Stock: Price Target Raised to $225 as $100B OpenAI Deal Divides Wall Street")

TLDR

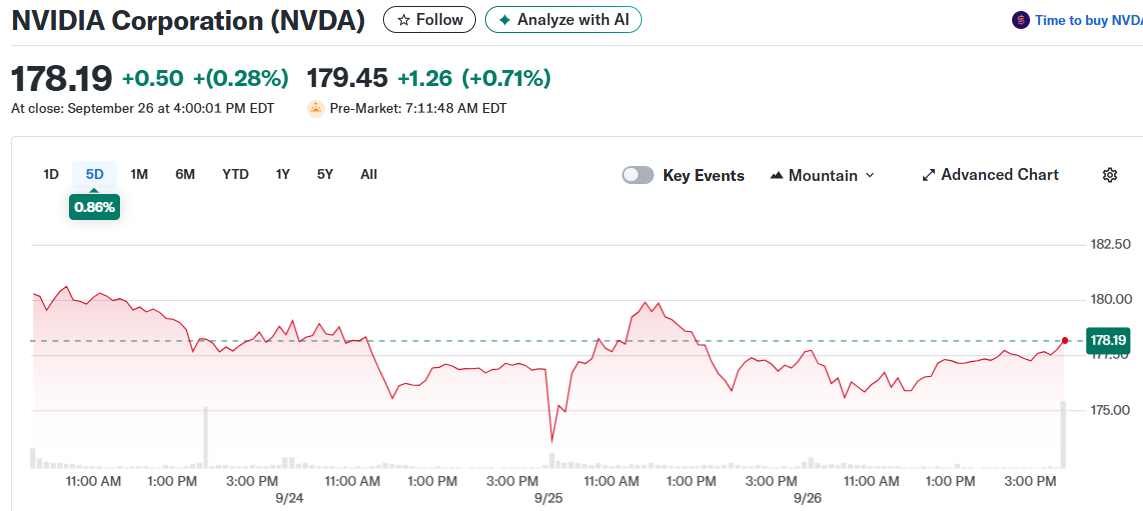

- Nvidia stock is trading at $178.67, up 0.6% and near its all-time high of $184.55, with strong technical momentum over the past three months

- Evercore raised its price target to $225 after talks with Nvidia’s CFO, highlighting underestimated AI demand and NVLink’s strategic importance

- The company signed a $100 billion deal with OpenAI to deploy 10 gigawats of AI computing power, though Wall Street remains split on execution risks

- Nvidia expects global data center spending to grow from $600 billion this year to $3-4 trillion by 2030

- Trading at 41x forward earnings, the stock appears reasonably valued given expected 40-50% quarterly revenue growth rates

Nvidia stock continues its climb near record highs as analysts weigh massive infrastructure investments against execution challenges. The semiconductor giant trades at $178.67, marking a 0.6% gain and maintaining its position just below the all-time high of $184.55.

The stock has surged roughly 22% over the past three months. Technical indicators show strong momentum with the Relative Strength Index approaching 68, nearing overbought territory but still indicating bullish sentiment.

Evercore analyst Mark Lipacis raised his price target from $214 to $225 following direct discussions with Nvidia’s CFO. The analyst emphasized Nvidia’s position as not just a hardware leader but the “AI ecosystem of choice” due to its CUDA software stack and proprietary NVLink connectivity technology.

Lipacis believes NVLink is on track to become an industry standard. This could help Nvidia secure long-term infrastructure contracts with major partners like OpenAI.

The analyst increased his 2026 revenue and earnings estimates by 2%. He noted these projections may prove conservative if AI demand accelerates beyond current expectations.

Wall Street Split on $100B Infrastructure Push

The $100 billion OpenAI collaboration has created a divide among Wall Street analysts. Some view it as cementing Nvidia’s AI infrastructure dominance while others worry about execution risks and potential overreach.

The deal includes a commitment for at least 10 gigawatts of AI infrastructure. Nvidia’s management suggests the addressable market per gigawatt could range from $30 billion to $40 billion.

This implies a multi-trillion-dollar opportunity if fully realized. However, some analysts remain cautious about the complexity of executing such a massive deployment.

A key insight from company commentary is that OpenAI may have underestimated its compute needs. The AI company is now racing to scale capacity before it becomes a bottleneck to its operations.

Barclays also raised its price target to $240, citing strong demand for AI hardware and dominant GPU market share. The firm expects Nvidia’s upcoming B100 chip to drive the next growth wave.

Data Center Spending Expected to Explode

Nvidia management forecasts total data center capital expenditures reaching $600 billion this year. By 2030, the company expects global data center buildouts to reach $3 trillion to $4 trillion.

Currently, only the U.S. and China are heavily investing in AI technology. Europe is just beginning to embrace the AI trend, representing another potential market for Nvidia’s graphics processing units.

Data centers take years to build, creating a predictable pipeline for Nvidia. Companies announcing data center projects this year will need computing units when facilities become operational in future years.

Nvidia has secured additional partnerships to strengthen its market position. CoreWeave placed a $6.3 billion order for Nvidia GPUs to increase its computing capacity.

The company also announced a $5 billion investment in Intel. This partnership will allow Nvidia to design and build CPUs that better control its GPUs, expanding its ecosystem dominance.

Trading at 41 times forward earnings, Nvidia’s valuation appears reasonable given its expected growth trajectory. The company maintains profit margins above 52% and return on equity over 90%.

Nvidia expects to maintain 40% to 50% quarterly revenue growth over the next few years. This growth rate makes the current valuation look attractive from a five-year perspective.

Support levels for the stock sit in the $150-$160 range, coinciding with the 50-day moving average. Resistance remains at the $184-185 zone, where the stock has struggled on previous attempts.

The company’s debt-to-equity ratio under 0.15 demonstrates strong balance sheet management. These metrics highlight Nvidia’s exceptional capital efficiency and ability to scale revenue with minimal financial strain.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants