TLDR

- The greenback is experiencing its steepest weekly decline since early April, dropping approximately 0.7% over the past five trading days

- June employment figures showed only 57,000 new jobs added, significantly below the anticipated 110,000

- Probability of a Federal Reserve rate increase in September plummeted from approximately 64% to between 35–52%

- The yen experienced a modest recovery after touching a four-decade low of 162.84 against the dollar

- Japanese officials signaled readiness to intervene in currency markets if necessary

The greenback is poised for its most significant weekly decline in almost three months following a lackluster June employment report that dampened market expectations for additional Federal Reserve interest rate increases.

June’s nonfarm payroll figures revealed an addition of merely 57,000 jobs. This result fell considerably short of the 110,000 consensus estimate from economists. Additionally, employment data from the previous two months underwent downward revisions.

The labor force participation metric declined to 61.5%, marking its weakest reading in over five years. Market participants swiftly adjusted their expectations regarding the likelihood of imminent Federal Reserve policy tightening.

Prior to the employment data release, financial markets had been assigning roughly a 64% probability to a September rate increase. Following the report, that figure dropped to a range of 35% to 52%, based on CME FedWatch and LSEG analytics.

U.S. government bond yields also retreated. Two-year Treasury note yields, which demonstrate high sensitivity to rate outlook changes, ended a three-session rally with a four basis-point decline.

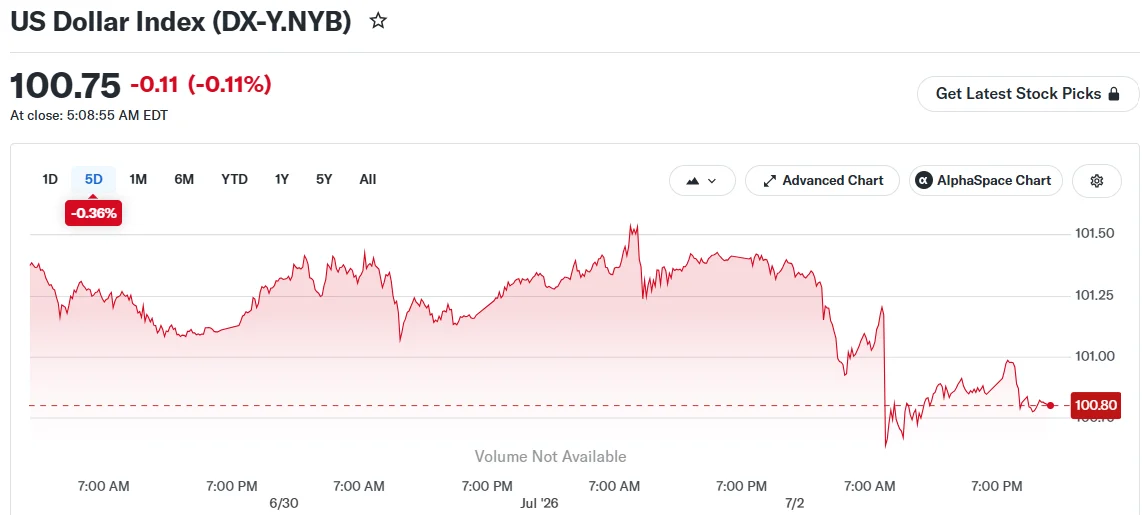

The dollar index, which measures the currency against a collection of major international counterparts, decreased roughly 0.3% to reach 100.68 on Friday. For the entire week, the index is down approximately 0.7%, representing its largest weekly drop since early April.

Currency Markets React

The euro advanced to nearly $1.1472, approaching a two-week peak, and is tracking for a weekly increase of around 0.6%. Sterling strengthened to $1.3380, positioning itself for a 1.2% weekly gain — its strongest performance in nearly three months.

The Australian dollar climbed to $0.6935, appearing set to end a four-week decline. The New Zealand dollar posted approximately a 1.2% weekly advance.

Karl Steiner, head of analysis at SEB, noted the disappointing data aligned with his team’s projection that the dollar would ultimately weaken. He indicated further downside movement remains possible.

Yen Watchfulness

The Japanese yen received some reprieve this week, recovering above the 161 per dollar level after touching a 40-year nadir of 162.84 on Thursday.

Japanese Finance Minister Satsuki Katayama stated on Friday that Tokyo maintains consistent communication with Washington regarding currency matters and remains prepared to take action. Chief Cabinet Secretary Minoru Kihara emphasized that authorities were monitoring markets with heightened urgency.

Market participants are now vigilant for potential intervention, particularly during light holiday trading conditions with U.S. markets shuttered for Independence Day.

Tony Sycamore, analyst at IG, suggested 162.83 appears to represent a near-term ceiling for the dollar-yen exchange rate. He noted that the pair’s future direction will depend substantially on forthcoming U.S. economic releases and developments in the Japanese government bond market.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants