TLDR

- June employment figures showed only 57,000 new positions, significantly below the anticipated 113,000.

- Major indices advanced following the data release, with the Dow climbing approximately 0.7%.

- Unemployment ticked down to 4.2%, better than the projected 4.3%.

- Federal Reserve Chair Kevin Warsh emphasized that markets should focus on economic indicators rather than Fed guidance.

- Market pricing now shows a 21.7% probability of rates remaining unchanged through the year’s end, per CME FedWatch Tool.

Equity markets posted solid gains Thursday following the release of June employment data that came in substantially below forecasts, giving investors confidence that the Federal Reserve might pause its monetary tightening campaign.

The Dow Jones Industrial Average advanced approximately 370 points, representing a 0.7% increase. The S&P 500 climbed 0.6%, while the Nasdaq Composite posted a 0.5% gain during morning trading sessions.

Employment Figures Fall Short of Expectations

According to the Labor Department’s latest release, the U.S. economy generated 57,000 new positions in June. This figure significantly underperformed analyst projections of 113,000. The result marked a considerable deceleration from the robust hiring pace observed during the prior three-month period.

The jobless rate registered at 4.2%, slightly better than the consensus estimate of 4.3%, delivering a modest positive surprise.

The softer employment numbers brought an end to three consecutive months of robust job creation. The data also fundamentally altered market expectations regarding the central bank’s future policy direction.

Federal Reserve Chair Kevin Warsh recently advised Wall Street participants to concentrate on incoming economic indicators instead of relying on central bank communications for direction. Thursday’s employment figures provided market participants with tangible information to assess.

Chris Zaccarelli, chief investment officer at Northlight Asset Management, suggested the weaker hiring momentum might prompt even the more hawkish Federal Reserve officials to recalibrate their stance on aggressive rate increases.

Market-implied probabilities for unchanged rates through year-end increased to 21.7%, based on CME FedWatch Tool data. However, traders continue to price in at least one potential rate increase during 2025.

Treasury market yields responded to the employment data. The 2-year yield declined to 4.15%, while the 10-year yield moved slightly higher to 4.49%. The greenback weakened against major currencies.

Technology Sector Faces Headwinds From Semiconductor Weakness

Despite broader market strength, technology shares encountered resistance. The Nasdaq underperformed relative to both the Dow and S&P 500 during the trading day.

A sharp decline in South Korean semiconductor manufacturers dampened investor sentiment. The Kospi benchmark plunged 7.9%. SK Hynix tumbled more than 14%, while Samsung Electronics declined over 9%. Both technology giants had recently unveiled substantial artificial intelligence infrastructure investment programs.

Microsoft shares moved counter to the broader technology sector trend, posting gains despite widespread weakness among peers.

Oil prices retreated after Qatar, serving as mediator in U.S.-Iran nuclear negotiations, characterized this week’s diplomatic discussions as constructive. While no agreement was finalized, the diplomatic tone was interpreted favorably by commodity markets.

With U.S. exchanges scheduled to close Friday in observance of Independence Day, some market participants appeared to be adjusting positions ahead of the extended weekend.

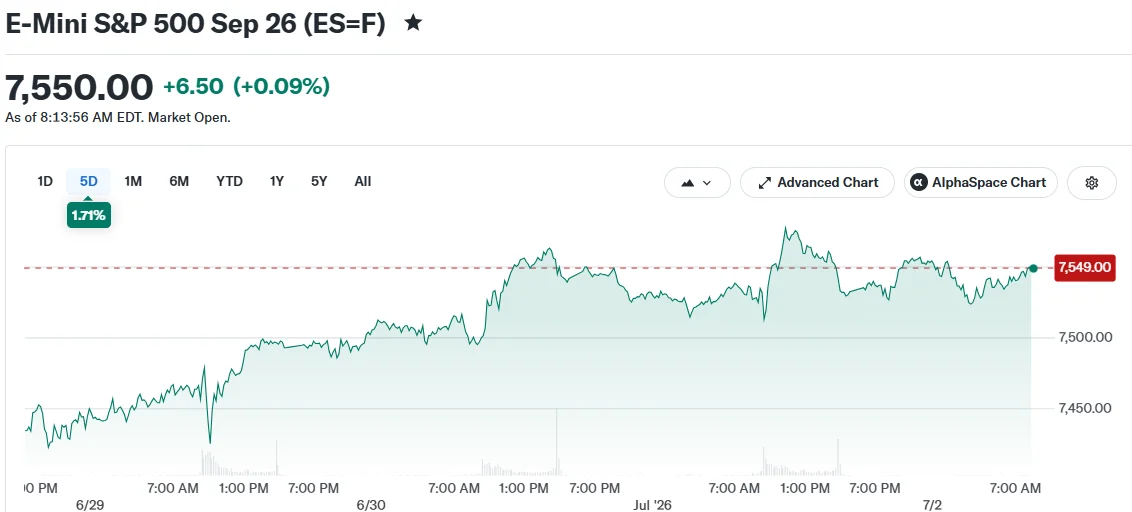

The S&P 500 was changing hands at 7,501 during midday trading. The Dow stood at 52,757. The Nasdaq was positioned at 25,992.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants