Key Highlights

- Natural gas prices in Europe increased on Tuesday but remain poised for their first quarterly reduction in six quarters.

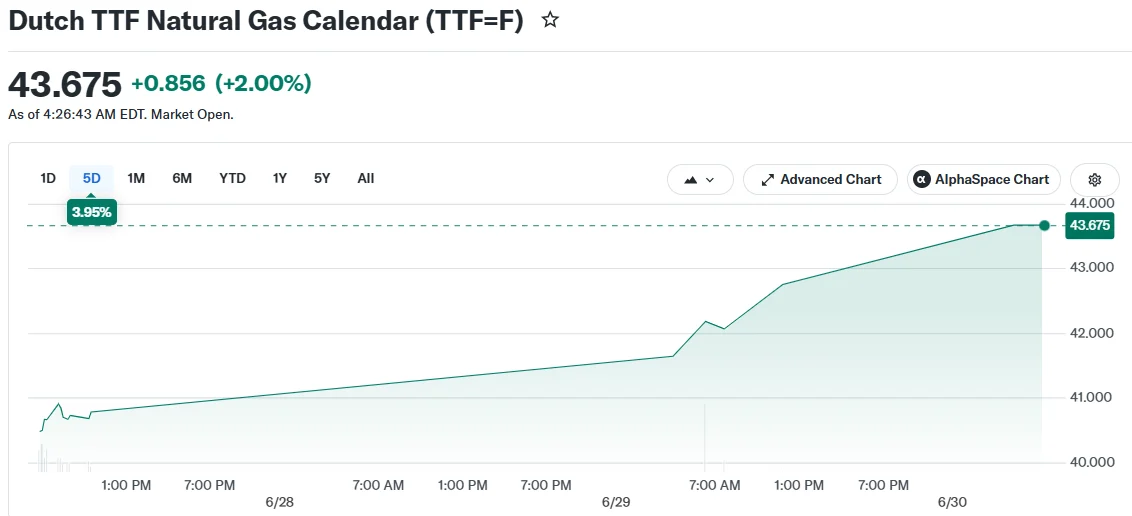

- The benchmark Dutch TTF contract advanced 2% to reach 43.44 euros per megawatt-hour while maintaining its quarterly downward trajectory.

- De-escalation between the United States and Iran restored normal maritime operations in the Strait of Hormuz, alleviating supply disruptions.

- Storage facilities across Europe stand at approximately 48% of total capacity, significantly beneath previous year levels and historical averages.

- European authorities maintain that present storage volumes pose no immediate risk to winter energy security requirements.

Wholesale natural gas markets across Europe experienced upward movement on Tuesday. Nevertheless, the broader trend indicates the continent is approaching its first quarterly price reduction in more than twelve months.

The Dutch TTF futures contract for nearest delivery, which serves as Europe’s primary pricing benchmark, increased by 2% to settle at 43.44 euros per megawatt-hour. This positions the market for its initial quarterly decrease across six consecutive quarters.

Meanwhile, the United Kingdom’s wholesale natural gas contract similarly rose 2%, climbing to 104.57 pence per therm. British markets are tracking toward their first quarterly contraction in five consecutive quarters.

Factors Behind Market Volatility

Energy markets experienced significant turbulence earlier this year amid military tensions involving Iranian forces. The confrontation generated substantial concern regarding critical energy transportation corridors throughout the Middle Eastern region.

Maritime attacks occurred last week, temporarily disrupting vessel movements through the strategically vital Strait of Hormuz. American and Iranian representatives are scheduled to convene in Doha today for diplomatic negotiations.

The Strait of Hormuz serves as a conduit for approximately 20% of global liquefied natural gas exports. Any interruption to this passage typically drives upward pressure on international gas valuations.

A diplomatic ceasefire established earlier this month enabled shipping operations to return to regular patterns. LNG cargo shipments originating from Qatar and the United Arab Emirates that experienced delays have now resumed their journey toward global destinations.

International crude oil prices have likewise retreated to pre-conflict valuations. This development eliminated a key factor that had been sustaining elevated European natural gas and power prices.

Storage Capacity Concerns Persist

Despite the general price downturn, market participants indicate that inadequate storage inventories may prevent substantial further declines. European storage infrastructure currently holds just below 48% of maximum capacity.

This represents a decrease from the 56.2% level recorded during the comparable timeframe last year. The figure also trails the five-year average injection benchmark of 61%.

According to a Financial Times analysis referencing Wood Mackenzie data, European Union storage facilities may conclude the refilling period at approximately 76% capacity. This would represent the lowest peak storage achievement since no later than 2011.

The deficit originates from the Iranian conflict, which obstructed LNG cargo movements through the Strait of Hormuz. Diminished output from Qatari and Emirati production facilities contributed additional strain.

European storage locations began the injection period with merely 28% capacity utilization. Current average levels throughout the continent hover near 48%.

The European Commission announced Sunday that existing storage volumes do not constitute an urgent threat to energy supply stability. Officials emphasized that achieving 80% storage capacity proves adequate to satisfy winter consumption requirements.

A commission representative stated that storage stands approximately 10% beneath pre-crisis historical norms. The official further noted that natural gas consumption throughout the European Union has declined roughly 17%.

The commission has advised member nations to target storage levels between 75% and 80% as a minimum threshold. In previous years, the non-mandatory objective had been established at 90%.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants