Key Takeaways

- Both the STOXX 600 and DAX reached unprecedented peaks on Friday, with the STOXX 600 posting its strongest weekly advance in more than four weeks

- Disappointing US employment figures reduced anticipation of an imminent Federal Reserve interest rate increase

- Christine Lagarde, President of the ECB, indicated that inflation and growth uncertainties are achieving better equilibrium, reducing expectations for additional rate increases

- Siemens spearheaded DAX advances following a Kepler Cheuvreux rating upgrade from “reduce” to “hold”

- L’Oreal ranked among the session’s weakest performers after J.P. Morgan highlighted concerns about second-half performance

Continental equity markets climbed to unprecedented territory on Friday, concluding a robust week as subdued US employment statistics and more accommodative central banking language reinforced market sentiment.

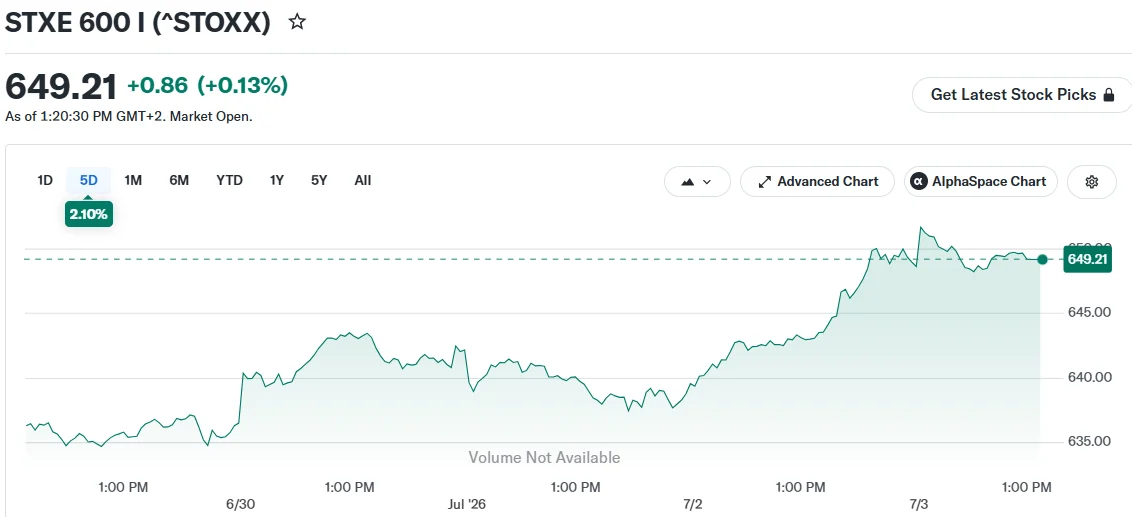

The continent-wide STOXX 600 momentarily reached a historic peak during trading, advancing approximately 0.2% to 649.86 points. Germany’s benchmark DAX similarly achieved a record level, climbing 0.5% intraday. For the week, the STOXX 50 surged 2.3% while the STOXX 600 gained 1.9% — marking its most impressive weekly climb in approximately four weeks.

The upward momentum extended across multiple sectors, with technology, industrials, financial institutions, automotive manufacturers, and utility companies all recording positive movements.

US Employment Figures Drive Sentiment Shift

The primary driver behind the advance was Thursday’s US employment report, which registered below market forecasts. This development prompted investors to recalibrate their expectations regarding a Federal Reserve rate increase at the September policy meeting.

Prior to the release, financial markets had priced in over 60% probability that the Fed would implement a rate hike in September, influenced partially by initial remarks from recently appointed Fed Chair Kevin Warsh. Following the data publication, expectations pivoted toward maintaining current rates until October at the earliest.

A more cautious Fed stance carries significance for continental markets. It alleviates upward pressure on worldwide financing costs and diminishes capital outflows from the euro area toward more attractive US yields.

ECB Commentary Reinforces Market Confidence

European Central Bank President Christine Lagarde contributed to the constructive atmosphere at the ECB’s yearly forum in Sintra, Portugal. She noted that threats to euro area inflation and economic expansion are achieving greater balance — a subtle linguistic adjustment that markets interpreted as diminished urgency for continued rate increases.

Earlier during the week, euro zone inflation measurements for June registered below analyst predictions. Market participants now anticipate merely 23 basis points of total ECB rate increases for the remainder of the calendar year.

Developments in US-Iran diplomatic negotiations also provided support, driving oil quotations lower and alleviating supply chain constraints for continental enterprises.

Individual Equity Performance

Siemens emerged as the prominent DAX winner, surging approximately 1.7% to 1.8% following Kepler Cheuvreux’s rating elevation to “hold” from “reduce.”

Semiconductor equities also delivered strong results. Soitec and Aixtron each appreciated 4.1%, while BE Semiconductor climbed 3.6%. Technology stocks had previously recorded their largest quarterly appreciation since 2001 earlier in the week, propelled by the worldwide artificial intelligence-driven rally.

French benefits provider Pluxee advanced 5.3% after reporting a third-quarter organic sales decline smaller than market expectations.

Among decliners, L’Oreal retreated approximately 2.6% after J.P. Morgan communicated expectations for deteriorating second-half performance for the beauty products manufacturer. Kering similarly declined around 1.9%.

Defense sector equities edged upward following accounts of Russia’s most devastating attack on Ukraine this year, with market participants forecasting elevated defense expenditures.

In London, the FTSE 100 declined 0.3%, pressured by its substantial commodity sector weighting. Pirelli appreciated 2% on reports of potential stake acquisition interest from Czech enterprises, while Auto1 Group rose 2% after J.P. Morgan included it on its positive catalyst monitoring list.

Trading activity was projected to remain subdued due to a US national holiday.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants