TLDR

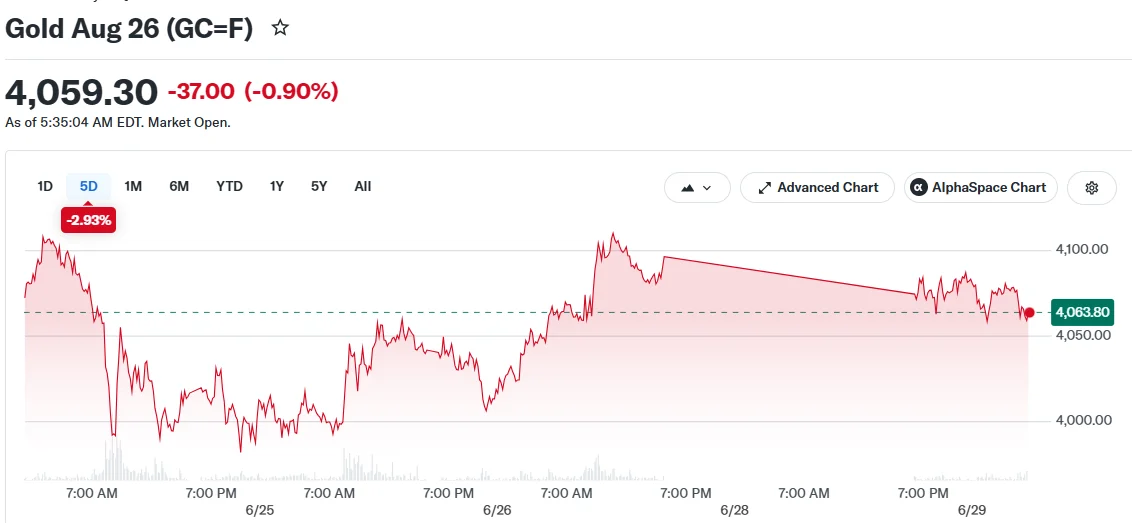

- Gold declined more than 1% on Monday, approaching $4,000 per ounce following renewed military confrontations between the US and Iran in the Persian Gulf

- A ceasefire agreement has been reached, with diplomatic discussions scheduled in Doha for Tuesday

- The precious metal has declined approximately 23% since coordinated US-Israeli military operations against Iran began in late February

- Financial markets now indicate over 30% probability of a Federal Reserve interest rate increase before 2026 ends

- Critical economic indicators releasing this week, particularly employment figures, may shape Fed monetary policy direction

Renewed military confrontations between the United States and Iran during the weekend pushed gold prices lower on Monday, driving the precious metal toward the $4,000 threshold as investors returned their focus to inflationary pressures.

Spot gold decreased 1.1% to settle at $4,043.62 per ounce during early Asian trading sessions. Futures contracts for gold declined 1% to reach $4,056.77.

Military operations between the United States and Iran resumed in the Persian Gulf during the weekend, disrupting a temporary ceasefire that had provided relief to energy markets recently. A vessel transporting Qatari crude oil sustained damage during these exchanges, creating obstacles for shipping operations through the strategically vital Strait of Hormuz.

Notwithstanding the escalating tensions, both nations have committed to cease hostilities. According to Axios, citing anonymous US government sources, representatives from both countries will convene in Doha on Tuesday for negotiations.

Elevated Interest Rates and Dollar Strength Weigh on Gold

Gold has experienced sustained downward momentum over recent months. The metal has depreciated roughly 23% since combined US and Israeli military strikes against Iranian targets commenced in late February.

Escalating energy costs stemming from the regional conflict have amplified inflationary pressures, strengthening market expectations that central banks will maintain elevated interest rates for an extended period. This dynamic has particularly impacted gold, which generates no income or dividend yields for investors.

Current market pricing reflects greater than 30% probability that the Federal Reserve will implement a rate increase before the conclusion of 2026, based on CME Fedwatch tool analytics.

Additional headwinds have emerged from US dollar strength and elevated Treasury bond yields. The Federal Reserve’s June policy meeting conveyed a restrictive monetary stance, while recent inflation data, though aligned with analyst projections, registered at elevated levels.

The Fed’s preferred inflation metric, the personal consumption expenditures price index, advanced 0.4% during May. Treasury yields experienced modest declines following the release of that measurement.

Other precious metals similarly retreated Monday. Silver tumbled 1.8% to $58.11 per ounce. Platinum decreased 0.4% to $1,612.20.

Employment Report Could Dominate Market Sentiment This Week

Market participants are closely monitoring multiple economic releases this week for insights into future monetary policy trajectory.

Japanese industrial output figures, Chinese purchasing managers index data, and European inflation statistics are all scheduled for publication.

However, the primary focus remains the US nonfarm payrolls report covering June activity. Robust labor market performance would provide the Federal Reserve additional justification for raising interest rates.

Evidence of continued hiring momentum could apply additional downward pressure on gold valuations, as elevated rates amplify the opportunity cost of maintaining non-income-generating assets such as precious metals.

The ceasefire negotiations scheduled for Tuesday in Doha will also attract significant market attention. A durable peace agreement could alleviate energy price pressures and moderate inflation expectations, fundamentally altering the outlook for gold markets.

Currently, the precious metal remains constrained near multi-month lows, navigating between geopolitical volatility and expectations of rising borrowing costs.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants