Key Takeaways

- Year-to-date gains for the S&P 500 exceed 7%, though June has seen considerable volatility

- Thursday’s employment data release could intensify speculation about potential rate increases

- Federal Reserve maintains hawkish position with primary emphasis on combating inflation

- Chip sector rallied 85% from spring bottom before experiencing sharp correction this week

- Consumer price increases breached 4% threshold for first time since 2023, driven by energy sector

Investors are approaching the upcoming week with heightened attention on Thursday’s employment figures while navigating significant swings in the technology sector. Concerns about monetary policy tightening combined with unstable semiconductor equities have created uncertainty as the year reaches its midpoint.

The benchmark S&P 500 has delivered gains exceeding 7% through the first half of 2026. However, the most recent month has proven challenging, with equities surrendering portions of their previous advances.

Employment Data Takes Center Stage

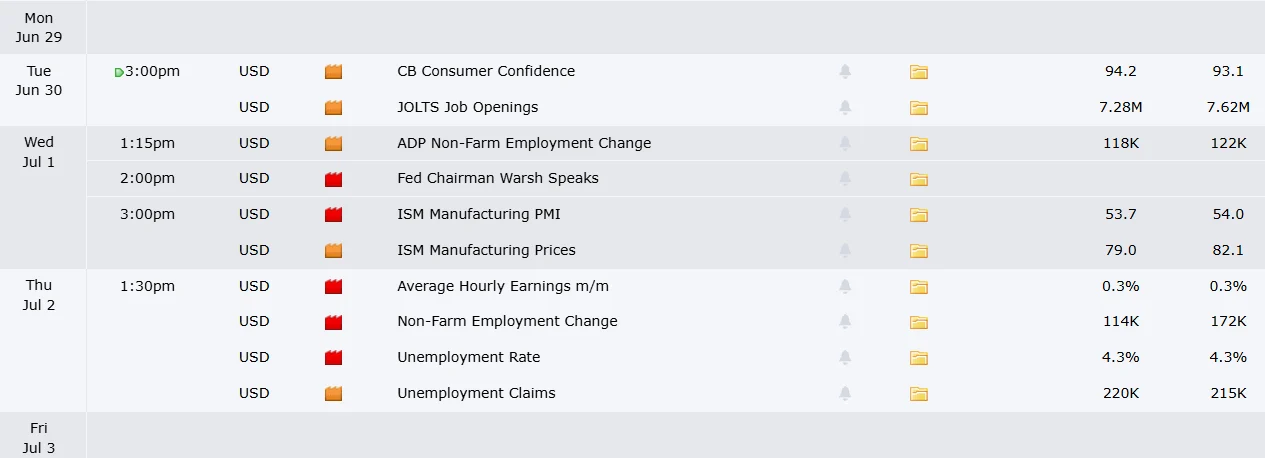

The labor market report for June arrives on Thursday. Analysts surveyed by Reuters anticipate approximately 110,000 positions were created during the previous month. May’s figures showed 172,000 new positions, marking the third consecutive month of robust employment expansion.

Robust employment figures could prove problematic for equity markets. Market participants fear such results would increase the likelihood of the Federal Reserve implementing rate increases instead of the previously anticipated reductions.

“Should we receive particularly strong employment data, I anticipate the market will interpret this negatively,” stated Doug Huber from Wealth Enhancement. He suggested such an outcome would elevate probabilities of monetary tightening.

Futures contracts for federal funds currently indicate greater than 50% probability of a rate increase by September. This represents a dramatic shift from early 2026 expectations, when traders anticipated rate reductions before year-end.

The central bank emphasized at its most recent policy meeting that inflation management remains the top objective. Price pressures have now exceeded the 4% mark for the first time in three years, partially attributable to elevated energy prices connected to Middle Eastern tensions.

Elevated interest rates increase financing expenses for both corporations and households. They additionally decelerate economic expansion and can negatively impact equity valuations.

Technology Sector Faces Headwinds

Equities in the technology space have dominated Wall Street narratives throughout recent months. The Philadelphia Semiconductor Index surged 85% from late-March lows. However, the sector experienced a pullback this week as market participants questioned the sustainability of the advance.

Micron Technology delivered robust quarterly results on Wednesday, providing temporary sector support. Nevertheless, the Nasdaq experienced a decline exceeding 4% during the week.

“The critical question remains whether elevated interest rates will undermine the more cyclical and volatile elements currently driving market performance,” noted Julia Hermann from New York Life Investment Management.

Oil prices have moderated, declining to approximately $70 per barrel from $100 monthly earlier following a Middle Eastern ceasefire agreement. This development could alleviate inflationary pressures if sustained.

Nike’s quarterly earnings release is scheduled for next week. The second-quarter reporting period accelerates more broadly throughout mid-July.

The Federal Reserve continues navigating a challenging environment. Employment statistics that deviate significantly in either direction could rapidly alter market expectations as the second half commences.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants