Earnings, Treasury Yields, and Retail Earnings Dominate This Week’s Market Focus")

Quick Summary

- Nvidia’s Wednesday after-hours earnings release expects $1.78 per share and $79.2 billion revenue, drawing intense market attention

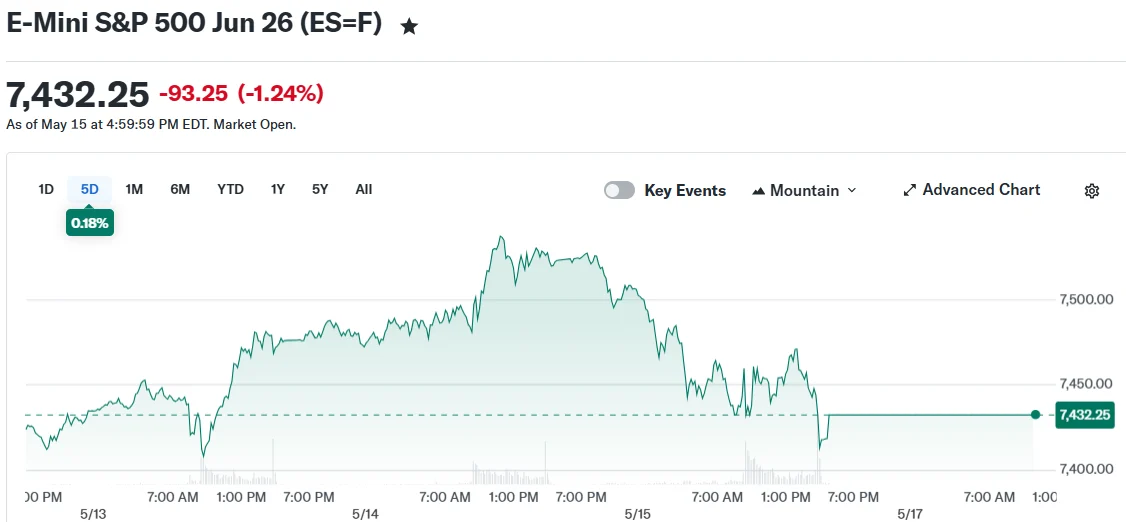

- Major indexes stumbled Friday with the S&P 500 falling 1.2%, snapping a seven-week positive streak on a disappointing close

- Treasury yields breached 4.5% on the 10-year note, maintaining downward pressure across equity markets

- Carlyle Group’s Jeff Currie suggests commodity markets may be starting an extended multi-year bull cycle

- Walmart’s Thursday earnings will provide crucial consumer health signals as April CPI registered 3.8%

Market participants enter the trading week with considerable uncertainty. Equity benchmarks declined Friday, Treasury rates advanced higher, and diplomatic friction from recent Trump-Xi discussions continues weighing on sentiment.

The S&P 500 surrendered 1.2% Friday, though it squeezed out a marginal 0.1% weekly advance — marking seven consecutive weeks of positive performance. The Nasdaq relinquished 1.5% Friday, concluding the week approximately 0.1% lower. The Dow similarly finished the week in negative territory, declining 0.2%.

The 10-year Treasury note yield pushed decisively beyond 4.5% Friday, a threshold that has traditionally created headwinds for stock valuations. This benchmark will remain under close observation as trading commences.

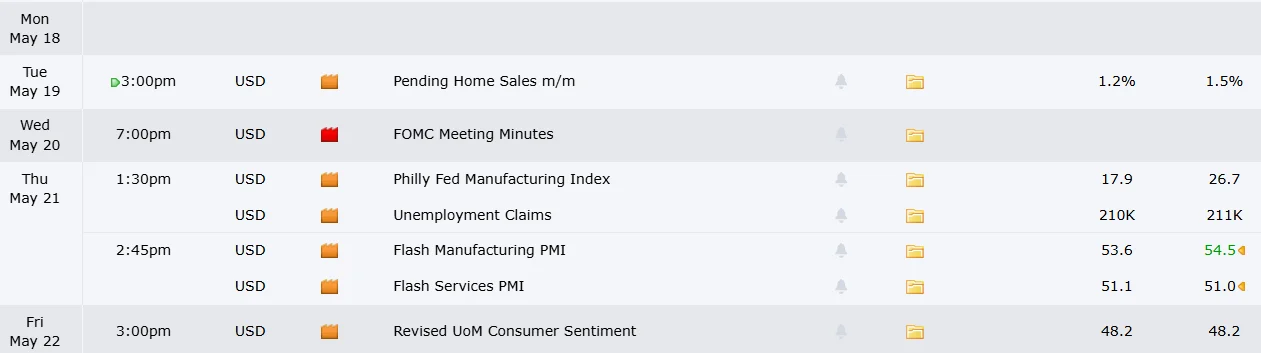

The upcoming week’s economic calendar appears less congested than recent periods, yet one announcement dominates attention.

All Eyes on Nvidia’s Quarterly Performance

Nvidia plans to unveil first-quarter financial data Wednesday following the closing bell. The company currently holds the distinction of being the world’s most valuable corporation, surpassing $5.7 trillion in market capitalization last week.

Wall Street consensus anticipates adjusted profits of $1.78 per share alongside revenue reaching $79.2 billion.

During March remarks, Nvidia CEO Jensen Huang characterized demand for the company’s products as “off the charts.” He escalated forecasts for two major product categories, projecting potential revenues exceeding $1 trillion by late 2026.

Huang recently accompanied President Trump on a China visit, engaging with government representatives and corporate executives. Market observers will scrutinize any disclosure regarding negotiations or partnerships established during those discussions.

Reuters disclosed last week that Chinese technology giants including Alibaba, Tencent, ByteDance, and JD.com received authorization to purchase Nvidia’s H200 processors. This development propelled shares to record highs Thursday before retreating Friday.

Notwithstanding the impressive rally, UBS analyst Tim Arcuri observed that numerous institutional investors have displayed subdued optimism approaching the announcement, potentially creating conditions for upside surprise if performance exceeds expectations.

Bank of America analyst Vivek Arya highlighted that market participants will scrutinize management commentary regarding competitive dynamics with Advanced Micro Devices, Broadcom, and emerging challenger Cerebrus, which completed its public offering last week.

Walmart, Retail Sector, and Consumer Health Indicators

Walmart unveils results Thursday morning. Attention remains elevated considering April’s Consumer Price Index demonstrated 3.8% year-over-year growth, predominantly influenced by escalating energy prices.

During the previous quarter, Walmart characterized its customer base as “resilient.” This week’s report will test whether that characterization remains accurate.

Target additionally reports Wednesday. Newly appointed CEO Michael Fiddelke has articulated strategies focused on restoring growth momentum. Home Depot and Lowe’s deliver results Tuesday and Wednesday respectively, though both face challenges as residential real estate activity remains subdued.

The University of Michigan’s consumer confidence and inflation expectation survey releases Friday, completing the week’s macroeconomic data.

Is a Commodity Supercycle Beginning?

Carlyle Group energy strategist Jeff Currie published extensive analysis Friday proposing markets may be initiating an extended commodity bull market.

Currie identified AI’s expanding requirements for tangible infrastructure — including energy resources, industrial metals, and processing capabilities — as a primary catalyst. He referenced the Iran situation, which Goldman Sachs estimates has withdrawn over 13.7 million barrels daily from global markets, representing the most substantial energy supply disruption recorded.

Currie contends capital has concentrated toward the AI trade while the fundamental physical resources required for AI deployment have experienced chronic underinvestment. He maintains this mismatch is beginning to resolve itself.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants