If you’re looking for an alternative investment strategy outside of the traditional stocks and shares space, then it might be worth considering the merits of a peer-to-peer lending platform. Such platforms allow you to lend cash to third-party borrowers, with interest yields often in the double digits.

With that being said, the likes of PeerBerry claims to generate average returns of 13.7% annually through its peer-to-peer lending structure. The Latvia-based platform also offers a Buyback Guarantee on its loans, which adds a layer of protection on your investment.

If you’re keen to find out more about the investment process, be sure to read our PerryBerry review. We’ll cover everything that you need to know, such as how the platform works, who can invest, how much you can make, what risks you need to consider, and more.

| PeerBerry Visit |

|---|---|

| Product Type | Peer to Peer Lending |

| Potential Return | Average 11.51% Per Year |

| Fees | No Fees |

| Min Investment | € 10 |

| Available to | Worldwide |

What is PeerBerry?

Launched in 2017, PeerBerry is a peer-to-peer lending platform that enables everyday investors to loan out money to third-party borrowers. The platform itself operates much in the same way as any other peer-to-peer site, insofar that you can invest as little as €10.

PeerBerry typically tailors its platform to those located in the European Union, and most of its loans are on a short-term basis. In fact, the vast majority of its loans will have a maturity date of one month or less. This is great for those of you that are looking for an investment avenue without locking your cash up for long periods of time.

The platform was initially backed by lending originator Aventus Group, who was solely responsible for underwriting the loans at PeerBerry. However, the company has since expanded by partnering with a number of other originators. This is beneficial for investors, as it reduces the risks associated with an originator default – which could be detrimental for your Buyback Guarantee.

In terms of the loan structures, you will be lending your cash to the consumer marketplace. Most borrowers are based across Eastern Europe, as well as Kazakhstan and Russia. As the loans typically have a maturity date of less than one month, interest rates charged to the end borrower are usually on par with those of payday loans. This is how PeerBerry is able to offer average yields of 13.7%.

Although most loans are facilitated for the consumer marketplace, PeerBerry recently entered the car loan space. Unlike many of its industry counterparts, the platform does not offer a secondary marketplace. However, this isn’t really needed when you consider the short-term nature of the loans it facilitates.

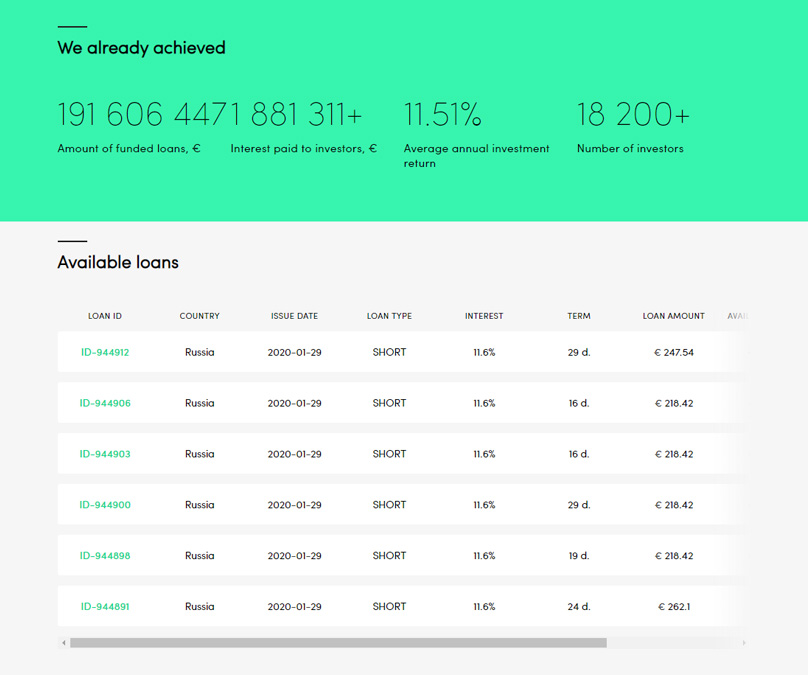

Since the platform was launched in 2017, PeerBerry claims to have funded more than €191 million in loans. This has netted more than 17,200 members returns of €1.5 million+, averaging annual yields of 11.51%.

So now that you have a general overview of what PeerBerry is, let’s take a look at who is eligible to invest.

PeerBerry Eligibility

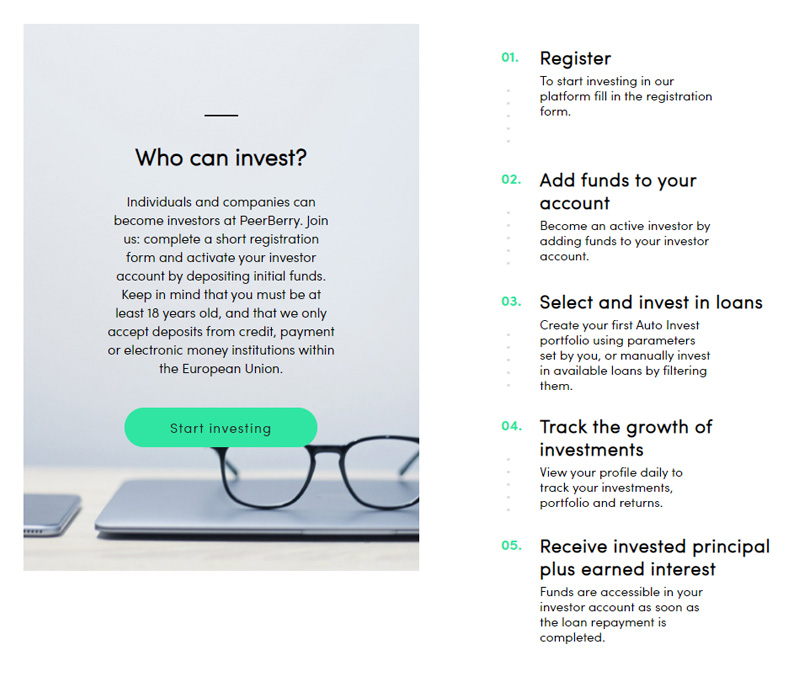

As a Latvia-based entity that seeks to target European investors, PeerBerry requires you to hold a European bank account.

However, this isn’t to say that you won’t be eligible if you’re a non-European investor. On the contrary, as long as you can open a European bank account remotely, you’ll be eligible to invest with PeerBerry.

A number of investors using the platform have noted that opening an EURO-denominated account at TransferWise is sufficient to get started at PeerBerry. You can read our review of Transferwise here.

Regardless of where you are based, you’ll need to ensure that you are aged at least 18 years old, and you have a government-issued ID to verify your identity.

How are Loans Funded?

The underlying investment process at PeerBerry is largely the same as other crowdfunding platforms operating in the space. First and foremost, PeerBerry is not a lender. Instead, it partners with third-party loan originators. These originators deal with the end borrower directly.

This starts at the very offset with the application and due diligence process, meaning that it is the originator’s responsibility to assess the creditworthiness of the borrower. Once the originator has approved a loan, it will then appear on the PeerBerry website. This then allows PeerBerry members to invest in the loan from as little as €10.

Who Will you be Lending Money to?

PeerBerry offers very little information on the end borrowers it facilitates financing for.

Most of the loans are taken out for terms of no more than one month, so it’s safe to say that the originators are involved in payday loan-style arrangements. This means that the end borrower is likely paying an APR significantly higher than the yield offered to PeerBerry members.

Loanees will be based in one of the following countries:

- The Czech Republic

- Denmark

- Kazakhstan

- Lithuania

- Poland

- Russia

- Ukraine

Although you will not know the identity of the person you are lending money to, you will know the amount that they wish to borrow and the country they are based in.

How Much can I Make at PeerBerry?

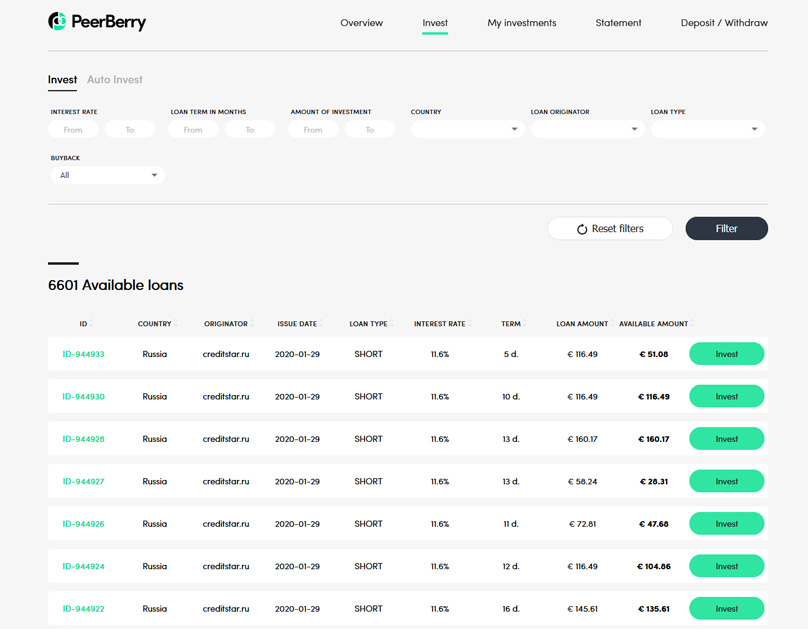

The loans available at PeerBerry typically come with annual yields of between 11% and 25%. If you decide to manually invest on a loan-by-loan basis, you will get to view the yield for each structure.

It goes without saying that the higher the yield, the higher the risk associated with the end borrower. This is determined by the originator underwriting the loan as opposed to PeerBerry itself.

It is important to remember that these yields are based on annual gains, even though the loans available at the platform usually mature within a month. As such, you would be required to continuously reinvest your earnings throughout the year to reach the 11%-25% yields on offer.

When do I Receive my Investment Back?

Most peer-to-peer lending platforms offer longer-term loans, meaning that you would receive a fixed monthly payment from the borrower until the full amount is paid back. However, as PeerBerry facilitates short-term loans, you will only receive a single payment. This will include the principal amount plus the applicable interest.

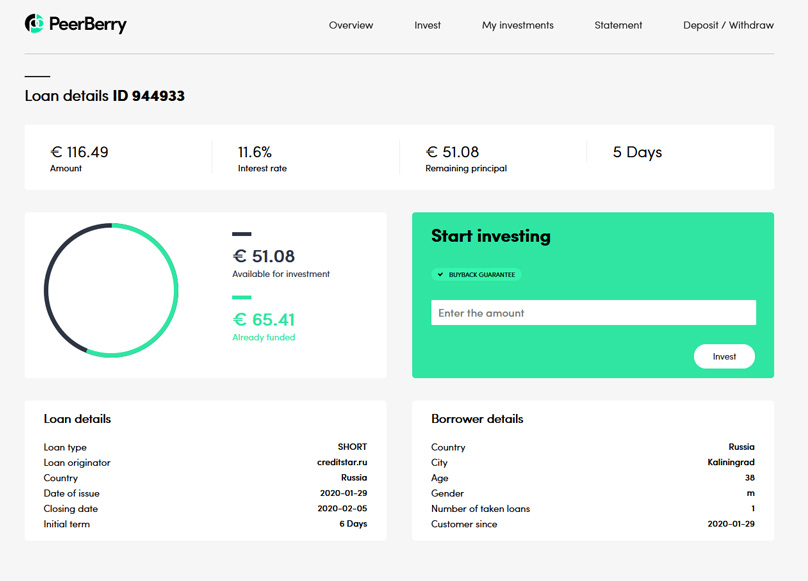

For example, let’s say that you lent out €500 to a borrower in Russia on a 28-day term. The borrower would make a single payment of €550 to the originator 28 days after the funds were distributed. The originator would then forward the funds onto PeerBerry, who it turn would credit your account.

What are the Risks of Investing in PeerBerry?

If you’re a seasoned investor, then you will be fully aware of the ‘risk vs reward’ trade-off. In Layman Terms, the higher the yields on offer, the more risk there is that the borrower will default. This is especially true in the case of PerryBerry, not least because you’ll be making at least double-digits on your investment.

Crucially – and as we have noted throughout our review thus far, PeerBerry loans are essentially payday loans. Such financing agreements are typically facilitated for those that need a small boost of cash, and borrowers often have poor credit.

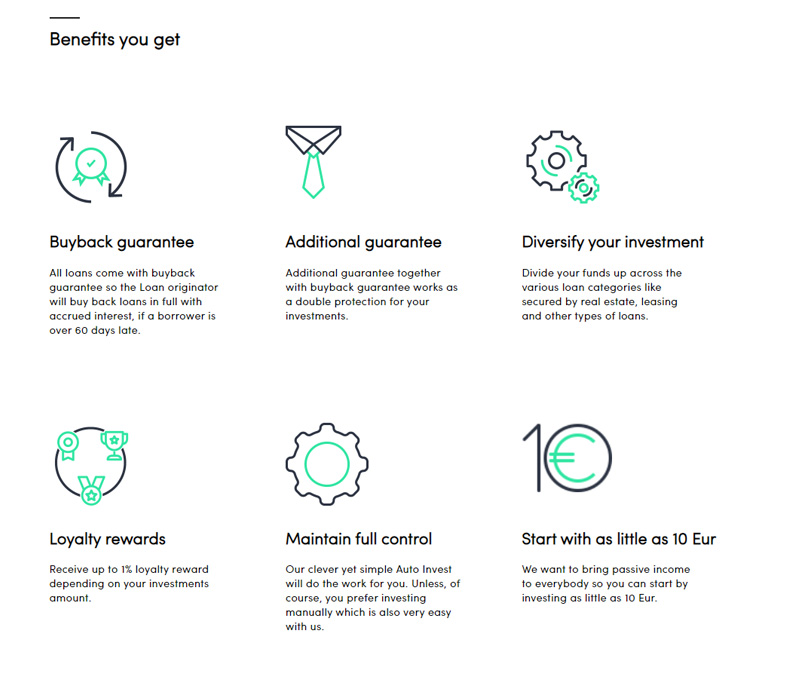

When you factor in the exceptionally high interest rates that come with the loans, there is the very real chance that the end borrower could default on their loan. If this is the case, then the good news is that all PeerBerry loans come with a Buyback Guarantee.

Buyback Guarantee

Buyback Guarantees are becoming more and more popular in the peer-to-peer lending space. They offer investors an element of protection in the event that a borrower defaults on their loan. The Buyback Guarantee is between PeerBerry and the originators that it has partnered with.

As such, were a borrower to default on their payments, the originator would be legally obliged to purchase the loan in full from PeerBerry.

Here’s how it works.

- You lend out €300 to a borrower in Denmark at 15%.

- Although the borrower was supposed to repay the funds 30 days later, no payment has been made. As such, you will not have received any money back in your PeerBerry account.

- The originator behind the loan will personally chase the borrower in an attempt to obtain payment.

- If the borrower has still not settled the loan 60 days after the agreed repayment date, the Buyback Guarantee will kick-in.

- This means that the originator will forward the €300 + interest to PeerBerry as per the guarantee.

- Your PeerBerry account will then be funded with the full principal amount plus the agreed interest of 15%.

As you will see from the above example, the only loss that you would have made as per the Buyback Guarantee was an opportunity cost. In other words, by having to wait an additional 60 days to receive your money back, you were not able to reinvest the cash into other opportunities.

What if the Originator Defaults?

The above example illustrates just how effective the Buyback Guarantee can be in the event a borrower defaults on payment. However, it is crucial to note that the Buyback Guarantee is not 100% fool-proof. Don’t forget, the guarantee is between the originator and PeerBerry, with the originator subsequently treating the default as a bad debt if they are not able to recover the funds.

As a result, there is always the possibility that the originator runs into financial difficulties, which could put the Buyback Guarantee into jeopardy. After all, if the originator doesn’t have the cash to purchase the default from PeerBerry, who will?

Whether or not PeerBerry would have the required finances to cover the bad debt itself remains to be seen. Some peer-to-peer platforms carry an additional reserve pot, which is in place to cover the event of an originator default. However, we were unable to find any information as to whether or not such a pot exists at PeerBerry.

Auto-Invest or Manual Investing?

As it the case with a lot of crowdfunding platforms, you will have the option of choosing your own investments, or opting for the auto-invest feature.

If you’re the type of investor that likes to take a hands-on approach, then you might prefer to manually browse through the many loans listed. This will allow you to view key metrics on the loan, such as where the borrower is based, how much they seek to borrow, and how much interest you’ll earn.

However, most of the loans at PeerBerry are much the same, so you won’t have a substantial amount of data to go by. As such, you might be best to stick with the auto-invest option.

In doing so, you simply need to specify how much you want to invest, and then PeerBerry will take care of the rest. The platform will diversity as much as possible, with auto-invest plans consisting of loans from multiple countries and various risk scores. This is how you will meet the platform’s target annual yield of 13.7%.

Diversifying at PeerBerry

Regardless of what asset class you are choosing to invest in, it is important to diversify your holdings as best as possible. This will allow you to mitigate your exposure to a single investment that goes wrong. In the case of PeerBerry, it would be wise to diversify your portfolio with as many loans as possible.

This can be achieved with ease at the platform, as you can invest from just €10 per agreement. For example, let’s say that you have €1,000 to invest. Instead of injecting the entire €1,000 into a single loan structure, you would be best advised to purchase 100 individual loans at €10 each.

In doing so, a single default would have little impact on you. In fact, when you consider the size of the yields on offer, a small number of defaults would still leave you with a good amount of profit.

Most importantly, even if a number of borrowers did default on their loan, you would still be covered by the Buyback Guarantee. With that being said, your diversification strategy should include as many originators as possible. This will mitigate the risks of being over-exposed to an originator default.

Secondary Marketplace

PeerBerry does not offer a secondary marketplace, meaning that you’ll need to hold onto your loan structures until they are repaid by the borrower. However, it wouldn’t make sense for a secondary marketplace to exist anyway, not least because the loans at PeerBerry rarely exceed 30 days.

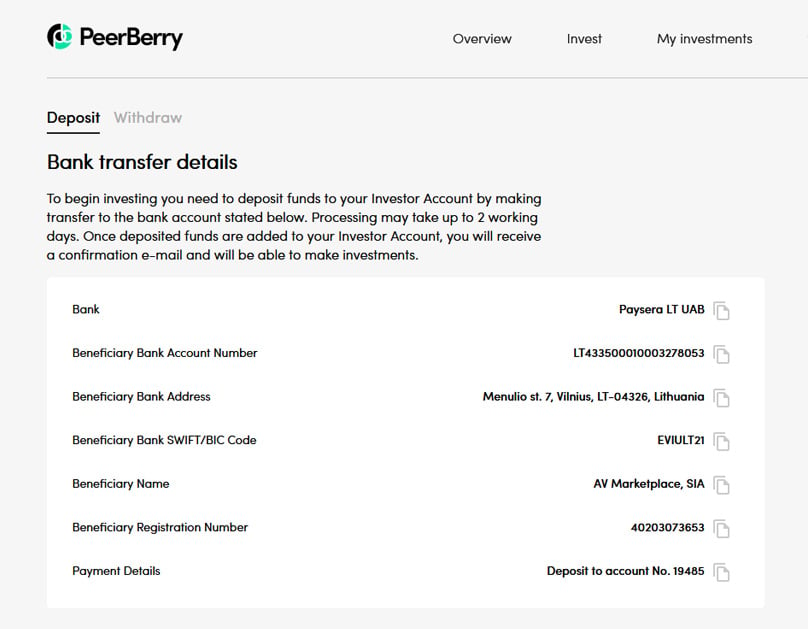

Depositing and Withdrawing Funds

The only payment method supported by PeerBerry is a bank transfer. The funds must come from a European Union bank account, and the transfer needs to be facilitated through SEPA. As noted earlier, non-European investors have the option of opening an EUR-denominated account with TransferWise, which is perfectly fine for making PeerBerry deposits.

To clarify, the only currency that you can fund your account with is Euros. When it comes to withdrawals, you will need to cash your funds back to the same bank account that you used to make a deposit.

If you do need to withdraw your earnings to a new bank account, you will first need to make a small deposit from the account. This is to verify that you are the true owner of the account, and the deposit can be as little as €0.01.

Before your first deposit is authorized, you will need to verify your identity. This is to ensure that PeerBerry remains compliant with European regulations on the countering of money laundering. To do this, you’ll need to upload a copy of your government-issued ID, which the verification team at PeerBerry will need to validate.

You can only withdraw funds that are available in your account, meaning that money locked into a loan agreement will remain unavailable until the borrower makes their payment.

Does PeerBerry Charge any Fees?

PeerBerry does not charge its investors any fees. You can deposit and withdraw funds for free, and there are no investment or maintenance charges to worry about. The platform instead makes its money from the originators that it has partnered with.

Customer Service at PeerBerry

The customer support team at PeerBerry works 7 days per week, between the hours of 08.00-17:00 (GMT+3). The easiest way to make contact is via the live chat facility. Alternatively, you can call the team directly on +370 61 355 529.

If you need to make contact outside of customer support opening hours, you can email the team at info@peerberry.com.

PeerBerry Review: The Verdict?

In summary, there is much to like about PeerBerry. The peer-to-peer lending platform offers a straightforward way to lend your money out to third-party borrowers. Loans are facilitated on a short-term basis, with agreements rarely surpassing 30 days. This is great if you don’t want to lock your investment up for long periods of time.

When it comes to annual yields, PeerBerry loans typically pay between 11% and 25%.

However, by engaging in a diversified plan via the auto-invest option, PeerBerry aims for 13.7% annually. This is much higher than traditional investment vehicles pay, albeit, as are the risks.

On the one hand, these risks are countered by the platform’s Buyback Guarantee. This means that you’ll still be paid out if the borrower defaults on the loan – including that of the interest. However, if the originator themselves runs into financial problems, the Buyback Guarantee could be of little use.

The platform itself is one of the best we have reviewed so far – its very clean and well organized and very easy to use. If you are new to these types of platforms you should have no trouble at all getting started.

The auto-invest tool is excellent and allows you to create any number of portfolios based on different criteria.

Overall, we recommend you take a look at Peerberry, its a great P2P loan platform.

PeerBerry

Pros

- Excellent Platform

- Buyback Guarantee

- Great Returns on Offer

- Great Auto Invest Tool

- Easy to Diversify

Cons

- Slightly Lower Returns than Competitors

- More risk than traditional finance products

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants