Key Highlights

- Spot gold surged 1.4% on Friday, marking its first weekly advance since the final week of May

- Disappointing U.S. employment figures (57,000 jobs created in June) lowered Federal Reserve rate increase probabilities

- Market expectations for a September rate hike dropped to 53.5%, compared to 65% prior to the employment release

- Other precious metals including silver, platinum, and palladium experienced significant Friday gains

- Despite Friday’s rally, gold remains approximately 22% below its January record of $5,300 per ounce

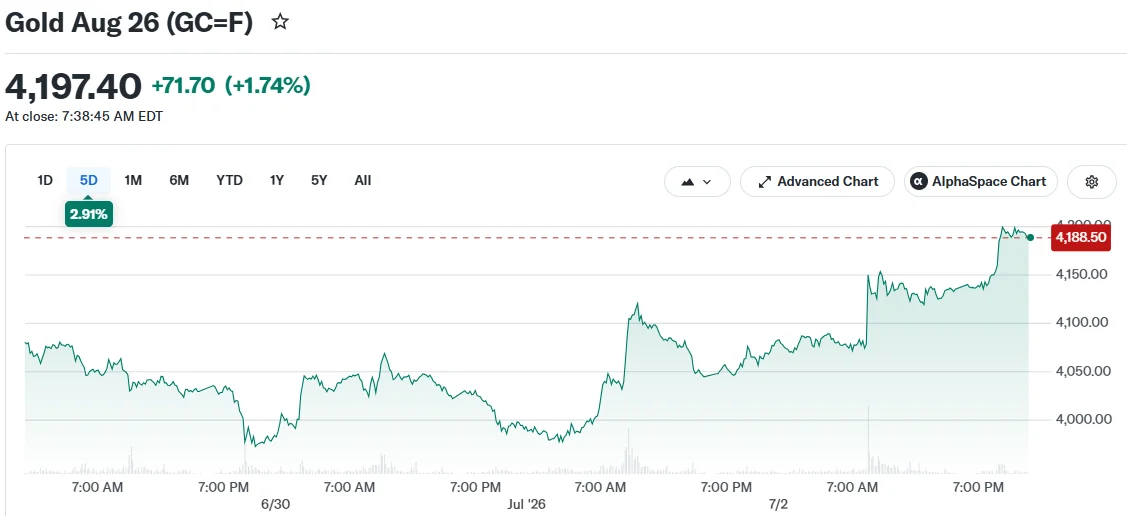

The precious metal experienced a notable rally on Friday, positioning itself for its first weekly gain after four consecutive weeks of losses. Spot gold reached approximately $4,182 per ounce, registering a 1.4% daily increase and approximately 2.3% weekly advance.

The upward momentum followed Thursday’s release of U.S. nonfarm payrolls figures, which revealed the American economy generated only 57,000 positions in June. This figure significantly underperformed the anticipated 115,000 estimate and fell short of May’s downwardly adjusted 129,000 additions.

The disappointing employment data diminished concerns that the Federal Reserve would maintain its aggressive interest rate policy. Robust labor market conditions represent one of the central bank’s primary justifications for monetary tightening.

Prior to the employment release, financial markets assigned approximately a 65% probability to a September rate increase. Following the data publication, this likelihood declined to 53.5%, based on CME’s FedWatch tool calculations.

Factors Behind Gold’s Recent Struggles

Gold has endured a challenging year. The yellow metal recorded its most severe quarterly decline in 13 years during the three-month period ending in June, dropping approximately 13% throughout that timeframe.

A strengthening U.S. dollar, mounting inflation worries, and aggressive rhetoric from the Federal Reserve have collectively pressured valuations. The escalation of the U.S.-Iran conflict in February additionally disrupted markets and raised questions about gold’s traditional safe-haven characteristics.

Gold currently trades roughly 22% beneath its record high exceeding $5,300 achieved in January 2026.

The U.S. Dollar Index retreated from nearly 13-month peaks following Thursday’s employment data, providing support for gold and related metals.

Broader Precious Metals Rally

Silver demonstrated particularly impressive performance. Spot silver climbed approximately 2.9% to $62.77 per ounce, establishing a trajectory for a weekly increase of roughly 6.7%.

Spot platinum advanced 2.8% to $1,660.10 per ounce. Palladium registered approximately 1% gains at $1,280.09.

Both gold and silver achieved exceptional performance throughout 2025, advancing 66% and 135% respectively. This year has seen gold decline 3% while silver has fallen 12%.

OCBC analysts characterized their outlook as “cautiously constructive” on gold following the payrolls release.

They indicated the weaker employment figures help diminish the likelihood of additional aggressive Federal Reserve measures. Nevertheless, they emphasized that with unemployment remaining stable and inflation concerns persisting, prudence remains warranted.

OCBC stated a more sustainable gold recovery would necessitate declining real yields, stabilizing investor appetite, and a more accommodative Federal Reserve stance.

The financial institution had revised its gold and silver price projections downward earlier in the week, attributing the adjustment to ongoing pressure from U.S. rate expectations and elevated yields.

Trading activity remained subdued on Friday preceding a U.S. market closure.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants