Key Highlights

- The US dollar index experienced its second consecutive weekly decline, driven by yen strength

- Japan’s Finance Minister announced plans for the Government Pension Investment Fund to increase domestic asset allocation

- Japanese producer price data exceeded expectations, reinforcing the case for additional Bank of Japan interest rate adjustments

- Military tensions between the US and Iran generated conflicting market signals — strengthening the dollar’s safe-haven appeal while declining oil prices eased inflation concerns

- Precious metals gained momentum, with China’s central bank extending its gold accumulation streak

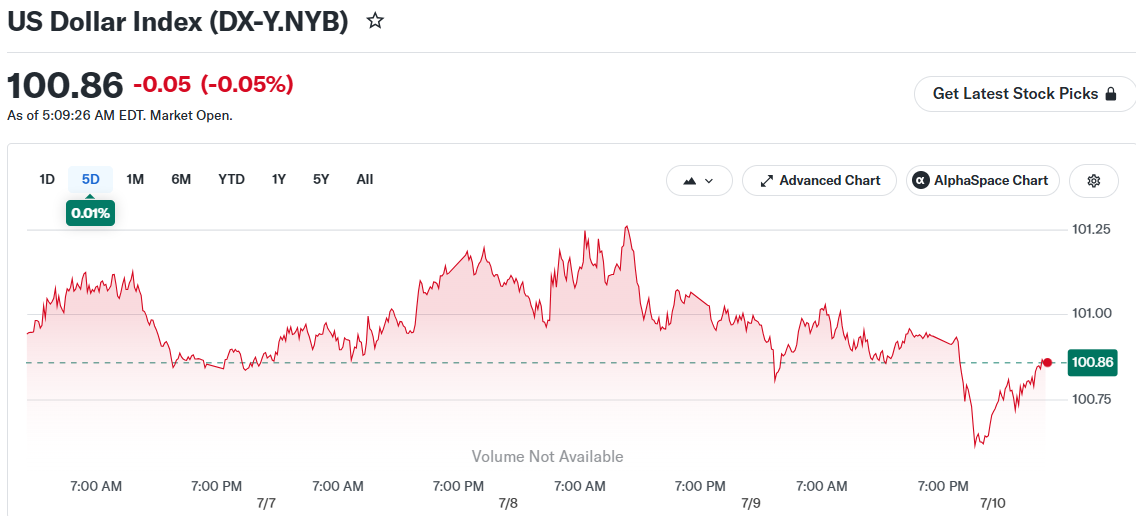

The US dollar retreated on Friday, pressured by significant strength in the Japanese yen. The dollar index decreased by 0.1%, recording a second straight week of losses.

Finance Minister Satsuki Katayama of Japan announced that the government seeks to redirect more capital from its Government Pension Investment Fund toward domestic investments. As the largest pension fund globally, any reallocation from this institution typically generates substantial market movements.

The yen experienced immediate gains following this announcement. The dollar-yen exchange rate fell 0.6% to reach 161.44. Japanese 10-year government bond yields declined 3.4% in response to the news.

Additionally, Japan released producer price index figures for June that surpassed forecasts, marking the strongest expansion in more than three years. Rising producer costs typically translate into higher consumer inflation, potentially compelling the Bank of Japan to implement further interest rate increases.

Although the yen strengthened on Friday, it continues trading near 40-year lows. Japanese officials have previously intervened in currency markets when the yen reached comparable levels, and market observers suggest intervention remains a significant possibility.

Middle East Tensions and Economic Data Create Mixed Market Dynamics

Escalating US-Iran tensions contributed to currency market volatility throughout the week. US military forces conducted strikes against approximately 90 Iranian targets on Thursday, prompting Iran to launch drone and missile counterattacks targeting US military installations in Bahrain, Kuwait, and Qatar.

President Trump declared an end to ceasefire efforts early in the week, though he subsequently suggested Iran had initiated communication regarding additional negotiations.

The escalation initially bolstered the dollar’s safe-haven status. However, crude oil prices declined 2% on Thursday, alleviating inflation concerns and diminishing pressure on the Federal Reserve to implement rate hikes.

June Federal Reserve meeting minutes revealed division among policymakers regarding potential rate increases this year. Disappointing employment figures from the prior week had already diminished rate hike expectations. Current market pricing indicates only a 24% probability of a rate increase at the upcoming July 28-29 Federal Reserve meeting.

Weekly jobless claims decreased by 2,000 to reach a six-week low of 215,000, indicating continued labor market resilience. Conversely, existing home sales fell 2.4% in June to 4.09 million units, falling short of analyst projections.

Most major currencies appreciated against the dollar. Both the euro and British pound advanced approximately 0.1%. The Chinese yuan strengthened 0.2% following inflation data demonstrating sustained economic momentum. The Australian dollar climbed 0.3%.

The South Korean won bucked the trend, weakening 0.3% amid domestic equity market turbulence. South Korea recently implemented 24-hour trading for the won-dollar currency pair.

Gold advanced 1.43% to finish the session higher, while silver surged 3.77%. Both precious metals benefited from dollar weakness, declining bond yields, and heightened Middle East geopolitical risks. China’s central bank expanded its gold reserves by 320,000 ounces in May, representing its largest monthly acquisition in 17 months and marking the 19th consecutive month of additions.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants