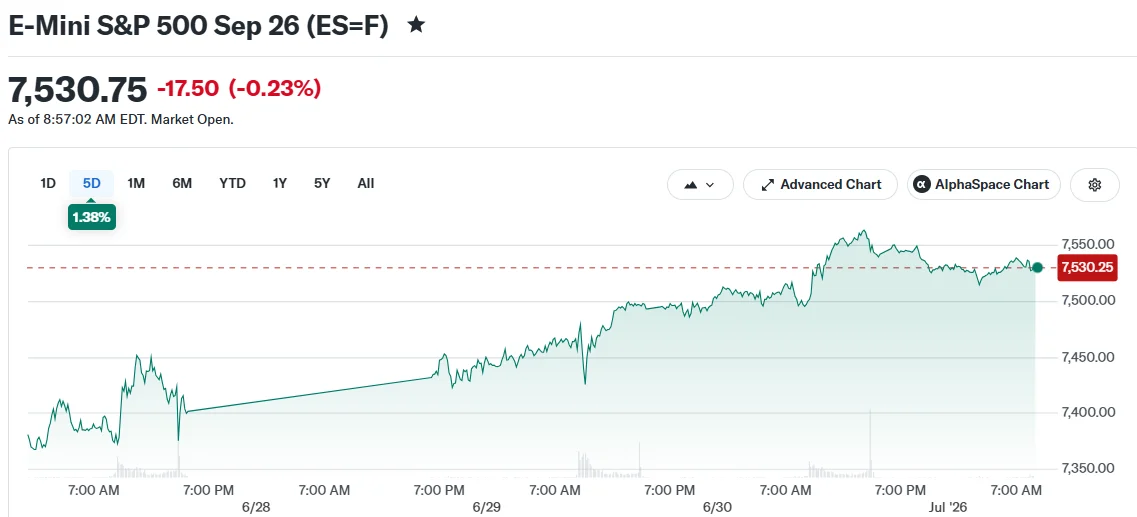

American equity futures declined Wednesday morning, July 1, launching the third quarter with a subdued tone as market participants turned their attention to Federal Reserve Chair Kevin Warsh’s scheduled remarks at a European Central Bank conference in Portugal.

Futures tied to the Dow Jones Industrial Average retreated between 0.2% and 0.3%. Contracts tracking the S&P 500 fell roughly 0.2%, while Nasdaq 100 futures experienced losses approaching 0.5%.

The downturn follows an impressive second-quarter rally. The S&P 500 advanced 15% during Q2, while the Nasdaq surged 21%—marking the strongest quarterly performance for both indices since 2020. The Dow climbed 13%, recording its most robust quarter since 2022.

Investors Parse Warsh Remarks for Interest Rate Direction

Warsh’s presentation at the ECB’s annual monetary policy symposium in Sintra, Portugal was set for 9 a.m. Eastern Time Wednesday. Market observers were keenly analyzing his commentary for insights into future interest rate policy.

Analysts on Wall Street weren’t anticipating explicit forward guidance from Warsh. However, any observations regarding inflation trends or economic conditions could trigger market volatility, particularly as expectations for rate increases intensify.

Chris Turner, an analyst at ING, noted that consumer sentiment has exceeded forecasts and American equities continue trading near recent peak levels. He suggested these conditions make it unlikely Warsh would moderate his more restrictive policy stance.

The 10-year Treasury yield remained stable at 4.471%, essentially unchanged from Tuesday’s close. Meanwhile, the Japanese yen declined to a four-decade low versus the dollar, influenced partially by mounting speculation that the Federal Reserve will implement rate hikes.

ADP’s employment report revealed the private sector added 98,000 positions in June. This data, combined with Challenger’s job reduction figures, was helping frame expectations ahead of Thursday’s official June employment report from the Labor Department.

The government’s jobs data is being published one day earlier than usual due to Friday’s Independence Day holiday. Market participants were simultaneously monitoring manufacturing indicators for additional perspective on American economic momentum.

Middle East Diplomacy Fails, Energy Markets React

Negotiations in Qatar reached an impasse Wednesday after Iran announced its diplomatic representatives would refuse meetings with President Trump’s negotiating team, diminishing prospects for a comprehensive agreement.

Oil prices reversed morning advances and declined roughly 1%. Brent crude futures slipped toward $72 per barrel, while West Texas Intermediate crude fell beneath $69.

Crude had been hovering near $70 per barrel, approximating price levels observed before the escalation of Iranian tensions. Iran’s Islamic Revolutionary Guard Corps previously threatened to again blockade the Strait of Hormuz without security assurances regarding control of the strategic waterway.

According to Wall Street Journal reporting, Trump has indicated to advisers he’s willing to allow negotiations to extend beyond the August 18 deadline established for reaching a nuclear agreement.

Micron and Sandisk were among technology sector stocks experiencing notable premarket losses. Gold retreated below $4,000 per ounce amid concerns about potential rate increases.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants