Key Highlights

- The Dow Jones Industrial Average maintained its position around 52,000 following Monday’s historic milestone close above this threshold.

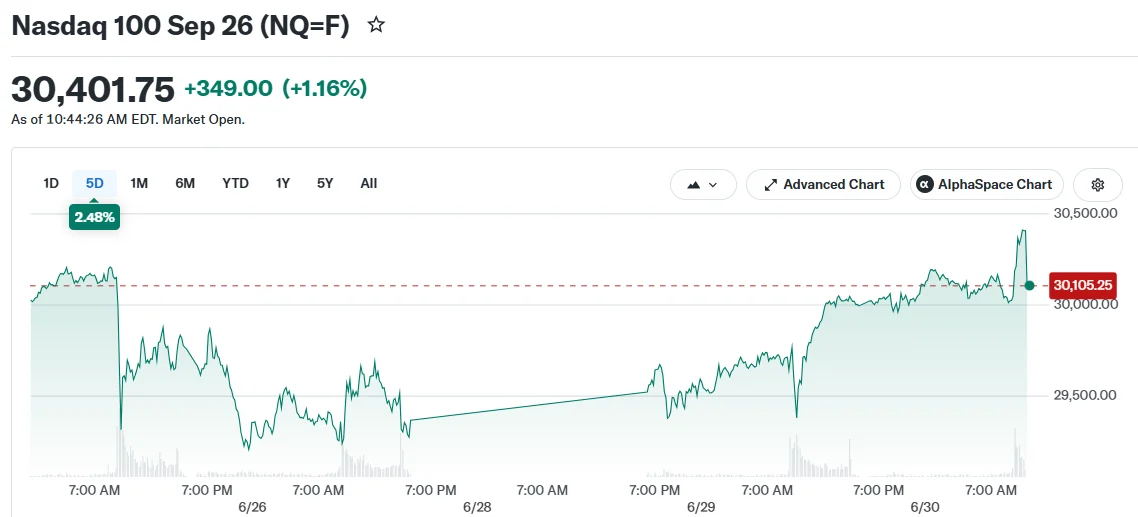

- The Nasdaq Composite led market performance with gains ranging from approximately 1% to 2% during morning trade.

- The S&P 500 advanced between 0.3% and 0.5% as markets concluded the second quarter and the year’s first six months.

- Semiconductor equities have more than doubled in value across the last half-year, driving technology sector strength.

- Crude oil declined as shipping through the Strait of Hormuz normalized more rapidly than anticipated, alleviating supply concerns.

American equity markets advanced on Tuesday as Wall Street concluded the opening half of 2026. The Dow Jones Industrial Average maintained its momentum following the previous session’s breakthrough above the 52,000 threshold. Meanwhile, both the S&P 500 and Nasdaq Composite posted gains.

The Nasdaq emerged as the session’s standout performer. The technology-focused benchmark initially opened flat before rallying as market participants adjusted their holdings in advance of the quarter’s conclusion.

Forces Behind Market Strength

Technology equities have dominated market narratives throughout 2026. Semiconductor manufacturers have experienced exceptional appreciation, with share prices climbing more than 100% during the preceding six-month period.

This semiconductor boom has been instrumental in propelling broader market advancement. Industrial and materials sectors also posted positive movement on Tuesday, contrasting with relative weakness in real estate, healthcare, and consumer staples segments.

Market participants also digested a Supreme Court decision that preserved the Federal Reserve’s operational autonomy for the time being. This ruling eliminated a potential source of market volatility as investors look toward the year’s second half.

Diplomatic developments in the Middle East provided additional support. Scheduled negotiations between American and Iranian officials in Qatar offered hope for reduced geopolitical tensions that had previously pressured financial markets.

Energy Markets And Currency Movements

Oil prices retreated as supply disruption concerns diminished. Maritime traffic through the strategically critical Strait of Hormuz has normalized ahead of forecasts.

This development shifted market sentiment from shortage anxiety toward potential oversupply scenarios. Brent crude futures hovered around $74 per barrel, with West Texas Intermediate trading just above $71. Both benchmarks appeared headed for quarterly losses.

The US dollar continued its ascent relative to foreign currencies. This strength drove the Japanese yen to four-decade lows, increasing the probability of intervention by Japanese monetary authorities.

HSBC analysts indicated that dollar appreciation could accelerate should the Federal Reserve signal potential additional interest rate increases. This perspective introduced a cautionary element to an otherwise optimistic trading session.

Regarding economic indicators, May’s job openings report exceeded forecasts. However, the hiring rate remained subdued.

This contradictory data will likely influence market expectations regarding Federal Reserve monetary policy. Attention now turns to Thursday’s June employment report, which could significantly impact interest rate projections.

On the corporate front, Nike was scheduled to release quarterly earnings Tuesday. The athletic apparel giant continues navigating challenges related to inventory management and consumer demand fluctuations.

As trading progressed, the Dow exchanged hands near 52,300, representing an approximate 0.2% daily increase. The S&P 500 hovered around 7,470, up roughly 0.4%, while the Nasdaq Composite approached 26,034, delivering the session’s most impressive performance among major indices.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants