TLDR

- Institutional investors dumped technology hardware and semiconductor positions for the fourth consecutive week, Goldman Sachs data shows

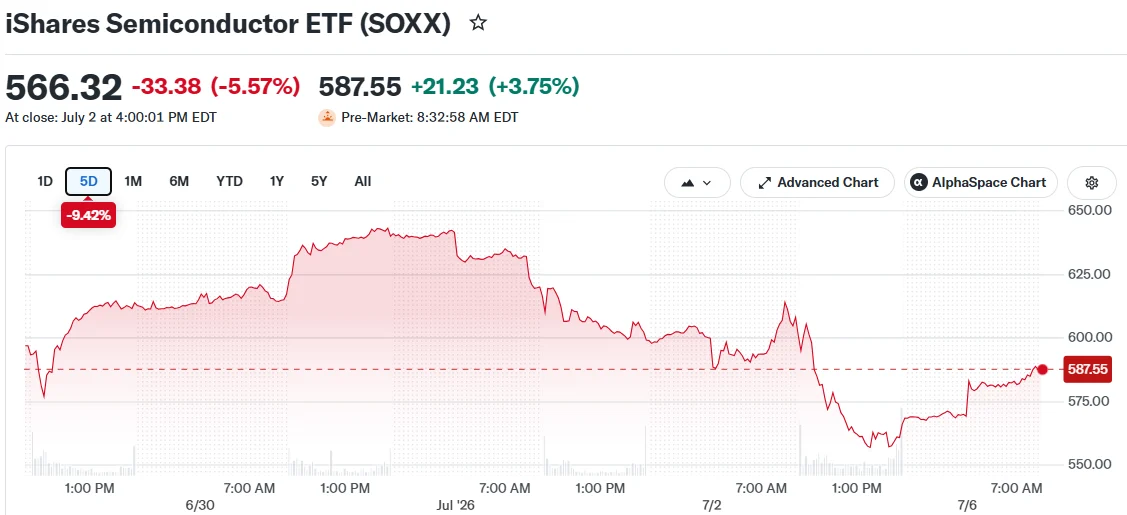

- Semiconductor benchmark SOX index declined 4.2% during the week concluded July 3

- Foxconn’s Q2 revenue exceeded analyst projections, reinforcing confidence in AI infrastructure demand

- Samsung Electronics anticipated to deliver 18-fold year-over-year profit surge in results due Tuesday

- Nasdaq 100 futures rallied 1% Monday morning as technology sector showed signs of stabilization

Institutional investors in the United States continued liquidating positions in technology hardware and semiconductor equities for a fourth straight week, according to Goldman Sachs client communications distributed Friday. This sustained divestment arrives as major chip manufacturers prepare to unveil quarterly financial results.

The Philadelphia Semiconductor Index (SOX) registered a 4.2% decline throughout the week concluded July 3. This downturn signals mounting investor apprehension regarding artificial intelligence capital expenditure velocity and timeline for return on these substantial investments.

According to Goldman Sachs analysis, information technology — encompassing semiconductors and hardware manufacturers — represented the most heavily net-sold American equity sector for four consecutive weeks. Hedge fund managers simultaneously divested industrial and consumer discretionary holdings throughout this timeframe.

Institutional selling exceeded buying activity for three consecutive weeks. The predominant portion of last week’s liquidation focused on individual U.S. equities rather than diversified index instruments.

While reducing technology exposure, hedge fund managers reallocated capital toward alternative sectors. They accumulated positions in commercial services, consumer staples, real estate, and energy companies. Additionally, they purchased index-tracking and exchange-traded fund products that correlate with broader market movements.

Technology Futures Rebound Monday Morning

Notwithstanding recent institutional selling pressure, U.S. equity futures advanced Monday. Nasdaq 100 futures surged 1%, while S&P 500 futures increased 0.4%. Dow Jones Industrial Average futures remained relatively flat following the blue-chip benchmark’s record-breaking holiday-abbreviated trading week.

The recovery materialized after Foxconn, a critical supplier to Nvidia, announced quarterly revenue Sunday that surpassed analyst expectations. These results indicated sustained appetite for AI infrastructure components, alleviating some downward pressure on semiconductor valuations.

Samsung Quarterly Results Take Center Stage

Market focus now shifts to Samsung Electronics, scheduled to release quarterly performance metrics Tuesday. The world’s dominant memory chip producer is projected to report an 18-fold profit multiplication versus the corresponding period last year, substantially exceeding its complete 2025 fiscal year total.

JPMorgan strategists elevated their S&P 500 price target, projecting the AI supercycle will propel the benchmark higher. They cautioned, nevertheless, that volatility should be anticipated along this trajectory.

Regarding macroeconomic developments, market participants are monitoring U.S. services sector data published Monday. A disappointing June employment report has already recalibrated interest rate expectations. Federal Reserve meeting transcripts, the inaugural release under new chair Kevin Warsh, are scheduled for Wednesday dissemination.

Baird investment strategist Ross Mayfield told Yahoo Finance the market remains in a bull run. “It’s a bull market driven by earnings and liquidity,” he said, adding he expects gains to continue into 2027.

While hedge funds may be crystallizing gains or hedging against potential semiconductor sector weakness, Monday’s futures performance indicates certain investors perceive the recent price correction as an attractive entry point.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants